What is Private Mortgage Insurance?

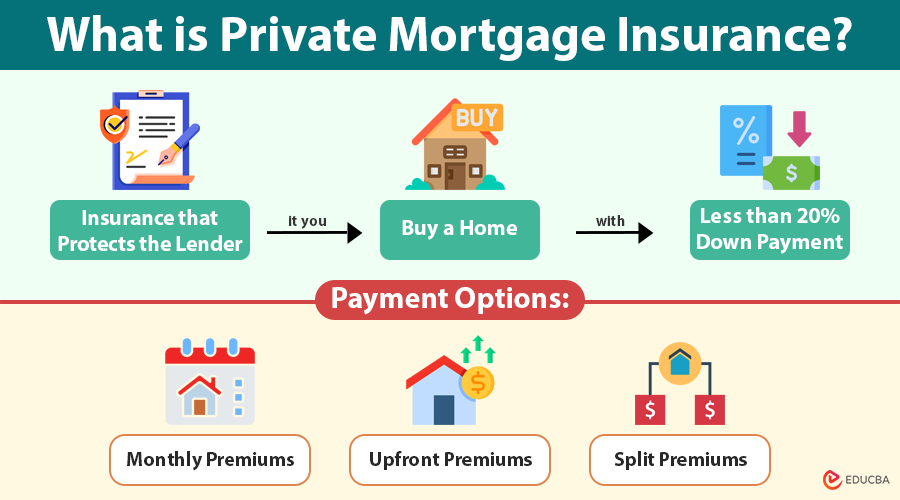

Private Mortgage Insurance (PMI) is insurance that a homebuyer has to pay when they take a regular home loan and make a down payment of less than 20% of the home’s cost. It protects the lender—not the borrower—if the borrower stops making payments on the loan.

Suppose you are buying a home worth $300,000 but can only afford a $15,000 down payment (5%). Since your down payment is less than 20%, the lender will ask you to pay for PMI. This might cost you around $100–$150 per month until your loan balance drops below 80% of the home’s value.

Table of Contents

- What Is Private Mortgage Insurance?

- Why Lenders Require Private Mortgage Insurance?

- When Do You Need to Pay PMI?

- How Much Does Private Mortgage Insurance Cost?

- Ways to Pay for Private Mortgage Insurance?

- How to Cancel Private Mortgage Insurance?

- How to Avoid PMI?

- Pros and Cons of Private Mortgage Insurance

- PMI vs. Mortgage Insurance Premium (MIP)

Key Takeaways

- You need to pay PMI if your down payment is less than 20% on a regular home loan.

- It protects the lender, not the borrower, in case you stop making mortgage payments.

- PMI usually costs between 0.3% and 1.5% of your loan amount each year and is included in your monthly mortgage payment.

- You can cancel PMI once your loan balance reaches 78–80% of your home’s original value or through refinancing/appraisal.

- PMI does not impact your credit score directly, but missed payments can harm your credit.

- Avoid PMI by making a 20% down payment, using VA loans, or exploring options like Lender-Paid Mortgage Insurance (LPMI).

Why Lenders Require Private Mortgage Insurance?

Lenders take on more risk when borrowers put down less than 20%. With a smaller equity stake in the property, the likelihood of default is statistically higher. PMI provides a financial cushion for the lender, covering a portion of the outstanding balance if the borrower stops making payments.

When Do You Need to Pay PMI?

You are generally required to pay PMI if you:

- Take out a conventional loan (not FHA or VA loans)

- Make a down payment of less than 20%

- Refinance with less than 20% equity in your home.

-

Are a first time home buyer and choose a low down payment option to purchase sooner

How Much Does Private Mortgage Insurance Cost?

PMI costs vary based on several factors:

- Loan-to-Value (LTV) Ratio: The higher your LTV, the higher your PMI premiums.

- Credit Score: Borrowers with lower credit scores often pay higher PMI rates.

- Loan Type: Fixed-rate or adjustable-rate mortgages can affect PMI costs.

- Insurer and Loan Size: PMI providers may charge different rates depending on the lender and loan amount.

On average, PMI costs between 0.3% to 1.5% of the original loan amount per year. For example, on a $300,000 loan, PMI might cost between $900 to $4,500 annually ($75 to $375 monthly).

