Updated August 9, 2023

What is an Enterprise Value Calculation?

In our last tutorial, we understood the concept of market risk premium (MRP). Now, we will see enterprise value calculation and learn about some adjustments for valuation.

Find the present value of the projected cash flows using NPV/XNPV formulas (discussed in our Excel classes).

The projected cash flows of the firm divide into two parts:

- Explicit Period (the period for which FCFF Formula was calculated – till 2013E)

- Period after the explicit period (post 2013E)

The Concept of Enterprise Value Calculation

The concept of present value implies that a dollar today is worth more than a dollar tomorrow (assuming a positive interest rate). For example, US$1.00 in a savings account today, earning 5%, will be worth US$1.05 one year from today. Similarly, Rs 1.05 one year from today, assuming a 5% investment rate, equals Rs 1.00 today.

Enterprise Value Calculation of a single cash flow

Enterprise Value Calculation of multiple cash flows

CF = cash flows

K = discount rate

n = number of years

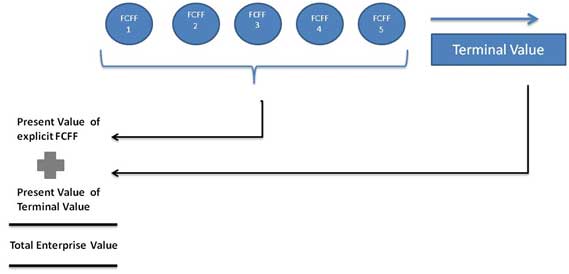

Step 12: Present the Value of the FCFF Formula for the Projected Years

Calculate the Present Value of the Explicit Cash Flows using WACC Formula derived above.

Step 13: Calculate the Enterprise Value Calculation of the Terminal Value using WACC Formula

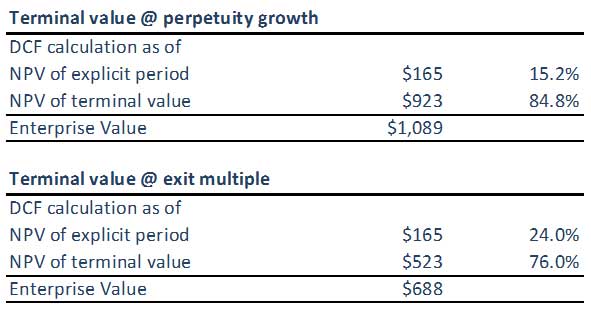

(A) Terminal Value using Perpetuity Growth Method

(B) Terminal Value using Exit Multiple Method

Please note that the Terminal Value from both approaches is not in sync. We may have to double-check our assumptions on EBITDA Exit Multiples or the WACC Formula/growth rate assumptions applied. Both approaches should ideally give similar answers.

Step 14: Calculate the Enterprise Value Calculation of the firm

By summing the (adjusted) present value of the projected free cash flows and the (adjusted) present value of the terminal value (whether calculated using the perpetuity method or multiple methods), the result is the Enterprise Value of the modeled business.

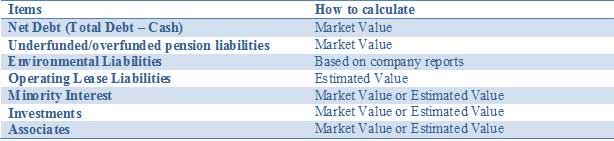

Adjust your valuation for all assets and liabilities, for example, non-core assets and liabilities not accounted for in cash flow projections. The enterprise value may need adjustment by adding other unusual assets or subtracting liabilities to reflect the company’s fair value. These adjustments include:

The above list is not exhaustive, and other potential adjustments relevant to specific situations should be discussed with team members. When performing a DCF analysis, it is important to reflect the values associated with partially-owned investments properly.

Net Debt Adjustments

Lacking more frequent disclosure of the fair value of debt means analysts and investors need to estimate the market value of debt. Although the market value of outstanding bonds can be monitored, this is nearly impossible for the related derivatives. So although conceptually including debt at fair value is the superior approach, this information is not always easily available. Therefore, the use of book value in the majority of cases, especially the difference between book value and market value of debt is only going to be material in a few cases For example, when companies have issued fixed-rate debt and interest rates either move up or down quite significantly.

Another example would be in cases where the credit ratings of the companies involved change quite dramatically. Only in these situations, estimating the fair value of debt and related derivatives to get a better proxy for the bondholders to claim is of recommendation instead of simply using book value.

Minority Interest

Minority interests are pieces of a business consolidated but not fully owned by the consolidating entity. Since the minority’s proportion of income is included in EBIT and free cash flow, the amount ‘owed’ to another owner must be subtracted from the DCFs Total Enterprise Value (TEV) to arrive at a ‘clean’ enterprise and then a ‘clean’ equity value. One can derive the market value of a minority interest by applying the % consolidated but not owned by a total subsidiary TEV. One can calculate the subsidiary TEV in one of three ways:

- If public, utilize existing stock price and debt information

- If private, create a separate DCF if enough information is available

- Utilize a price to book or earnings multiple of comparable companies and add associated debt

The book value of the minority interest plus the relevant portion of consolidated debt can be used as a proxy if no other information is available.

Pension Adjustments

Companies generally offer defined benefits or defined contribution pension plans.

Below we briefly summarize the two types of pension plans:

For Enterprise Value, defined contribution (DC) pension schemes are not relevant, as the employer pays a fixed amount into a pension fund. The pension fund’s investment policy determines the (variable) pension for the employees. As the company has not offered a pension promise to its employees, it neither recognizes pension liabilities nor pension assets on its balance sheet.

Defined benefit (DB) schemes matter for Enterprise Value as the company commits to pay a fixed amount to the employee on retirement. This puts the risk with the employer to pay the pension, creating an economic and accounting liability. To measure pension liability, companies forecast future pension payments by taking into account employee variables, such as inflation, mortality, and retirement dates. These future pension payments are then discounted to the present to get a pension liability. In addition to providing pension benefits to their employees, companies, particularly with activities in the US, offer post-retirement health benefits with a defined benefit character. This means the total obligation to employee benefits combines defined benefit pension plans and other post-employment benefits.

For Enterprise Value, view defined benefit obligations as a loan provided by employees to the company to be repaid upon retirement. Typically in the annual reports, Fair Market Value of Pension Assets and Pension Liabilities have mention.

Environmental Liabilities

Another non-debt liability that we deem to be financing in nature is environmental liabilities. These are long-term liabilities that utilities, energy, and mining companies incur to restore the environment to its original state when companies abandon a production site. Given the long-term nature, companies recognize the liability as a net present value, i.e., they give rise to interest accrual. The combination of long-term period and interest accrual means one should treat them as part of Enterprise Value.

Operating Lease Adjustments

In Accounting, leases are classified as finance (capital) or operating leases. Finance leases are recognized on the balance sheet as tangible assets with accompanying debt finance. Despite their similar characteristics, operating leases are not recognized on the balance sheet (off-balance sheet), with only the operating lease payment being reflected in the income statement. One should include operating leases as an adjustment to the Enterprise Value. One must calculate the The Present Value of Operating Lease rentals. Sometimes due to insufficient information, one multiplies the operating lease rentals by a factor of 8x-10x to arrive at the Present Value of the Operating Lease.

Investments

Investment in marketable securities, stocks, and other companies requires calculation at Market Value wherever possible. For example, stocks and marketable securities can be valued at Market Price. However, for investment in unlisted companies, an estimated value should be used.

What’s Next?

We have learned about various kinds of adjustments. In the next article, we will look at the Equity Value of the firm post Adjustments.

Recommended Articles

Here are some further articles for expanding understanding: