What is Tranching?

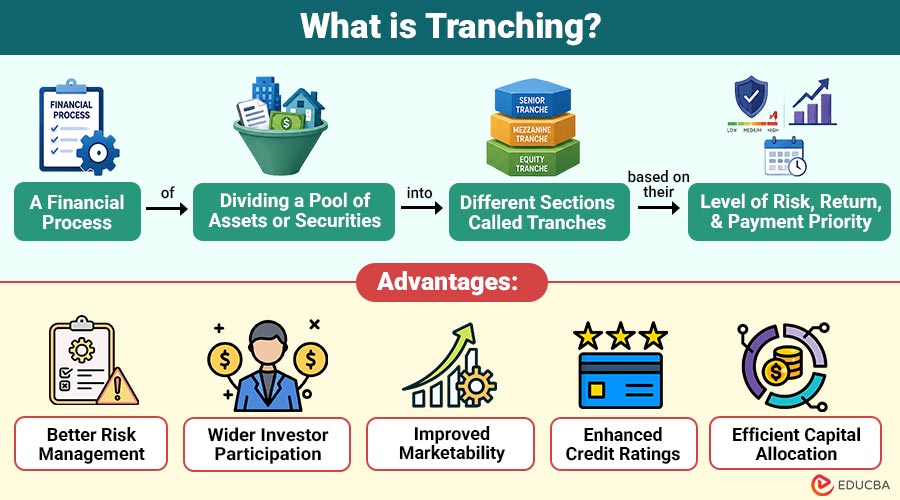

Tranching is a financial process of dividing a pool of assets or securities into different sections, called tranches, based on their level of risk, return, and payment priority. Each tranche is designed to meet the needs of different types of investors. While all tranches are backed by the same underlying assets, they differ in who is paid first and who bears losses first.

In simple words, tranching allows the same investment to be split into multiple layers so investors can choose level of risk and reward that best matches their investment goals.

For example, a bank bundles thousands of home mortgages into a single investment product. It then creates three tranches: a senior tranche with lower risk and lower returns, a mezzanine tranche with moderate risk and returns, and an equity tranche with the highest risk but the potential for the highest returns.

Table of Contents:

Key Takeaways:

- Tranching divides pooled assets into multiple investment layers with different risk, return, and payment priorities.

- Senior tranches receive payments first, while equity tranches absorb losses before higher-priority investors.

- Different tranches help investors align investments with their risk tolerance and return expectations.

- It improves capital allocation but requires an understanding of the underlying assets, structure, and associated investment risks.

How Does Tranching Work?

It follows a structured process that allocates cash flows and risks among different investor groups.

Step 1: Pool Assets

A financial institution combines similar assets, such as mortgages, auto loans, student loans, or corporate debt, into one large investment pool.

Step 2: Create Tranches

The pooled assets are divided into multiple tranches according to payment priority and risk level.

Step 3: Assign Risk Levels

Each tranche receives a different level of risk and expected return.

- Senior tranche – Lowest risk

- Mezzanine tranche – Medium risk

- Equity tranche – Highest risk

Step 4: Sell to Investors

Investors choose the tranche that aligns with their risk tolerance and return expectations.

Step 5: Distribute Payments

As borrowers make payments, the cash flows are distributed in order of priority:

- Senior tranche investors are paid first.

- Mezzanine investors are paid next.

- Equity investors receive the remaining cash flows.

If losses occur, the reverse order applies.

- Equity tranche absorbs losses first.

- The mezzanine tranche absorbs losses next.

- The senior tranche is affected only after the lower tranches are exhausted.

Features of Tranching

The following points highlight the primary features.

1. Risk Segmentation

Investments are divided into multiple tranches based on risk levels, allowing investors to choose the appropriate level of exposure.

2. Payment Priority

Cash flows are distributed according to a predefined payment hierarchy, ensuring senior tranches receive payments before subordinate tranches.

3. Different Return Profiles

Each tranche offers distinct return expectations based on its risk level, payment priority, and potential loss exposure.

4. Credit Enhancement

Lower tranches absorb initial losses, thereby significantly improving the credit quality and stability of higher-ranking senior tranches.

5. Investor Flexibility

Investors can effectively select tranches that align with their risk tolerance, return expectations, investment goals, and overall portfolio strategy.

6. Structured Cash Flow

Payments follow predetermined contractual rules, enhancing transparency, predictability, and efficient allocation of principal and interest among tranches.

Advantages of Tranching

The following are the major advantages:

1. Better Risk Management

Risk is distributed across multiple tranches, allowing investors to assume exposure matching their individual risk tolerance and objectives.

2. Wider Investor Participation

Different tranches attract conservative, moderate, and aggressive investors by offering varying levels of risk, return, and payment priority.

3. Improved Marketability

Structured securities become more attractive because multiple-tranche options effectively meet diverse investment preferences and financial goals.

4. Enhanced Credit Ratings

Senior tranches often receive higher credit ratings because they have payment priority and lower expected default risk.

5. Efficient Capital Allocation

Financial institutions raise capital more efficiently by offering tranches that appeal to different investor categories and preferences.

Disadvantages of Tranching

The following points highlight the disadvantages of tranching.

1. Complex Structure

The layered structure can be difficult for new investors to understand, evaluate, and assess potential investment risks accurately.

2. Higher Risk for Junior Tranches

Junior tranche investors face greater loss potential because they absorb defaults before senior and mezzanine tranche holders.

3. Dependence on Asset Performance

Poor performance or borrower defaults in underlying assets can negatively affect cash flows across multiple tranches over time.

4. Valuation Challenges

Pricing structured securities requires advanced financial models, assumptions, and expertise to accurately estimate fair market value.

5. Reduced Transparency

Complex contractual terms and multiple payment layers may make structured securities harder for investors to understand fully.

6. Liquidity Risk

Certain tranches may have limited market demand, making them difficult to sell quickly at fair prices before maturity.

Applications of Tranching

It is widely used across structured finance and capital markets.

1. Mortgage-Backed Securities

Mortgage payments are distributed among investors across different tranches based on predefined payment priorities and associated investment risks.

2. Collateralized Debt Obligations

Corporate loans and bonds are pooled into structured securities offering tranches with varying risks, returns, and payment priorities.

3. Commercial Mortgage-Backed Securities

Commercial real estate loans are divided into multiple tranches, attracting institutional investors with different risk preferences and objectives.

4. Infrastructure Financing

Large infrastructure projects use it to distribute financing risks among investors with different return expectations and priorities.

5. Project Finance

Infrastructure and energy projects issue multiple debt tranches featuring different repayment priorities, risk levels, and financing terms.

Example of Tranching

The following example illustrates how it works in practice.

A financial institution issues a $300 million mortgage-backed security backed by thousands of residential mortgages.

The security is divided into three tranches:

| Tranche | Investment | Risk Level | Payment Priority |

| Senior | $180 million | Low | First |

| Mezzanine | $90 million | Medium | Second |

| Equity | $30 million | High | Last |

During normal loan repayments:

- Senior investors receive payments first.

- Mezzanine investors receive payments after senior investors.

- Equity investors receive any remaining payments.

Suppose mortgage defaults result in $20 million in losses.

- Equity tranche absorbs the first $20 million loss.

- Senior and mezzanine investors remain unaffected.

If losses increase to $50 million:

- Equity tranche loses its entire $30 million.

- Mezzanine tranche absorbs the remaining $20 million.

- The senior tranche still receives full payments.

This structure protects lower-risk investors while offering higher return opportunities to investors willing to take greater risk.

Who Uses Tranching?

The following are the major financial institutions and market participants that commonly use it for investment, risk management, and structured finance purposes.

1. Investment Banks

Structure and issue securitized products by dividing pooled assets into tranches for different investor categories.

2. Commercial Banks

Use tranching to securitize loans, manage credit exposure, and improve capital efficiency by distributing risk.

3. Asset Management Companies

Invest in different tranches to create diversified portfolios that match clients’ varying risk-return objectives.

4. Pension Funds

Prefer senior tranches to earn a stable income while minimizing investment risk and preserving long-term retirement capital.

5. Insurance Companies

Invest primarily in low-risk senior tranches to generate predictable returns and support policyholder obligations effectively.

6. Hedge Funds

Target higher-risk tranches seeking greater returns through active investment strategies and sophisticated risk management techniques.

Final Thoughts

Tranching helps divide investment risk into multiple layers, allowing different investors to choose securities that match their risk tolerance and return expectations. While it improves flexibility, capital allocation, and risk management, understanding each tranche’s structure and underlying assets is essential before making informed investment decisions.

Frequently Asked Questions (FAQs)

Q1. Who usually invests in senior tranches?

Answer: Conservative investors seeking lower risk and stable returns.

Q2. Can a tranche lose money?

Answer: Yes. Losses depend on the performance of the underlying assets and the tranche’s payment priority.

Q3. Are all tranches backed by the same assets?

Answer: Yes. All tranches are backed by the same asset pool but have different payment priorities.

Q4. Does a higher-risk tranche always generate higher returns?

Answer: Not always. It offers higher return potential, but returns depend on the underlying assets’ performance.

Recommended Articles

We hope that this EDUCBA information on “Tranching” was beneficial to you. You can view EDUCBA’s recommended articles for more information.