Ways to Pay for Private Mortgage Insurance?

Lenders typically offer a few options for paying PMI:

- Monthly Premiums: Most commonly, PMI is included as part of your monthly mortgage payment.

- Upfront Premium: Paid all at once during closing; this can lower your monthly mortgage payments.

- Split Premium: A combination of upfront and monthly payments.

Discuss these options with your lender to see which best suits your financial situation.

How to Cancel Private Mortgage Insurance?

You can stop paying Private Mortgage Insurance once you have built enough equity in your home:

1. Automatic Termination

Under the Homeowners Protection Act, your lender must automatically cancel PMI when:

- Your loan amount drops to 78% of the home’s original purchase price, and

- You are current on your mortgage payments.

2. Request for Cancellation

You can request PMI cancellation earlier if:

- Your loan amount becomes 80% of the home’s original price, and

- You have a good payment history with no late payments.

3. Reappraisal or Refinancing

If your home value has increased, you may reach the 80% threshold sooner. A new appraisal or refinancing of the loan can help eliminate PMI.

How to Avoid PMI?

Avoiding PMI entirely may be possible through the following strategies:

- Make a 20% Down Payment: The most straightforward way to bypass PMI.

- VA Loans: If you are a veteran or active-duty service member, VA loans do not require PMI.

- Lender-Paid Mortgage Insurance (LPMI): The lender pays the PMI, but you will likely receive a higher interest rate.

- Piggyback Loans: Also called an 80-10-10 loan, this involves two loans to avoid PMI, but it adds complexity and potential risk.

Pros and Cons of Private Mortgage Insurance

Pros

- Enables Homeownership Sooner: You do not need to wait until you have saved 20%.

- May Offer Competitive Rates: PMI can make the home buying more accessible.

- Cancelable: You can eliminate PMI as you build equity.

Cons

- Added Cost: PMI adds to your monthly mortgage expense.

- No Benefit to Borrower: PMI protects the lender, not you.

- Difficult to Cancel if Home Value Drops: Cancellation becomes more challenging in a declining market.

PMI vs. Mortgage Insurance Premium (MIP)

It is important not to confuse PMI with MIP (Mortgage Insurance Premium) required for FHA loans. While both serve to protect the lender, MIP is generally more difficult to remove and applies for the life of the loan unless refinanced.

| Feature | PMI (Conventional Loan) | MIP (FHA Loan) |

| Removable? | Yes (typically at 80% LTV) | Usually not (unless refinanced) |

| Who Pays? | Borrower | Borrower |

| Who it Protects? | Lender | Lender |

| Premium Type | Monthly/Upfront/Split | Upfront + Monthly |

Final Thoughts

Private Mortgage Insurance may seem like an added burden, but it opens doors to homeownership for those who cannot afford a 20% down payment. The key is to understand how it works, budget for it, and plan to remove it as soon as possible. Whether you are buying your first home or refinancing, planning wisely for PMI can make it easier to manage your mortgage.

Frequently Asked Questions (FAQs)

Q1. Does PMI affect my chances of mortgage approval?

Answer: No, PMI does not impact whether you get approved for a loan. Instead, it helps more people qualify for a mortgage even if they cannot make a large down payment. However, lenders factor the added PMI cost into your overall debt-to-income (DTI) ratio when evaluating your application.

Q2. Is PMI tax-deductible?

Answer: The latest tax guidelines allow you to deduct PMI, depending on your income level and when you took out the loan. The deductibility has changed over the years in response to Congress’s decisions. Check with a tax expert or visit the IRS website for the latest updates.

Q3. Can PMI be transferred if I refinance or sell my home?

Answer: No, PMI does not transfer to a new mortgage or new borrower. If you refinance and still have less than 20% equity, you may need to get new PMI coverage. If you sell your home, the buyer will go through their loan approval process.

Q4. Does PMI affect my credit score?

Answer: PMI payments are not shared with credit bureaus and do not directly affect your credit score. However, late or missed mortgage payments (which include PMI if bundled) will hurt your credit, so it is essential to stay current.

Recommended Articles

We hope this detailed guide on Private Mortgage Insurance helps you make informed decisions when planning to buy a home. Explore the following resources to learn more about home financing options and smart borrowing strategies: