What Is a Collecting Banker?

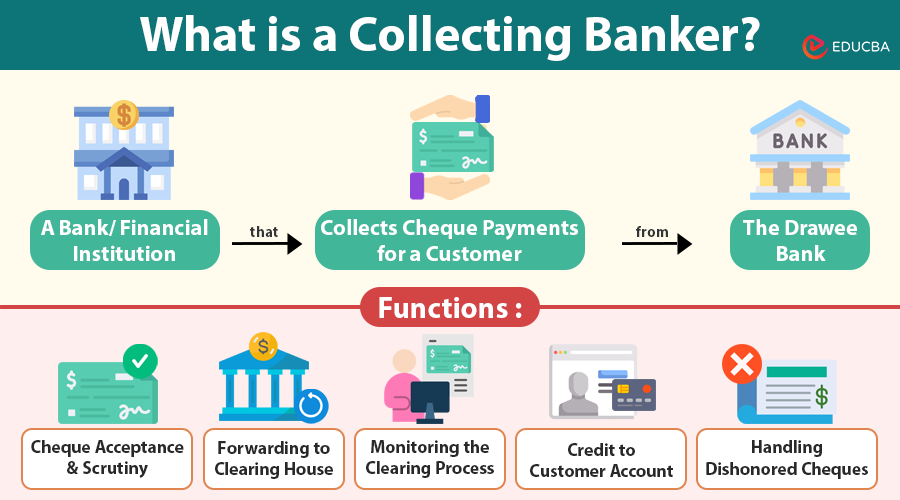

A collecting banker is a bank or financial institution that receives a cheque or negotiable instrument from a customer and works to collect the amount from the bank on which it is drawn (called the paying bank).

Suppose you deposit a cheque issued by someone with an HDFC Bank account into your SBI account. SBI becomes the collecting banker. It will approach HDFC Bank (the paying banker) to collect the funds and credit your account.

Table of Contents

- Meaning

- Where do you encounter?

- Functions

- Legal Protection

- Rights

- Risks

- Collecting banker vs. paying banker

- Digital advancement

- Special cases

- Tips

Key Takeaways

- A collecting banker collects cheques on behalf of customers from paying banks.

- Key duties include verifying cheques, sending them for clearing, and crediting accounts.

- Section 131 gives legal protection to collecting bankers if they act honestly and carefully without being careless.

- Rights include lien over funds, charging fees, and acting as an agent.

- Risks involve forgery, dishonor, and liability for negligence.

- Digital tools, such as the Cheque Truncation System (CTS), have sped up and secured the process.

Where Do You Encounter Collecting Bankers?

- Salary cheques deposited into savings accounts

- Small business owners receiving client payments by cheque

- Government refund cheques (e.g., income tax refund)

- Inter-city business transactions

- Outstation cheque deposits.

Functions of a Collecting Banker

A collecting banker does more than deposit cheques. Here is a deeper look:

1. Cheque Acceptance and Scrutiny

The banker first checks:

- Whether the cheque is current (not stale or post-dated)

- Proper signatures and endorsements

- Amount in words and figures match

- Account holder details are correct

2. Forwarding to Clearing House

If the cheque is from a different bank, the collecting banker sends it to the clearing house system. In urban areas, this is done electronically through the Cheque Truncation System (CTS).

3. Monitoring the Clearing Process

The banker tracks whether the cheque has been honored or dishonored and updates the customer accordingly.

4. Credit to Customer Account

Once the cheque clears, the bank usually credits the amount to the customer’s account within 1 to 2 working days for local cheques.

5. Handling Dishonored Cheques

If the cheque bounces, the collecting banker notifies the customer and returns the instrument. Banks may also charge a fee for cheque returns.

Did You Know?

The RBI mandates banks to clear cheques deposited in local branches within T+1 days under the Cheque Truncation System (CTS).

Legal Protection of Collecting Bankers (Section 131 of NI Act)

Section 131 of the Negotiable Instruments Act of 1881 protects collecting bankers if they follow due care.

Conditions for Protection:

- The cheque is crossed (i.e., not payable over the counter).

- The collection is done for a bank customer.

- The collection is made in good faith and without negligence

- The banker acts as an agent, not as the owner.

When Is This Protection Lost?

If the banker:

- Fails to verify the customer’s identity

- Ignores suspicious signs (e.g., forged endorsements)

- Collects a cheque for a non-account holder

- Does not follow KYC norms.

Case Study: Canara Bank vs Canara Sales Corp (1987)

The bank collected a cheque for a fake customer. The court held the bank liable for negligence and denied protection under Section 131.

Rights of a Collecting Banker

Collecting bankers enjoy some important rights, especially when acting in good faith:

- Right of lien: If a customer owes money to the bank, the bank can retain the proceeds of a collected cheque to offset the dues.

- Right to charge collection fees: Outstation cheques or international instruments may incur service charges, especially when courier or correspondence services are involved.

- Right to act as agents: Banks act as agents, not owners of the cheques. This means they are not liable for losses unless negligence is proven.

Risks Faced by Collecting Bankers

Collecting bankers face real risks despite legal protection, especially if internal checks are weak.

- Forgery and fraud: If a customer deposits a forged cheque and the banker fails to detect it, the bank may suffer financial and reputational losses.

- Stale and post-dated cheques: Cheques older than 3 months (stale) or dated in the future (post-dated) can create disputes or bounce.

- Improper endorsements: A mismatch can result in liability in business accounts where cheques are endorsed multiple times.

- Dishonor risk: If the paying bank refuses to honor the cheque (e.g., due to insufficient funds), it causes operational delays and customer dissatisfaction.

Collecting Banker vs Paying Banker

| Feature | Collecting Banker | Paying Banker |

| Role | Collects cheque for customer | Pays cheque issued by account holder |

| Relationship with Cheque | Acts as agent | Acts as principal (holds the funds) |

| Legal Protection | Section 131 of NI Act | Section 85 of NI Act |

| Checks for | Endorsements, validity, customer KYC | Signature, sufficient funds, stop payment |

| Risk of Negligence | Yes – if KYC and scrutiny are not done properly | Yes – if payment is made on irregular cheques |

Digital Advancements: Cheque Truncation System (CTS)

The RBI introduced the Cheque Truncation System in 2010. It eliminates the need for physical checks to transfer funds between banks.

Features of CTS:

- Cheque image is scanned and sent electronically

- Verification and clearing happen digitally

- Increases speed and reduces fraud.

Real-World Stats:

- Over 90% of cheque clearing in India now uses CTS

- Average clearing time dropped from 3 days to 1 day

- Banks saved over ₹2,000 crore annually in courier and logistics costs (as per RBI data).

Special Cases

Foreign Cheques

Collecting bankers also collect cheques drawn in foreign currencies. These go through correspondent banks and may take 15-30 days.

Outstation Cheques

If someone draws a cheque in a different city, the bank sends it to that branch. This involves:

- Courier delays

- Charges ranging from ₹50 to ₹200

- Additional risk if postal systems fail.

Tips for Customers to Help the Collecting Banker

- Cross your cheque with two lines and write “A/C Payee Only”

- Do not deposit post-dated or stale cheques

- Use your full account name for endorsements

- Write your phone number behind the cheque in case of issues

- Track collection status via mobile banking or email alerts.

Final Thoughts

Collecting bankers are vital players in the banking ecosystem. Though their role may appear administrative, it carries significant financial and legal responsibilities. From handling routine salary cheques to cross-border instruments, their function keeps the wheels of commerce moving.

Understanding how collecting bankers operate builds financial awareness and helps customers avoid errors and delays. As banking becomes increasingly digital, the role continues to evolve; however, due diligence, responsibility, and good faith will always remain at its core.

Frequently Asked Questions (FAQs)

Q1. What happens if the cheque is dishonored after the amount has been credited?

Answer: If the cheque is dishonored after the bank credits the amount to your account, the bank reverses the credited amount and may charge a dishonor fee. You are responsible for any overdraft created due to this reversal.

Q2. Can collecting bankers be held liable for delays in cheque collection?

Answer: Yes, if negligence on the part of the collecting banker causes undue delays, they may be held liable for any losses incurred by the customer.

Q3. How does the collecting banker handle cheques drawn on foreign banks?

Answer: Collecting foreign cheques involves correspondent banking arrangements, longer clearing times, currency conversion, and additional fees. The collecting banker usually informs customers about the expected timelines.

Q4. What documentation is required when depositing a cheque with a collecting banker?

Answer: Typically, customers need to provide a duly filled deposit slip and may need to produce identification if required by the bank’s KYC norms.

Recommended Articles

We hope this article has clarified the role of a collecting banker and their legal responsibilities. Check out the recommended articles below to learn more about banking procedures, cheque handling, and financial best practices.