What is an Acquisition?

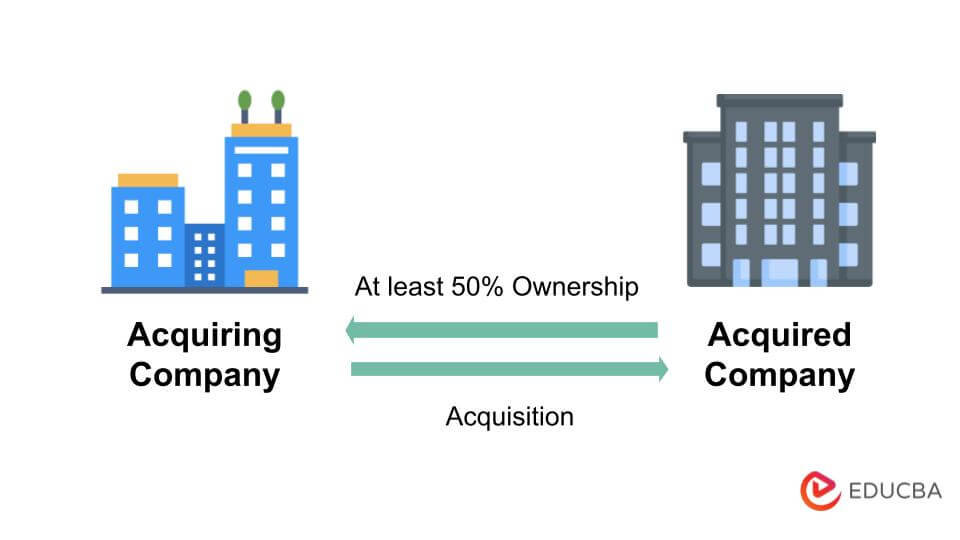

An acquisition is a deal where one firm buys a fraction of or all stocks of the other organization to gain operational control over it. Here, the two parties involved are the acquirer and the target company. An acquisition example would be Disney acquiring 21st Century Fox.

There are multiple reasons why the company decides to acquire another company. If they purchase over 50% of the target company’s shares and assets, they can control it without needing approval from shareholders. However, it does not affect the target firm’s brand name and autonomy. It only assists with entering a new industry and utilizing the resources and skills of the acquired organization.

Most importantly, post-acquisition, both companies exist. Still, only the acquiring company reports the consolidated balance financial statement, including the results of the target company. The acquisition of one company by another always creates a synergy value. Various areas can demonstrate synergy, including an increase in revenue, a decrease in expenses, or a reduction in the overall cost of capital.

Table of Contents

Key Highlights

- A corporate combination known as an acquisition occurs when one company purchases the majority or all of the shares of another organization.

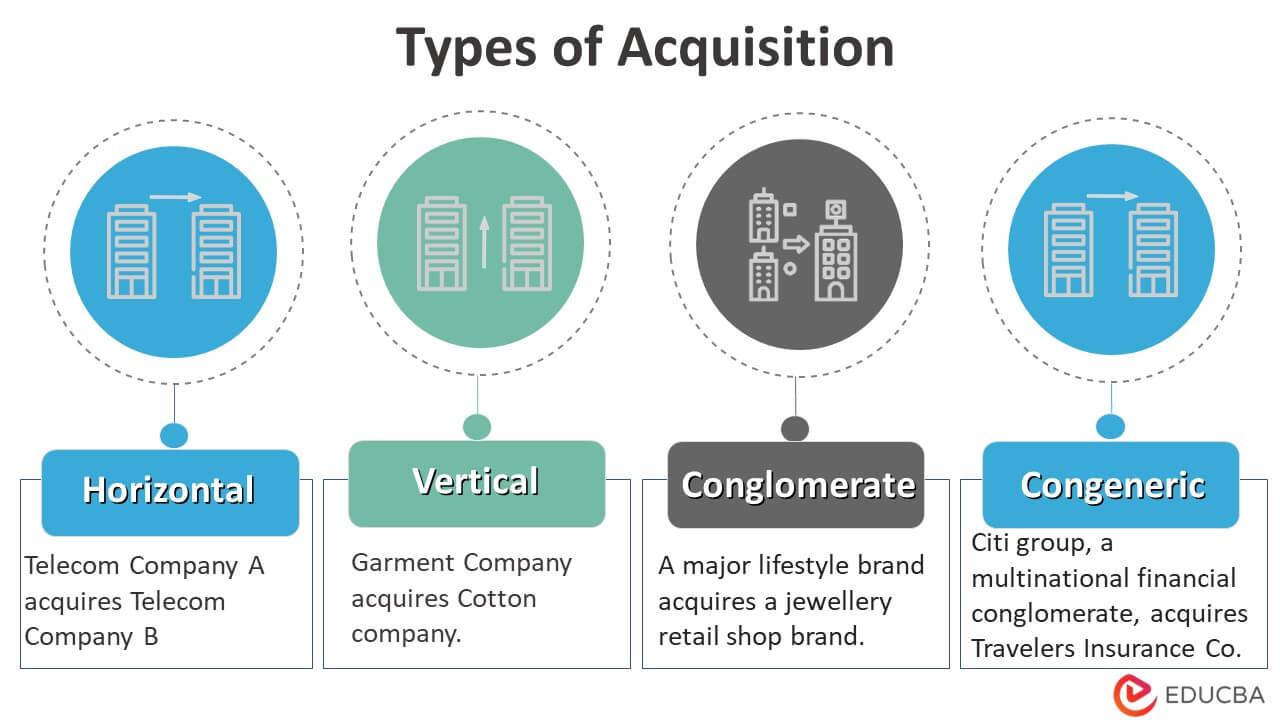

- There are four types of acquisition: Horizontal, vertical, congeneric, and conglomerate.

- Mergers are distinct from acquisitions as, in a merger, only one entity remains after the union, and the other corporation no longer exists.

- Businesses buy other businesses for cost savings, increased market share, diversity, and scale advantages.

How do Acquisitions Work?

The acquisition is a form of a business combination. It is when a firm acquires an established business to grow itself. As with most business combinations, the percentage should be at least 50% or more. However, transactions with less than 50% interest but significant controlling influence can sometimes occur.

The target business continues to operate as before, only the ownership shifts. The purchasing corporation may make some inroads into the target’s operations, but not to the extent that the target company dissolves altogether. The acquiring company can make decisions regarding the target company’s policies. In other forms of inter-corporate investments, either the influence is low or significant but not controlled.

The method of accounting used for all business combination transactions under both IFRS and US GAAP is known as the ’Acquisition’ method. When it is less than 100% of the target company, the minority interest shows on the consolidated balance sheet of the acquiring company.

Examples of Company Acquisition

Acquisition examples are as follows:

Example 1 – Acquisition of the Company Ranbaxy by the Sun Pharmaceuticals

The deal started when Sun Pharmaceuticals declared that it would acquire the company Ranbaxy and the deal got completed after that. The company got approval for the acquisition from different authorities. This acquisition example represents a classical share swap deal, wherein it was determined that Ranbaxy shareholders would receive four Sun Pharma shares for every five they held in Ranbaxy. 4 shares of Sun Pharma for 5 shares in Ranbaxy. This deal leads to the dilution of the 16.4 % equity capital of Sun Pharma.

Sun Pharma expressed interest in the acquisition because they believed that acquiring Ranbaxy would provide them with improved access to emerging markets and bolster Sun Pharma’s presence in the domestic market. After the merger, Sun Pharma can enter new markets by filling the gaps in the company’s offerings with the help of the acquired company.

With the help of the acquisition, it will also come to the first position as a generic company in the dermatology space. Before the acquisition, it was not holding as before; it was in the third position in the US market as a generic company in dermatology. The merger will help boost the products offered by Sun Pharma as it will create more visibility and market share in the pharmaceutical industry.

From the perspective of Ranbaxy also, the acquisition led to the turnaround of the distressed business.

Example 2 – Acquisition of the Company Whole Foods by the Amazon

In 2017, Amazon, the e-commerce announced that it would buy a high-end organic chain of groceries named Whole Foods for $ 13.7 billion or $ 42 per share. The deal was done officially by the end of August 2017. Whole food is a leader in the US for distributing natural and organic food products.

The acquisition by the Amazon of Whole Foods makes it possible to combine two leading brands, both focusing on the customer-centered approach. This will allow Amazon to expand the multichannel offering of its company and further enhance the customer experience in the market. Amazon expressed interest in the acquisition because it recognized the enormous potential for the development of Whole Foods. Initially, Whole Foods had a strong presence primarily in the U.S., but Amazon saw the opportunity to expand the same concept to other countries. Also, Amazon’s management knew that 33% of the company’s annual sales occurred in the fourth quarter of the calendar year. Diversifying into the food industry would help smooth out cash flows and address the seasonality issue associated with this sales pattern.

Thus, the acquisition was towards a rocky start, giving Amazon hundreds of physical stores and providing a strong entryway into the competitive food and grocery industry.

Example 3 – Acquisition of the Shazam by the Apple

Apple, in the year 2017, confirmed the acquisition of Shazam for the amount of $ 400 million by it.

Shazam is a well-known company among customers that lets users identify songs, TV shows, commercials, and movies from short audio clips.

Apple expressed interest in the acquisition because it saw the opportunity to leverage Shazam’s services to enhance Apple Music. At the time of the acquisition, Shazam had amassed a significant user base, with the app being downloaded over 1 billion times. Its users were also very loyal, so with the help of acquisition, Apple can get more paying customers for its own services like apple music. Also, Shazam was a profitable company and generated huge revenue through advertisements, so it makes sense for Apple to invest in the software brand, which already has a recurring amount of revenue and loyal users in some different countries of the world.

Example 4 – Google’s Acquisition of Motorola Mobility

In 2011, Google announced its acquisition of Motorola Mobility. After less than a year, in May 2012, Google finally acquired the company. Motorola operated as an independent entity post-acquisition. The main aim of this was to develop the patents owned by Motorola and prevent the misuse of Google’s Android software.

Google had significant control over Motorola, wherein it could change key personnel, sell off parts of the company to various entities, etc. After owning it for 2-3 years, Google sold it to Lenovo. This deal involved making payments to Motorola shareholders in cash. It meant that Google didn’t want to dilute its control after the acquisition, as it wanted to make hard decisions without resistance from Motorola shareholders.

Example 5 – Walmart’s Acquisition of Flipkart

After more than twenty months of negotiations, Walmart Inc. acquired a 77% share in India’s online retailer Flipkart for $16 billion in 2018. It marks the largest e-commerce business acquisition in the country and the entire world.

Walmart had to safeguard the unification of its two companies because of the overlap in facilities, including warehouses, the distribution network, and labor. Flipkart now has a 360-degree advantage, thanks to Walmart. There were already 200 million online users, and now the subscriber base of retailers is also available.

Types

1. Horizontal

- It is when a company acquires a competitor from the same business industry.

- To survive in the market, companies must consistently increase their market share.

- Therefore, they will have to offer higher-quality goods or buy the rival to drive out the competition.

- For example, one telecom company acquires another, like Facebook acquiring, Instagram, and Whatsapp.

2. Vertical

- It is when a company acquires either a supplier, distributor or a company that buys its products.

- It provides companies with more control over the supply chain.

- Generally affects how raw materials are received and goods are delivered. It, in turn, impacts input sources and product delivery to customers.

- For instance, a garment company buys the source of cotton, such as a farm like Ikea buying a forest in Romania.

3. Conglomerate

- This acquisition occurs between companies that have nothing in common. Here, a company acquires another from a completely different kind of business.

- The primary purpose is diversification. These acquisitions make it possible to provide other companies’ clients with the company’s products.

- It aids the company’s business expansion, client base growth, and improved economies of scale.

- One example is the acquisition of Tanishq by Titan.

4. Congeneric

- It occurs between businesses in the same sector offering distinct product lines.

- These businesses will have something in common: the marketplace, the technologies, or the production cycle.

- By combining their markets, these two businesses can expand their product offerings.

- For example, Citicorp’s acquisition of Travelers Group.

Frequently Asked Questions(FAQs)

Q1. What are some acquisition strategies?

Answer: These are a few tips for businesses looking to acquire another company.

- Every company has different work environments. These are called work cultures. Before acquiring a firm, keep in mind the cultural differences. Employees and management may have difficulty settling in if they are too varied. As a result, it may lead to distress for the business.

- While acquiring another business, make sure the proposal benefits both the business and not just the acquirer. Even though the company is ready to be accepted, it is still looking to profit from it. Thus, it should be profitable for both parties.

- All acquirers must set a specific limit on the investment value. Analyze your own business and the business you are looking to acquire. Create an investment limit and stay within those bounds.

- Sometimes, some acquisitions appear valuable in the beginning but may not seem the same after you have reached the middle of the process. Going through with it may lead to failure. Therefore, exit the deal if it doesn’t match your goals.

Q2. What does Special Purpose Acquisition Company mean?

Answer: A special purpose acquisition company (SPAC) intends to raise money through an initial public offering (IPO) to purchase another business. Shareholders or sponsors knowledgeable about a specific industry establish these to pursue opportunities.

The funds that SPACs raise go into an equity trust fund. They can only use the money to finalize an acquisition. If the SPAC dissolves, the funds return to shareholders. To avoid liquidation, a SPAC has two years to conclude a transaction.

Q3. What is the Cost of Acquisition?

Answer: Acquisition cost is the total amount paid to buy another business. It, however, presents the value before applying taxes. This cost depicts the actual capital acquired by the company, including legal fees, commissions, etc.

One of the ratios is the exchange ratio, which calculates the shares the acquired company’s shareholders will gain. After the acquisition, the company’s shareholders get a relative amount of shares.

The formula is,

Q4. How long does it take for an acquisition to complete?

Answer: Typically, an acquisition takes 4 to 6 months, but this time frame can change depending on the acquirer’s and the target company’s priorities. It can take up to several years as well.

Q5. What is the federal acquisition regulation?

Answer: The primary collection of regulations concerning public procurement in the United States is the Federal Acquisition Regulation. Its goal is to establish standards and guidelines that federal agencies can use while conducting procurement operations. These regulations offer a standard yet adaptable purchasing system to perform federal contracts in a straightforward, equitable, and objective manner.

Recommended Articles

This has been a guide to Acquisition Examples. Here we have discussed the top 5 practical examples of acquisitions with a detailed explanation. You can also go through our other suggested articles to learn more –