Introduction to Unbanked

Despite significant advances in financial technology, including digital wallets, credit scores, and investment apps, over 1.4 billion people worldwide still lack access to basic banking services. These individuals lack access to regular banking services, which not only reduces their ability to improve their financial situation but also makes it harder for them to live safe and independent lives. This article explores who the unbanked are, why they remain excluded, and how we can address this issue, not just through banks and governments but also through technology, communities, and conscious consumers like you and me.

Table of Contents

- Meaning

- Reasons for Unbanked

- Consequences

- Digital Divide

- Exclusion

- Positive Examples

- Innovative Solutions

- Call to Action

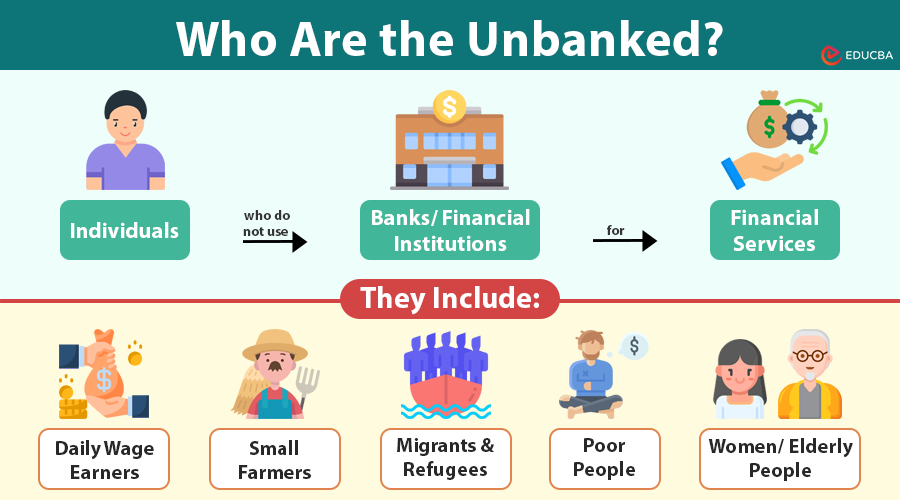

Who Are the Unbanked?

The unbanked are individuals who do not use banks or financial institutions for basic financial services.

They include:

- Daily-wage earners who deal only in cash.

- Small-scale farmers without access to credit or crop insurance.

- Migrants and refugees who lack the paperwork needed to open an account.

- Urban poor living in slums where banks do not operate.

- Women and the elderly who face systemic barriers to financial inclusion.

Even in developed nations like the United States, some individuals remain unbanked due to historical marginalization, mistrust, or low income. For example, people from racial minority groups and those without legal documents are more likely to be left out of regular banking services.

Why Are People Unbanked?

Let us dig deeper into the reasons behind financial exclusion. These are not just individual issues—they are often systemic and structural in nature.

1. Lack of Access

In many rural areas, banks are too far away. Public transport may be infrequent or expensive, and opening hours may clash with working hours. Moreover, many villages still lack mobile networks, let alone internet access.

2. Lack of Documentation

Billions of people worldwide lack government-issued identification, including birth certificates and passports. For many, especially women and refugees, this invisibility in the system keeps them permanently excluded.

3. Cost of Banking

Banking fees, such as monthly maintenance charges, minimum balance penalties, and ATM surcharges, can discourage low-income individuals. Some have been penalized for simply not using their accounts, which has led to mistrust and disengagement.

4. Mistrust in Institutions

In areas affected by conflict or economic crises, people have lost their savings due to sudden currency devaluations or bank collapses. Such experiences breed a deep-seated mistrust of formal institutions.

5. Financial Illiteracy

Financial education is not a part of school curricula in many developing nations. People often do not understand the terms, benefits, or risks of financial products. Predatory lending and hidden fees further discourage trust.

6. Cultural and Religious Beliefs

In some conservative communities, women need male permission to open accounts or own property. Additionally, interest-based financial products are forbidden in Islamic finance, making Sharia-compliant banking essential for inclusion.

Consequences of Being Unbanked

Being unbanked limits not just financial growth but also basic life opportunities.

1. No Access to Credit or Loans

Without credit histories or collateral, unbanked individuals cannot get loans for:

- Starting a small business

- Paying for children’s education

- Investing in a home or farm equipment.

This perpetuates generational poverty and dependence on informal or exploitative lenders.

2. Safety Risks

Storing large amounts of cash at home increases the risk of theft, fire, or loss. In areas with conflict or natural disasters, entire life savings can disappear in seconds.

3. Missed Economic Opportunities

Online freelancing, digital commerce, and app-based gig work are all inaccessible without a bank account or digital wallet. The modern economy excludes the unbanked.

4. Costly Alternatives

Informal services, such as payday loans, money lenders, or pawn shops, often charge interest rates of 100-400% annually, trapping people in cycles of debt.

5. Intergenerational Impact on Education and Opportunity

When parents are unbanked, their children face indirect barriers to upward mobility:

- No access to student loans or digital scholarships

- Limited ability to pay school fees on time

- No savings for higher education.

The Digital Divide and the Unbanked

Most financial inclusion efforts rely on mobile banking apps and online verification systems. However, that assumes people:

- Own smartphones

- Have reliable electricity

- Understand app interfaces

- Are literate in the dominant languages.

This “digital-first” approach can unintentionally deepen financial exclusion for those on the margins.

Gender and Financial Exclusion

Women face double discrimination—as poor individuals and as females. Barriers include:

- Lack of national ID cards

- No mobile phone ownership

- Social restrictions on mobility

- Being denied inheritance or property rights.

Positive Examples: What is Working?

1. M-Pesa (Kenya)

Using simple SMS technology, M-Pesa allows users to send, receive, and save money via mobile phones. According to MIT researchers, it reduced poverty by 2%.

2. Jan Dhan Yojana (India)

With biometric-linked accounts and no minimum balance requirements, this initiative enabled direct benefit transfers for subsidies and pensions, reducing leakage and corruption.

3. Banco Palmas (Brazil)

This community bank offers a local currency (Palmas) and micro-loans, building economic resilience in favelas (urban slums).

4. GiveDirectly (Africa)

This NGO provides unconditional cash transfers via mobile money to people in extreme poverty. Studies show better nutrition, education, and health outcomes among recipients.

Innovative Solutions for the Future

Going beyond the basics, here are next-generation ideas that could reshape inclusion:

1. Biometric-Only Banking

Fingerprints, facial recognition, or iris scans could let users open accounts without paperwork. India’s Aadhaar-linked banking system already uses this.

2. Offline Mobile Wallets

New tools, such as NFC-based payment cards or Bluetooth wallets, can operate without an internet connection, which is crucial for remote areas.

3. Voice-Based Interfaces

AI-powered voice commands in local dialects allow the illiterate or visually impaired to access financial services securely.

4. Community-Led Banking

Training local women or youth as banking agents can help extend banking services to previously unbanked regions, using trust as a bridge.

5. Cryptocurrency and Stablecoins

While volatile, cryptocurrencies can be lifesavers in countries with unstable economies or capital controls. Stablecoins pegged to real-world currencies may offer a safer entry point.

What Can Be Done?

Governments Should

- Digitize and simplify ID issuance

- Promote financial education from schools to villages

- Regulate digital lenders and protect users.

Banks Should

- Create zero-fee, mobile-first accounts

- Accept alternative credit histories like utility bills or mobile recharges

- Translate services into local languages and voice formats.

Fintech Startups Should

- Focus on user-centric design

- Avoid assuming high digital literacy

- Partner with NGOs and grassroots leaders.

NGOs and Civil Society Should

- Run financial literacy programs

- Facilitate trust between communities and banks

- Advocate for policy changes on behalf of the unbanked.

Individuals Can

- Teach someone how to use a digital wallet

- Volunteer in financial education programs

- Support inclusive businesses.

Final Thoughts

Being unbanked is not a personal failure. It is often the result of broken systems, historical inequities, and blind spots in the global financial system. However, change is possible.

We must design inclusive systems that respect local cultures, require minimal resources, and value human dignity. Financial inclusion is not just a policy goal—it is a fundamental right and a powerful tool for justice, growth, and peace.

Frequently Asked Questions (FAQs)

Q1. Are the unbanked the same as the underbanked?

Answer: No. The unbanked have no access to traditional banking services at all. In contrast, underbanked individuals often have a bank account, such as a savings account, but they still utilize alternative financial services, including money orders, payday loans, or check-cashing services.

Q2. What is the role of postal banks in financial inclusion?

Answer: Postal banks use existing postal infrastructure to offer basic banking services in rural or underserved areas. Countries like Japan and India have effectively utilized this model to reach unbanked populations without the need for new branches.

Q3. Do the unbanked pay more for basic services?

Answer: Often, yes. Without access to digital payments or credit, unbanked individuals may incur additional costs, such as cash handling fees, transportation expenses for paying bills, or higher interest rates from informal lenders.

Q4. How do disasters and pandemics affect unbanked populations?

Answer: In times of crisis, unbanked individuals often lack access to government relief payments, insurance, or digital donations. This worsens their recovery and exposes them to greater risks.

Recommended Articles

We hope this article has helped you understand who the unbanked are and why financial inclusion matters. Explore the recommended articles below to learn more about inclusive banking, digital finance solutions, and efforts to close the financial gap.