What is Term Insurance?

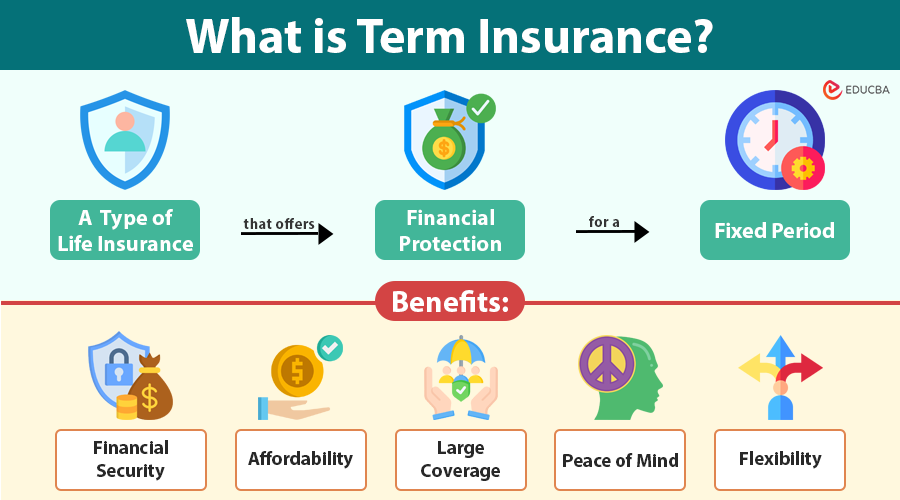

Term insurance is a type of life insurance that offers financial protection for a fixed period, usually 10, 20, or 30 years. If the insured person dies during this period, their nominee receives a lump sum amount known as the death benefit.

However, if the policyholder lives beyond the policy term, they usually do not get any money back unless they choose a return-of-premium plan. The primary objective of term insurance is to protect the family’s finances, allowing them to maintain their lifestyle, pay off loans, or cover education costs in the event of the main earner’s passing.

In 2023, term life insurance premiums in the U.S. reached nearly $3 billion—about 5% higher than in 2022—and term policies made up approximately 19% of the total U.S. individual life insurance market.

Table of Contents

- Meaning

- Features

- Benefits

- Types

- How Does it Work?

- Global Perspective

- Term Insurance vs. Whole Life Insurance

- Who Should Buy?

- How to Choose the Right Insurance?

- Examples

- Companies

Key Takeaways

- Term insurance provides strong financial protection at a low cost, making it an affordable way to safeguard your family’s future.

- There is usually no payout if you survive the policy term, unless you choose a return-of-premium option.

- The global popularity of term insurance is strong, with features such as conversion privileges, living benefits, and inflation-linked sums assured gaining traction worldwide.

- Various types of term insurance exist, including level, decreasing, increasing, return-of-premium, and group plans to suit diverse needs.

- Riders and add-ons enhance coverage, allowing protection against critical illnesses, accidental disability, or premium waivers.

- Term insurance is ideal for individuals with dependents or outstanding debts, as it helps their family maintain their lifestyle and repay loans in the event of the primary earner’s passing away.

Features of Term Insurance

Term insurance is popular because of its straightforward features. Here is a closer look:

- Fixed Term: Policyholders can choose a coverage period that aligns with their family’s financial obligations, such as 20 years for planning their child’s education.

- High Sum Assured: Allows you to buy coverage of up to $2–5 million at reasonable premiums.

- Death Benefit: Nominees get a lump-sum payout if the insured passes away during the policy term, ensuring no disruption in their financial plans.

- No Maturity Benefit: In most cases, there is no payout if the policyholder survives, keeping premiums lower.

- Riders & Add-ons: You can add extra benefits to your policy, such as critical illness cover, premium waiver, or accidental disability cover, for a small additional cost.

- Convertible Options: Some insurers allow you to convert your term policy to a whole life or endowment plan later if your financial priorities change.

- Renewable Features: After your policy ends, you can renew coverage without undergoing new medical underwriting in many regions.

- Global Portability: Many multinational insurers offer term insurance coverage, even if you relocate to another country, making it an ideal option for expatriates.

Benefits of Term Insurance

Term insurance offers a host of compelling advantages:

- Financial Security: Protects your family from a sudden loss of income. According to a 2023 OECD survey, only 43% of adults across participating countries reported that they could cover their living expenses for at least three months without borrowing money or moving home if they lost their main income source.

- Affordability: Term insurance premiums are up to 10 times cheaper than whole life insurance because they do not involve investment or maturity benefits.

- Large Coverage: Term plans can provide substantial coverage to replace your income and pay off debts.

- Peace of Mind: Knowing your family will be financially protected provides immense mental relief.

- Flexibility: Riders allow you to adapt the plan according to your changing needs, for example, adding a critical illness rider after a change in family medical history.

- Simple to Understand: No complex investment-linked returns, making it easy for anyone to buy confidently.

- Tax Benefits: In many countries, individuals can claim tax deductions on term insurance premiums, and the death benefit is typically tax-free for beneficiaries.

Types of Term Insurance

Globally, insurers offer a variety of term insurance products to meet diverse needs:

1. Level Term Insurance

- The payout amount stays the same during the entire policy term.

- Ideal for families who want predictable coverage.

2. Decreasing Term Insurance

- Coverage typically reduces gradually, usually in line with the repayment of a loan, such as a home mortgage.

- Popular in Europe and North America for mortgage protection.

3. Increasing Term Insurance

- The sum assured increases annually to keep pace with inflation.

- Useful in countries with high inflation rates, like parts of Africa and Latin America.

4. Return of Premium Term Insurance

- Refunds all premiums if you survive the term.

- Popular in Asia, where policyholders value getting something back at maturity.

5. Convertible Term Insurance

- Gives you the option to convert to a whole life or endowment plan.

- Provides future flexibility for young professionals.

6. Group Term Insurance

- Often provided by employers for their staff at lower rates.

- A report by the International Labour Organization states that group term insurance covers more than 40% of salaried workers worldwide.

How Does Term Insurance Work?

Let us break it down in practical steps:

- Choose Coverage: Determine the sum assured, term duration, and riders that best suit your family’s needs and budget.

- Pay Premiums: Pay your premiums on a monthly, quarterly, or annual basis. Digital policies have made this process simple worldwide.

- Stay Covered: During the policy term, if you pass away, the insurer pays the agreed death benefit to your nominee, ensuring they can cover living costs, debts, or future goals.

- End of Term: If you complete the policy term without choosing a return-of-premium rider, the insurer will end the policy without paying out any benefit.

Global Perspective on Term Insurance

Term insurance varies in design and popularity across the world:

- United States: Over 60% of new life insurance policies sold are term products, with features like conversion privileges and living benefits for terminal illnesses.

- United Kingdom: Homeowners widely use level-term and decreasing-term policies to protect their mortgages. Many couples also opt for joint life insurance policies to protect their spouses.

- India: Term insurance growth accelerated post-COVID, with IRDAI data showing a 32% year-on-year growth in term policies sold in 2023. Return-of-premium plans are a key preference.

- Europe: Mortgage-related term insurance dominates, with many banks mandating decreasing term policies to cover housing loans.

- Asia-Pacific: A rising middle class and growing awareness about health and protection have driven strong demand. Insurers often include critical illness add-ons.

- Middle East & Africa: Markets are developing, with insurers introducing flexible term products in regions where traditional life insurance penetration is low.

- Latin America: Inflation-indexed term plans are becoming popular due to economic volatility.

Term Insurance vs. Whole Life Insurance

| Feature | Term Insurance | Whole Life Insurance |

| Coverage Period | Fixed term | Entire lifetime |

| Premiums | Lower | Higher |

| Savings Component | None | Has investment/savings element |

| Death Benefit | Only if death occurs in term | Guaranteed whenever death occurs |

| Maturity Benefit | Usually none | Yes |

| Policy Complexity | Simple | Complex |

Who Should Buy Term Insurance?

Term insurance is highly recommended for:

- Young professionals with dependents

- Parents with school-going children

- People with home or personal loans

- Business owners wanting to protect partners

- Families seeking affordable, high-value coverage

- Anyone looking for financial peace of mind without complex products.

How to Choose the Right Term Insurance?

- Assess Your Needs: Consider your current loans, future expenses such as your children’s college fees, and the monthly costs of your dependents.

- Calculate Adequate Coverage: Most financial advisors suggest coverage of 10–15 times your annual income.

- Select the Right Term: Ideally, choose a policy term that protects you until you retire or until you finish repaying major debts.

- Check Claim Settlement Ratios: Always choose insurers with a claim settlement ratio of 95% or higher to ensure smooth payouts.

- Consider Inflation: Opt for increasing term coverage in economies prone to inflation.

- Review Riders: Add critical illness, accidental death, or waiver-of-premium riders for comprehensive coverage.

- Compare Quotes: Obtain at least three to four online quotes and consult with independent advisors.

Examples of Term Insurance

Here are some realistic examples:

1. United States: Family Income Protection

Michael, a 40-year-old father of two in Texas, purchases a 30-year term insurance policy with a $750,000 sum assured, paying $50 per month in premiums. If Michael passes away during the policy term, his wife and children will receive $750,000. This payout can replace his income, pay for the children’s education, and help with their mortgage. If Michael survives the policy term, the insurer pays no money, but he protects his family affordably during his prime earning years.

2. United Kingdom: Mortgage Cover

Sophie and Tom, a married couple in Manchester, buy a joint decreasing term policy of £250,000 over 25 years. The policy links directly to their mortgage, reducing the coverage amount over time as they repay their home loan. If either of them dies before paying off the mortgage, the insurance pays the outstanding loan amount, allowing their children to continue living in the house without debt.

3. India: Return of Premium Term Plan

Rajesh, aged 35, from Bangalore, opts for a ₹1 crore (about $120,000) return-of-premium term insurance for 20 years, paying ₹25,000 per year. If he dies during the policy term, his nominee will get ₹1 crore. If he lives through the term, he will receive ₹5 lakh, which is the total amount of premiums he has paid over 20 years. This gives him both protection and a sense of “no loss” if he stays healthy.

4. Kenya: Inflation-Adjusted Term Plan

Grace, 30, from Nairobi, purchases a 20-year term insurance plan with KES 10 million (approximately $70,000) in coverage, which increases by 5% annually to keep pace with inflation. Her premium is adjusted accordingly. If she dies at any point during the term, her family will receive the increased amount in that year, preserving their purchasing power in an economy with high inflation rates.

Top Term Insurance Companies

Here are some of the leading term insurance providers globally, known for their strong claim settlement ratios, innovative products, and trusted customer service:

1. Prudential (USA)

One of the largest and most reputable life insurers in the United States, offering flexible term plans with conversion and living benefit options.

2. Legal & General (UK)

Highly rated for their affordable term insurance, especially decreasing term policies, which are popular for mortgage protection.

3. LIC (India)

The Life Insurance Corporation of India (LIC) provides a variety of term plans, including return-of-premium options, and is trusted for its strong market reputation and wide reach in rural areas.

4. Allianz (Germany, Global)

A global giant with competitive terms and products and excellent financial ratings, making it a preferred choice for expatriates and multinational coverage.

5. AXA (France, Global)

Provides flexible term insurance plans with a strong presence across Europe, Asia, and the Middle East.

6. Ping An (China)

One of the largest insurers in Asia, known for combining digital services with affordable term plans for a fast-growing middle class.

7. Old Mutual (South Africa)

A top choice in African markets, offering flexible and inflation-adjusted term products to match local economic needs.

Final Thoughts

Term insurance is a universally trusted and proven way to protect your family’s future without stretching your budget. Whether you live in a developed or emerging economy, term insurance provides a simple, affordable, and powerful way to keep your loved ones financially secure in the event of life’s uncertainties.

Frequently Asked Questions (FAQs)

Q1. Can I have more than one term insurance policy?

Answer: Yes, you can buy multiple term insurance policies from different insurers as long as you can justify the total coverage amount based on your income and financial responsibilities. Insurers will typically ask about any existing life insurance when you apply.

Q2. What happens if I miss the premium payment deadline?

Answer: Most term insurance policies give you a grace period of 15 to 30 days to pay your premium without losing coverage. If you do not pay within this timeframe, the policy may end, and you may lose your benefits. Some insurers allow reinstatement within a certain period; however, you may need to undergo additional medical checks.

Q3. Does term insurance cover death due to accidents or pandemics?

Answer: Yes, term insurance generally covers death from natural causes, illnesses, accidents, and pandemics (like COVID-19), unless explicitly excluded in the policy. It is always best to carefully read the exclusions in the policy document.

Q4. Can I change my nominee later?

Answer: Yes. You can change your nominee (beneficiary) at any time during the policy term by filling out a simple form with your insurer. It is advisable to update your nominee if your family circumstances change, for example, after marriage or childbirth.

Q5. Is suicide covered in term insurance?

Answer: Most term insurance policies exclude suicide within the first year of policy inception, but after that initial exclusion period, suicide is usually covered. Always check the suicide clause in your policy wording.

Q6. How soon is the death claim settled?

Answer: Most insurers settle valid term insurance claims within 30 days of receiving complete documentation. Some companies even offer express claims processing within 7–10 days under certain conditions.

Recommended Articles

We hope this comprehensive guide on term insurance has been clear and informative. For more expert-backed insights on insurance and personal finance, explore these related articles: