What is Branchless Banking?

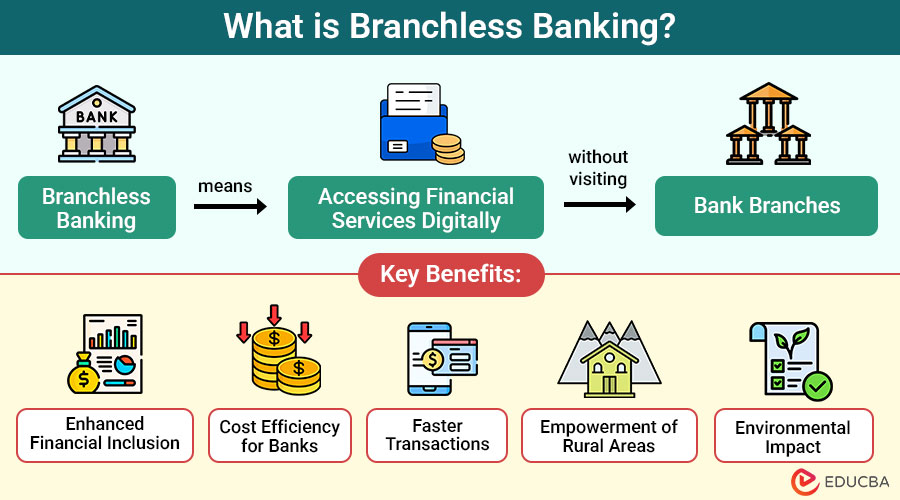

Branchless banking is a financial service delivery model that let customers to perform banking transactions without visiting physical branches, using digital platforms, mobile apps, ATMs, or authorized agents for convenient and remote access.

For example, a customer uses a mobile banking app to check their account balance, transfer money to a friend, and pay a utility bill — all from home, without visiting a bank.

Table of Contents:

- Meaning

- Working

- Why is it Popular?

- Key Benefits

- Challenges

- Role of Technology

- Future

- Tips for Safe Use

Key Takeaways:

- Branchless banking eliminates the need for physical branches by using digital platforms and local agents.

- It promotes financial inclusion, especially in rural and underserved communities.

- Mobile technology and agent networks form the foundation of the branchless banking model.

- Challenges such as digital illiteracy, security, and connectivity require strategic attention and consideration.

How Branchless Banking Works?

The core principle of branchless banking is leveraging technology to bridge the gap between financial institutions and customers. Here is a breakdown of its typical infrastructure:

1. Mobile Banking Platforms

Customers may pay bills, transfer money, and check balances without going to a bank thanks to smartphone apps and SMS-based services.

2. Banking Agents

Agents or business correspondents serve as the bank’s primary point of contact. Located in small shops, post offices, or standalone kiosks, they enable people to conduct basic banking activities with the aid of handheld devices or tablets.

3. ATMs and Kiosks

Automated Teller Machines and biometric-enabled kiosks are installed in public places to allow 24/7 access to cash withdrawals and other banking services.

4. Internet and USSD Services

For areas with internet access, customers can use online portals. In rural areas with limited connectivity, Unstructured Supplementary Service Data (USSD) codes offer a straightforward way to access banking services using feature phones.

5. POS Terminals

Used by merchants or banking agents, POS machines help users swipe cards and perform transactions, even in remote markets.

Why Branchless Banking is Gaining Popularity?

Several factors are fueling the rise of branchless banking:

1. Cost Reduction

Branchless banking significantly reduces the high operational costs associated with building, staffing, and maintaining physical branches by relying on digital infrastructure and agent-based services instead.

2. Wider Reach

It enables financial institutions to deliver services to remote, unbanked, and underbanked regions where establishing traditional bank branches would be impractical or economically unsustainable.

3. Convenience

Customers enjoy improved access to financial services, eliminating the need to wait in lines or travel long distances, making banking easier, faster, and more user-friendly.

4. Financial Inclusion

Branchless banking empowers underserved populations by providing them with access to essential financial tools, such as savings accounts, microloans, insurance, and payment systems, that were previously unavailable to them.

5. Digital Transformation

Branchless banking uses digital tools to improve financial services and reach larger demographics as mobile phone usage and internet connectivity increase.

Key Benefits of Branchless Banking

Here are the major key benefits that make branchless banking a transformative approach to delivering financial services:

1. Enhanced Financial Inclusion

Branchless banking provides a gateway to the financial system for millions who were previously excluded due to distance, income, or documentation requirements.

2. Cost Efficiency for Banks

Banks save money on overhead, allowing them to scale their reach and focus more resources on service and innovation.

3. Faster Transactions

Branchless banking enables customers to perform real-time transactions instantly, eliminating the need to wait at bank counters.

4. Empowerment of Rural Areas

Agents from local communities build trust and foster familiarity, while also boosting local employment and entrepreneurship.

