What Is Shadow Banking?

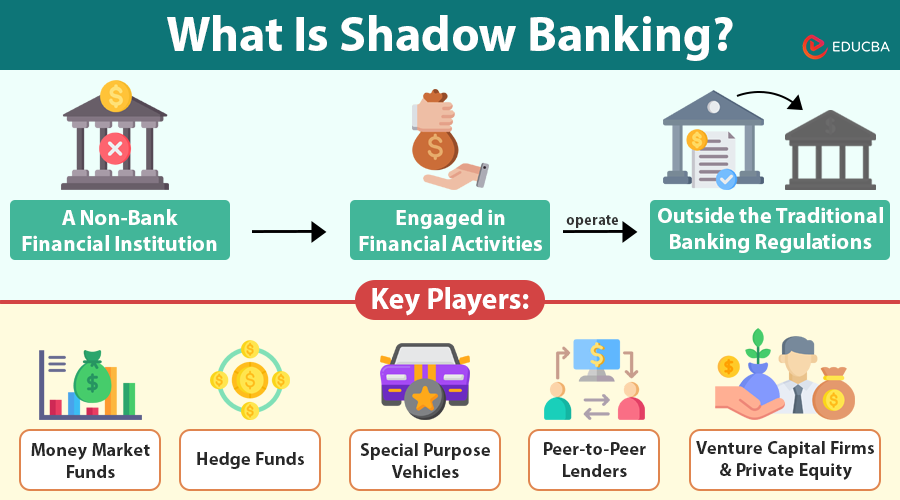

Shadow banking refers to the network of non-bank financial institutions that engage in activities traditionally associated with banks, such as lending and investing, but operate outside traditional banking regulations. Coined by economist Paul McCulley in 2007, the term has often sparked concern due to its lack of oversight, yet it is an integral part of the modern financial system. These entities do not accept deposits like traditional banks, but they still facilitate credit and liquidity in the market. Shadow banks include hedge funds, money market funds, investment banks, mortgage lenders, and structured investment vehicles (SIVs).

Example:

Lily is a small business owner in the food delivery industry. When the pandemic struck, her business experienced a significant decline in revenue due to lockdown restrictions. After failing to secure a loan from traditional banks, Lily turned to a P2P lending platform, which connected her directly with investors ready to fund her short-term loan. This loan enabled Lily to keep her business running, pay her employees, and transition to a delivery-only model. By the end of the pandemic, Lily’s business not only survived but also experienced growth as demand for food delivery surged.

How Shadow Banking Works?

Outside traditional banking regulations, shadow banking primarily revolves around financial intermediation—borrowing, lending, and investing. The process typically works as follows:

- Origination of Credit: Financial institutions within the shadow banking sector originate credit by pooling funds from investors.

- Securitization: Once the institution creates the credit, it often securitizes it, packaging it into securities and selling them to investors in global markets.

- Leverage: These institutions often employ higher leverage than traditional banks, utilizing borrowed funds to amplify returns.

- Disintermediation: In this process, shadow banking bypasses traditional intermediation, such as the role of commercial banks, and provides an alternative avenue for credit creation and liquidity.

Key Players in Shadow Banking

Some of the key players include:

- Money Market Funds (MMFs): Investors seeking low-risk returns often utilize these funds to invest in short-term debt instruments. They can also be a source of credit for borrowers.

- Hedge Funds: Hedge funds provide loans and credit, often investing in higher-risk assets, such as distressed debt, private equity, and complex derivatives.

- Special Purpose Vehicles (SPVs): Companies create SPVs for specific financial transactions, such as asset-backed securities, to isolate risk from the parent company.

- Peer-to-Peer (P2P) Lenders: These online platforms match borrowers with individual lenders, bypassing traditional banks and offering unsecured loans.

- Venture Capital Firms and Private Equity: These firms provide financing to businesses but are not subject to the same regulations as traditional banks.

Why Does Shadow Banking Exist?

Shadow banking plays a crucial role in the modern financial system:

- Alternative Credit Supply: Shadow banking offers an alternative source of credit to borrowers who may not qualify for traditional bank loans. It can support individuals, small businesses, and startups that have difficulty accessing traditional bank financing.

- Liquidity Enhancement: These institutions enhance market liquidity, especially when traditional banks are reluctant to lend. By facilitating the flow of money between borrowers and investors, they ensure the smooth functioning of financial markets.

- Efficient Capital Allocation: Shadow banks often invest in sectors or regions that traditional banks overlook. This approach directs capital toward productive uses that might not receive funding through traditional channels.

Key Differences Between Traditional Banks and Shadow Banking

While traditional banks and shadow banking institutions are involved in credit creation, they differ significantly in structure and regulation. Let us explore the key differences:

| Aspect | Traditional Banks | Shadow Banking |

| Regulation | Heavily regulated by central banks and governments | Operates outside traditional banking regulations |

| Primary Function | Accepting deposits, offering loans, and managing payments | Lending, investing, and creating financial products |

| Transparency | High level of transparency and oversight | Low transparency and limited oversight |

| Risk Management | Subject to capital requirements and liquidity ratios | No stringent capital or liquidity requirements |

| Access to the Central Bank | Direct access to central bank resources | No access to central bank liquidity |

Case Study: The 2008 Financial Crisis

The global financial crisis in 2008 provides a clear example of the risks associated with shadow banking. Leading up to the crisis, many shadow banks were heavily involved in securitizing subprime mortgages. Investors, including large institutional players, bought these financial products, believing they were low-risk investments.

However, when the housing bubble burst and mortgage defaults skyrocketed, the value of these securities plummeted, causing significant losses. As many institutions in the shadow banking sector lacked the same level of oversight as traditional banks, they encountered a liquidity crisis when they were unable to fulfill their obligations. This led to a domino effect, resulting in widespread financial instability.

Risks of Shadow Banking

While shadow banking offers the potential for higher returns, it also brings substantial risks. Some key risks include:

- Liquidity Risk: Shadow banks often rely on short-term borrowing to fund long-term investments. They may face liquidity crises if they cannot roll over their short-term debt during market stress.

- Systemic Risk: The interconnectedness of shadow banks with the broader financial system can lead to systemic risks. If one major player fails, it can trigger a cascade of failures in related institutions, much like during the 2008 financial crisis.

- Lack of Transparency: Since shadow banks operate outside the regulatory framework, their operations often lack transparency. This makes it difficult for investors, regulators, and the public to assess the risks.

- Moral Hazard: Since shadow banks operate outside the regulatory boundaries imposed on traditional banks, there is a moral hazard that they might engage in excessive risk-taking, knowing they are not held to the same penalties or capital requirements.

Regulation and Oversight

In response to the 2008 crisis, some global and national regulators have implemented or proposed measures to reduce the risks, as follows:

- The Financial Stability Board (FSB): In 2011, the FSB introduced the “Shadow Banking Monitoring Report” to track the size and risk levels of shadow banking worldwide. The board monitors the sector’s growth and potential risks to the global financial system.

- Enhanced Transparency: Regulators have pushed for more transparency in shadow banking activities. For example, financial institutions must now disclose more information about their investments in certain asset classes.

- Capital Requirements: Regulatory bodies are working to implement stricter capital requirements for shadow banks, ensuring they have sufficient buffers in place to withstand financial shocks.

- Systemic Risk Oversight: Regulators have intensified their surveillance of institutions that could be “too big to fail” or pose a systemic risk to the financial system if they collapse.

Global Growth of Shadow Banking

The Financial Stability Board reported that in 2020, the global shadow banking sector held an estimated value of around $60 trillion, accounting for nearly 40% of all global financial assets. While this growth reflects the increasing demand for alternative financial services, it also raises alarms about the risks associated with this large, under-regulated sector.

- United States: Shadow banking has been particularly prominent in the U.S. since the 2008 financial crisis. People often link it to the securitization of mortgages, student loans, and auto loans. As of 2020, the U.S. shadow banking market stood at approximately $22 trillion.

- China: Shadow banking in China has grown rapidly, driven by the government’s efforts to curb credit growth in the formal banking sector while promoting the expansion of non-bank credit providers. In China, the banking sector reached a value of $10 trillion in 2017.

Final Thoughts

Shadow banking is a crucial yet complex component of the global financial system. While it offers increased access to credit, innovative investment products, and greater market liquidity, it also brings significant risks, especially concerning systemic stability and regulatory challenges. As shadow banking continues to grow, regulators must address these risks without stifling the sector’s ability to innovate. Financial institutions, investors, and governments must work together to ensure that the banking sector remains a positive force in the global economy, mitigating potential risks while maintaining its benefits.

Recommended Articles

We hope this article on shadow banking provides you with valuable insights into this often-overlooked sector. Check out these recommended articles for a deeper understanding of financial systems and alternative investment options.