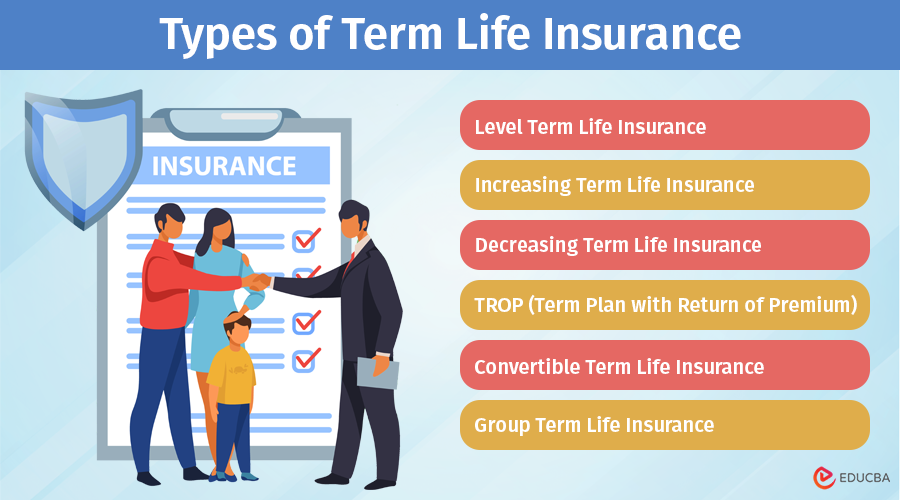

Types of Term Life Insurance Plans in India

Term insurance is a very popular form of life insurance in India. It is one of the most sold plans because it offers exactly what people need – maximum coverage at minimum cost. The term plans are handy with their flexible features and widespread benefits. There are several types of term life insurance available for you to choose from.

#1. Level Term Life Insurance

It is the standard form of term insurance where there is level or equal coverage throughout the term of the policy.

If you buy an INR 1 crore term plan, after five years, the coverage will remain the same.

If you pass away at any time within the policy period, your family will get the same payout without any deductions or additions. If you outlive the policy period, you will not get anything in return, and the policy will end. It is the most common, one of the best term life insurance options, and the least expensive.

#2. Increasing Term Life Insurance

Here, as the name suggests, the coverage amount increases. An increasing term insurance plan is a type of term insurance where the coverage amount steadily and uniformly increases as your policy progresses.

It is a good investment if you have small children or other financial responsibilities requiring more coverage with time. As your child grows, their financial requirements will grow as well. You have to make provisions for their college admission, business set-up, marriage expenses, etc. An increasing term plan helps in such cases.

#3. Decreasing Term Life Insurance

Contrary to the increasing cover, a decreasing term insurance plan is a type of plan where your coverage amount steadily decreases as the policy progresses.

It is a good type of term insurance to cover loans and other liabilities. As you pay off your loan, the debt burden reduces as well, making your term insurance needs lower, too. Use a decreasing term plan to cover the loan appropriately for as long as you are paying for your loan.

#4. TROP (Term Plan with Return of Premium)

TROP stands for term insurance with return of premium. Usually, a term insurance plan does not have a return component. In other words, you do not get anything in return if you outlive the policy period.

However, in a TROP, you get the premium you paid through the tenure of the plan at the end of the term, provided you are still alive. It is more expensive than a regular term insurance plan, but it allows you to recover your money at the end of the coverage period.

#5. Convertible Term Life Insurance

If you want to convert your term insurance plan to a permanent life insurance policy like Whole Life or Universal Life, this is the plan for you. You will not need to go through a new medical exam.

It is ideal for those who want the flexibility to switch to permanent coverage later, perhaps when they have more disposable income or changing needs.

#6. Group Term Life Insurance:

Employees get this plan as a part of their employee benefits package. It offers limited coverage, and the policyholder has little control over the terms.

It is a good option for employees looking for a cost-effective way to obtain some life insurance coverage, though it may not be sufficient on its own.

How to Choose a Term Insurance Plan?

1. List Your Current Financial Requirements

You need to consider the financial requirements of the family when choosing a suitable term insurance plan.

For example, if you are taking a plan just to offer financial coverage to your loved ones, a level-term plan may suit you the best. If, however, you wish to protect your loans and mortgages, a decreasing-term plan will be a better option.

2. Consider Future Financial Requirements

You have to factor in the future financial requirements of your family members. Consider your child’s education expenses, your spouse’s retirement needs, etc., and then choose the best plan. You may need an increasing cover if there are many financial milestones to cover.

3. Factor in Other Family Income

Are you the only earning member of your family, or does your spouse also work? Do your parents get pensions? You will have to take the other income of the family into account when you finalize your term insurance coverage.

4. Budget for the Premium

Keep your finances in mind when you choose the ideal term insurance plan. Choose an affordable option. You should be able to comfortably pay the term insurance premium. Any lapses here may lead to the termination of term insurance benefits, so choose something that you can manage and keep your term coverage active.

5. Existing Loan Liability

Loans are a big reason why you must opt for term insurance. If you have many loans and don’t want the burden to fall on your family members after your demise, get suitable term insurance plans to cover the liabilities.

Final Thoughts

It is very important to get the right type of term insurance plan, as only then can you provide for your family after your demise. Term insurance offers a pure life cover, so if life coverage is your only aim, go for the best term life insurance policy and secure the well-being of your loved ones simply and conveniently.

Recommended Articles

We hope you found this article listing the types of term life insurance plans helpful. For more insurance-based blogs, read these.