5. Environmental Impact

Reducing reliance on physical infrastructure lessens paper usage and energy consumption.

Challenges in Branchless Banking

Despite its advantages, branchless banking has several obstacles to overcome:

1. Digital Literacy

Many rural or underserved users lack the digital skills or confidence needed to navigate mobile apps, USSD codes, or online banking platforms, limiting their ability to use services effectively.

2. Connectivity Issues

Remote or underdeveloped areas often suffer from poor mobile network coverage or limited internet access, making it difficult to perform consistent and reliable, branchless banking transactions through digital platforms.

3. Security Concerns

First-time or less tech-savvy users are particularly vulnerable to digital threats, including phishing, identity theft, and cyberattacks, which necessitate robust education and security protocols from service providers.

4. Agent Reliability

Agents may face liquidity problems, charge unauthorized fees, or misuse customer data. Regular monitoring, training, and support are crucial for maintaining trust and ensuring service quality.

5. Regulatory Hurdles

Complex or inconsistent regulations regarding customer verification, transaction limits, and licensing requirements across regions can restrict the seamless implementation and expansion of branchless banking models.

Role of Technology in Branchless Banking

Technology is the backbone of branchless banking. Here is how it empowers the system:

1. Cloud Banking

Cloud banking enables financial institutions to provide scalable, secure, and cost-effective digital services without incurring significant investments in physical infrastructure or traditional data centers.

2. Biometric Authentication

Particularly in nations like India, where a large number of people use banking services connected to Aadhaar, biometric technology, such fingerprint or iris scans, safely and easily verify customers.

3. AI and Machine Learning

Artificial intelligence helps detect fraudulent activities, evaluates customer credit profiles, and streamlines support services, thereby enhancing operational efficiency and decision-making in branchless banking platforms.

4. Blockchain

Blockchain technology increases transparency, minimizes fraud, and secures transaction records, making it especially valuable for cross-border payments and decentralized financial applications in branchless banking.

5. Chatbots and Voice Banking

Chatbots and voice interfaces offer user-friendly, accessible banking support, especially for customers with low digital literacy or limited ability to use traditional mobile apps.

Future of Branchless Banking

The future of banking is branchless, paperless, and cashless. As AI, 5G, and financial technologies evolve, branchless banking will continue to:

1. Integrate with Super Apps

Branchless banking will merge with super apps that combine payments, shopping, social media, and other digital services seamlessly.

2. Include Voice-Enabled Services

Voice-based banking will enhance accessibility for users with limited literacy or technical skills, facilitating easier interactions and financial transactions.

3. Expand into Decentralized Finance

Branchless banking may adopt DeFi technologies to offer secure, transparent, and alternative financial services beyond traditional banking models.

4. Collaborate with Fintech Startups

Increased collaboration with fintech startups will drive innovation, creating user-centric solutions tailored to modern financial needs and market gaps.

Tips for Safe Use of Branchless Banking

Here are the essential safety tips to protect your finances while using branchless banking services:

1. Never Share Credentials

To avoid unwanted access and shield your account from fraudulent activity, keep your PIN, OTP, and login information confidential.

2. Use Official Channels Only

Always use verified banking apps or authorized agents to ensure secure and trustworthy transactions without the risk of fraud.

3. Collect Confirmation Messages

After every transaction, collect and verify the receipt or SMS confirmation to ensure your transaction was successful and properly recorded.

4. Report Suspicious Activity Immediately

If you notice unauthorized activity, contact your bank immediately to block access and prevent further fraudulent transactions on your account.

5. Stay Informed on Safety Practices

Educate yourself and your community about digital banking safety to reduce risks and promote responsible, secure financial behavior online.

Final Thoughts

Branchless banking is not just a trend—it is a transformation. It is reshaping how people interact with money, especially those who were previously sidelined by conventional systems. A more empowered, inclusive, and financially literate world could be created as it develops further, propelled by policy changes and technology breakthroughs.

Frequently Asked Questions (FAQs)

Q1. Is branchless banking safe?

Answer: Yes, as long as users follow basic security practices like not sharing PINs or OTPs and using verified platforms. Banks also use encryption and multi-factor authentication for protection.

Q2. How do branchless banking systems handle customer service?

Answer: Support is often provided through call centers, in-app chatbots, or directly by agents. Some advanced systems also offer AI-powered virtual assistants and multilingual support to help customers resolve issues quickly.

Q3. What if I do not have a smartphone?

Answer: Branchless banking is not limited to smartphones. USSD codes and agent kiosks make it accessible even to users with basic mobile phones.

Q4. How do branchless agents earn money?

Answer: Agents typically earn commissions from banks or mobile money operators for each transaction they perform on behalf of customers.

Recommended Articles

We hope that this EDUCBA information on “Branchless Banking” was beneficial to you. You can view EDUCBA’s recommended articles for more information.