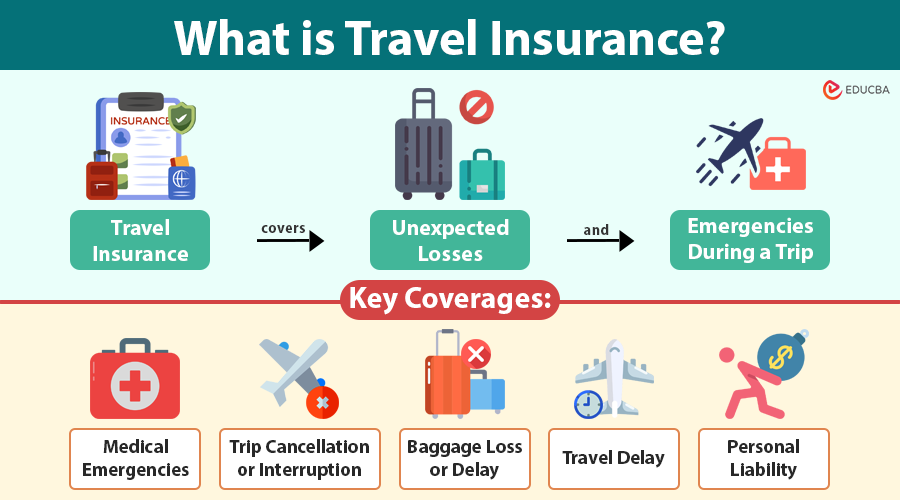

What Is Travel Insurance?

Travel insurance is a type of coverage that helps you pay for unexpected problems that can happen during a trip, like getting sick, losing luggage, or canceling your plans. It can cover medical emergencies, trip cancellations, lost luggage, flight delays, and other related expenses.

For example, imagine you are on vacation in Italy and suddenly fall ill, requiring hospitalization. If you have travel insurance, it covers your hospital stay and helps you get back home if needed.

Table of Contents

- Meaning

- Types

- Why does it matter?

- Key Coverage Areas

- Optional Add-Ons and Specialized Policies

- Regional Differences

- How to Choose the Right Travel Insurance?

- Common Exclusions to Watch Out For

- Travel Insurance in a Post-Pandemic World

- Leading Providers

Key Takeaways

- Travel insurance covers unexpected losses and emergencies during a trip.

- Insurers offer policies based on trip type—single-trip, annual, or long-term—and allow travelers to customize them with add-ons for specific needs.

- Medical emergencies are the most critical coverage area, especially in countries with high healthcare costs.

- Some destinations require insurance (e.g., Schengen countries), making it essential for visa approvals.

- Coverage for COVID-19 and options like Cancel For Any Reason (CFAR) are now commonly included in modern plans.

- Top insurers offer 24/7 support, fast claims, and flexible options for students, families, and remote workers.

Types of Travel Insurance Policies

Travel insurance can be customized to meet the traveler’s specific needs and the duration of their trip. The main types include:

- Single-trip policies: Cover a specific trip with a fixed start and end date.

- Annual or multi-trip policies: Good for frequent travelers, as it covers multiple trips in a year.

- Long-term travel insurance: Designed for extended travel, often chosen by backpackers, digital nomads, or international students.

Why Travel Insurance Matters?

Travel insurance is a universally relevant product for several reasons:

- Medical expenses: Healthcare costs vary dramatically across countries. In the U.S., even a short hospital stay can cost thousands of dollars, while many European countries do not offer subsidized care to non-EU travelers.

- Legal requirements: Some countries require you to have travel insurance to enter. For example, all Schengen countries’ medical insurance with a minimum coverage of at least €30,000

- Unpredictable events: Natural disasters, airline strikes, or geopolitical instability can disrupt plans and cause significant disruptions. Insurance helps recover non-refundable costs.

- Travel trends: With the rise of digital nomads and remote workers, more people are traveling for extended periods and to offbeat locations, where risks are higher and infrastructure may be limited.

Key Coverage Areas

Some key coverage areas under travel insurance are:

1. Medical Emergencies

This is the most crucial part of any travel insurance policy. It covers:

- Hospitalization and surgeries

- Doctor consultations and prescriptions

- Emergency evacuation and air ambulance services

- Repatriation of remains in case of death.

Some policies also cover COVID-19-related treatments, although coverage levels and terms can vary.

Example:

While trekking in Nepal, you suffer a fall and need surgery. Travel insurance covers your hospital stay, surgery, and even an airlift to a better facility.

2. Trip Cancellation or Interruption

This benefit reimburses you for non-refundable costs if you have to cancel or cut short your trip due to:

- Personal illness or injury

- Death or serious illness of a family member

- Natural disasters at your destination

- Job loss or jury duty.

It helps safeguard large pre-paid expenses such as flights, cruises, and hotel bookings.

Example:

You cancel your honeymoon to Japan after being hospitalized with dengue. Your policy refunds the cost of non-refundable flights and hotel reservations.

3. Baggage Loss or Delay

Lost or delayed baggage is a common travel inconvenience. This feature typically covers:

- Lost, stolen, or damaged personal belongings

- Essentials like clothes and toiletries if baggage is delayed

- Reimbursement for baggage delivery fees.

Example:The airline delays your luggage for two days in Paris. The insurance reimburses you for essentials like clothes, toiletries, and a new phone charger.

4. Travel Delay

This clause covers delays caused by weather conditions, mechanical issues, or other unforeseen disruptions. Insurance may reimburse:

- Meals and accommodations during the delay

- Transportation costs to catch up with your itinerary

- Missed connections.

Example:

Your flight from London to Rome is delayed overnight due to a snowstorm. Your travel insurance covers the hotel stay and meals.

5. Personal Liability

This aspect protects you if you cause injury or property damage to someone else. It is particularly useful in countries where litigation is common. Coverage usually includes:

- Legal fees

- Compensation payments

- Court-related expenses.

Example:

You accidentally knock over a valuable sculpture in a hotel lobby. Travel insurance covers the legal and compensation costs.

6. Emergency Evacuation and Repatriation

If you face a serious medical emergency or a natural disaster during your trip, you might need to be moved to the nearest hospital or sent back to your home country for treatment. This coverage ensures:

- Quick and safe transportation

- Coordination with medical providers

- Repatriation of mortal remains.

Example:During a volcanic eruption in Indonesia, you are airlifted to safety and flown back to your home country with the help of your insurer.

Optional Add-Ons and Specialized Policies

Depending on your travel style, consider these additional options:

- Adventure sports insurance: Covers injuries from skiing, scuba diving, rock climbing, etc.

- Cruise insurance: Includes shipboard medical care, missed ports, and evacuation from a cruise ship.

- Student insurance: Covers tuition refunds, academic interruption, and extended stays.

- Business travel insurance: Adds protection for laptops, presentation materials, and last-minute trip changes.

- Rental car insurance: Protects against vehicle damage, theft, and liability while driving abroad.

Travelers can usually customize these add-ons for each trip, and experts highly recommend them for specialized travel.

Regional Differences in Travel Insurance

1. North America

Travelers from the U.S. and Canada face some of the highest healthcare costs in the world. Consequently, comprehensive medical coverage is essential. Domestic travel insurance is also popular, especially during hurricane season.

2. Europe

European travelers often rely on the European Health Insurance Card (EHIC), but it only offers limited protection. For non-EU travelers or visitors to Europe, travel insurance with medical and liability coverage is essential. Schengen visa applicants must have a minimum of €30,000 in medical coverage.

3. Asia-Pacific

Travel insurance is gaining popularity as outbound tourism continues to increase. Many destinations, including Thailand and Japan, now require travelers to have insurance for certain visa types. Some countries have healthcare agreements with Australia; however, experts still recommend purchasing private travel insurance.

4. Middle East

The UAE, Saudi Arabia, and Qatar often require proof of insurance for visa issuance. Travel insurance is crucial due to the high cost of private healthcare.

5. Africa

Due to limited access to healthcare in many areas, travelers to Africa should prioritize emergency evacuation and repatriation coverage. Political instability in some countries also makes trip cancellation and interruption coverage important.

How to Choose the Right Travel Insurance?

Consider the following when selecting a policy:

- Destination requirements: Does the country mandate insurance?

- Trip duration: Short trips need basic coverage; longer trips need extended benefits.

- Activities: Are you engaging in sports, trekking, or volunteering?

- Health conditions: Declare all pre-existing conditions and check coverage eligibility.

- Coverage limits: Ensure sufficient medical and baggage loss coverage.

- Claim process: Choose insurers with easy online claims and global customer support.

If you face a serious medical emergency or a natural disaster during your trip, you might need to be moved to the nearest hospital or sent back to your home country for treatment.

Common Exclusions to Watch Out For

Even the best policies have exclusions. Be aware of:

- Ignoring government travel advisories

- Undisclosed pre-existing conditions

- Injuries under the influence of drugs/alcohol

- High-risk sports not listed in your policy

- Self-inflicted injuries or illegal activities.

Always read the details carefully to avoid unexpected problems during emergencies.

Travel Insurance in a Post-Pandemic World

COVID-19 changed global travel forever. Today’s travelers look for flexibility and pandemic-related protections. Most insurers now offer:

- Coverage for trip cancellation due to infection

- Reimbursement for quarantine expenses

- Telemedicine and remote medical consultations

Some insurers provide Cancel For Any Reason (CFAR) coverage, which lets you cancel your trip for nearly any reason and still get back up to 75% of your prepaid costs, even if the regular policy does not cover it.

Leading Travel Insurance Providers

Here are some reputable global insurers:

| Company | Best For | Key Features |

| World Nomads | Adventurous and long-term travelers | Covers 150+ activities, extendable plans, great for digital nomads |

| Allianz Global Assistance | Frequent international travelers | Comprehensive coverage, 24/7 support, strong medical and cancellation coverage |

| Travel Guard (AIG) | Customizable family/business plans | Trip interruption, baggage, and medical; app-based support |

| Travelex Insurance Services | Family vacations | Free child coverage, trip cancellation, medical and baggage coverage |

| AXA Assistance USA | Budget-conscious travelers | Global reach, affordable plans, strong evacuation and medical benefits |

| Berkshire Hathaway (BHTP) | Fast claims & tech-savvy users | Immediate digital payouts, pre-existing condition coverage |

| Seven Corners | Expats, students, frequent flyers | High medical coverage, multilingual support, strong evacuation features |

| IMG (International Medical Group) | Students and international trips | Customizable medical plans, long-term travel, study abroad options |

| Tin Leg | Strong medical benefits | High medical limits, comprehensive trip protection, value for money |

Here are some reputable Indian insurers:

| Company | Best For | Key Features |

| ICICI Lombard | Quick service, general use | Easy claims, global tie-ups, covers students, seniors, and family trips |

| Tata AIG | Senior citizens, students | Add-on flexibility, good network hospitals, student-specific benefits |

| Bajaj Allianz | Budget-friendly coverage | Affordable premiums, group policies, decent international coverage |

| HDFC ERGO | All-rounder | Strong global network, flexible plans, baggage/trip delay cover |

Final Thoughts

Travel insurance is not just an accessory—it is a travel essential. From medical emergencies to trip cancellations, the right policy offers protection and peace of mind. As global travel evolves, so do the risks. Being informed and insured ensures you can focus on what truly matters: enjoying your journey.

Whether you are a student heading abroad, a family going on vacation, or a digital nomad working remotely, travel smart—travel insured.

Frequently Asked Questions (FAQs)

Q1. Is travel insurance mandatory for international travel?

Answer: It depends on the destination. Some countries, like those in the Schengen area, require insurance for visa approval.

Q2. Can I buy travel insurance after departure?

Answer: Some insurers allow this, but it often comes with limited benefits and waiting periods.

Q3. Is COVID-19 covered by travel insurance?

Answer: Yes, most providers now include COVID-19 treatment and quarantine-related expenses, but coverage varies.

Q4. How much does travel insurance cost?

Answer: Typically, travel insurance costs around 4% to 10% of your total trip expenses, depending on factors like your destination, age, coverage type, and trip duration.

Q5. How do I make a claim abroad?

Answer: Use the insurer’s website, mobile app, or 24/7 helpline. Keep receipts, medical reports, and official documents for future reference and as proof of documentation.

Recommended Articles

We hope this article on travel insurance helps you plan safer and more stress-free trips. For more insights on travel planning and protection, check out: