Updated July 14, 2023

Definition of Tax Slabs

The tax is governed by the Indian Income Tax Act 1961. CBDT governs the Indian Income Tax Department and is part of the Department of Revenue under the Ministry of Finance, Govt. of India. Income tax is an important source of funds that the government uses to fund its activities and work for the public.

“Tax slabs are categories that tell the people how much tax they must pay according to their income level. Government uses the tax money for matters like social welfare, defense, and security.”

CBDT governs the Indian Income Tax Department and is part of the Department of Revenue under the Ministry of Finance, Govt. of India. Income tax is an important source of funds that the government uses to fund its activities and work for the public.

The Income Tax Department is the major revenue mobilizer for the Government. The total tax revenues of the Central Government are greater than before, from ₹ 1392.26 billion in 1997-98 to ₹ 5889.09 billion in 2007-08.

Income Tax Slabs & Rates for Assessment Year 2018-19

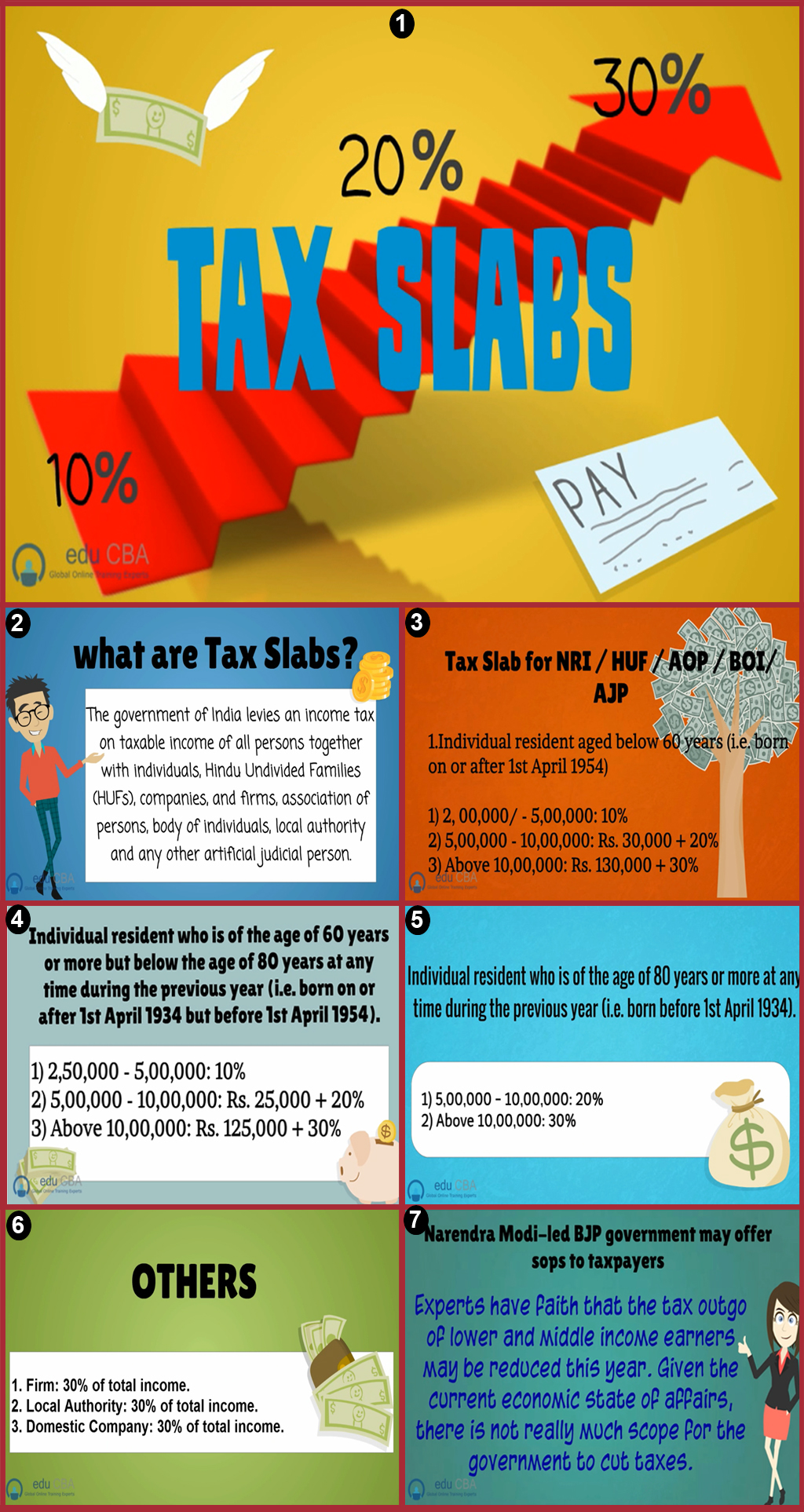

I. Individual resident aged below 60 years (i.e. born on or after 1st April 1954) or any NRI / HUF / AOP / BOI/ AJP( NRI – Non-Resident Individual; HUF – Hindu Undivided Family; AOP – Association of Persons; BOI – Body of Individuals; AJP – Artificial Judicial Person)

| INCOME SLABS | TAX RATES | |

| 1 | Where the total income does not surpass Rs. 2 00,000/-. | NIL |

| 2 | Where the total income surpasses Rs. 2, 00,000/- but does not surpass Rs. 5, 00,000/-. | 10% of the amount by which the total income goes beyond Rs. 2 00,000/-. Less: Tax Credit – 10% of taxable income up to a maximum of Rs. 2000/-. |

| 3 | Where the total income exceeds Rs. 5 00,000/- but does not surpass Rs. 10 00,000/-. | Rs. 30,000/- + 20% of the amount by which the total income goes beyond Rs. 5, 00,000/-. |

| 4 | Where the total income surpasses Rs. 10 00,000/-. | Rs. 130,000/- + 30% of the amount by which the total income goes beyond Rs. 10, 00,000/-. |

Surcharge: the surcharge is 10% of the Income Tax where the total taxable income is more than Rs. 1 crore. (Marginal Relief in Surcharge, if applicable).

Education Cess: It is 3% of the total Income Tax and Surcharge.

Example:

Mr. X has a total Income of Rs. 11 00,000. He is of 45 years of age. The calculation of his Tax Liability is as follows:

|

Income |

Tax |

|

First Rs. 2,00,000 |

NIL |

|

Rs. 2,00,000 to Rs. 5,00,000 |

Rs. 30,000 (10%) |

|

Rs. 5,00,000 to Rs. 10,00,000 |

Rs. 1, 00,000 (20%) |

|

Above Rs. 10,00,000 |

Rs. 30,000 (30%) |

|

Total |

Rs. 1,60,000 |

Surcharge: surcharge of 10% of the Income Tax, where total taxable income is more than Rs. 1 crore. (Marginal Relief in Surcharge, if applicable)

Education Cess: it is 3% of the total Income Tax and Surcharge.

II. Individual resident who is of the age of 60 years or more but below the age of 80 years at any time during the previous year (i.e. born on or after 1st April 1934 but before 1st April 1954).

|

Income Slabs |

Tax Rates |

|

| 1 | Where the total income does not go beyond Rs. 2, 50,000/-. | NIL |

| 2 | Where the total income go beyond Rs. 2,50,000/- but does not exceed Rs. 5,00,000/- | 10% of the amount by which the total income surpasses Rs. 2, 50,000/-. |

| 3 | Where the total income go beyond Rs. 5,00,000/- but does not exceed Rs. 10,00,000/- | Rs. 25,000/- + 20% of the amount by which the total income surpasses Rs. 5, 00,000/-. |

| 4 | Where the total income exceeds Rs. 10,00,000/- | Rs. 125,000/- + 30% of the amount by which the total income surpasses Rs. 10, 00,000/-. |

Surcharge: surcharge of 10% of the Income Tax, where total taxable income is more than Rs. 1 crore. (Marginal Relief in Surcharge, if applicable)

Education Cess: it is 3% of the total Income Tax and Surcharge.

III. Individual resident who is of the age of 80 years or more at any time during the previous year (i.e. born before 1st April 1934).

|

Income Slabs |

Tax Rates |

|

| Where the total income does not surpass Rs. 5,00,000/-. | NIL | |

| 2 | Where the total income surpasses Rs. 5,00,000/- but does not exceed Rs. 10,00,000/- | 20% of the amount by which the total income goes beyond Rs. 5,00,000/-. |

| 3 | Where the total income surpasses Rs. 10,00,000/- | Rs. 100,000/- + 30% of the amount by which the total income goes beyond Rs. 10,00,000/-. |

Surcharge: surcharge of 10% of the Income Tax, where total taxable income is more than Rs. 1 crore. (Marginal Relief in Surcharge, if applicable)

Education Cess is 3% of the total Income Tax and Surcharge.

IV. Co-operative Society

|

Income Slabs |

Tax Rates |

|

| 1 | Where the total income does not surpass Rs. 10,000/-. | 10% of the income. |

| 2 | Where the total income surpasses Rs. 10,000/- but does not exceed Rs. 20,000/-. | Rs. 1,000/- + 20% of income in surplus Rs. 10,000/-. |

| 3 | Where the total income surpasses Rs. 20,000/- | Rs. 3.000/- + 30% of the amount by which the total income surpasses Rs. 20,000/-. |

Surcharge: surcharge of 10% of the Income Tax, where total taxable income is more than Rs. 1 crore.

Education Cess: it is 3% of the total Income Tax and Surcharge.

V. Firm

Income Tax: for firms, it is 30% of total income.

Surcharge: the surcharge is 10% of the Income Tax where total taxable income is more than Rs. 1 crore.

Education Cess: it is 3% of the total Income Tax and Surcharge in the firm’s case.

VI. Local Authority

Income Tax: For Local Authority, it is 30% of total income.

Surcharge: the surcharge is 10% of the Income Tax where total taxable income is more than Rs. 1 crore.

Education Cess: it is 3% of the total Income Tax and Surcharge.

VII. Domestic Company

Income Tax: For Domestic companies, 30% of total income.

Surcharge: The amount of income tax as calculated in agreement with the above rates, and after being reduced by the amount of tax rebate, shall be increased by an additional charge.

• At the rate of 5% of such income tax, on condition that the total income goes beyond Rs. 1 crore.

• At the rate of 10% of such income tax, on condition that the total income goes beyond Rs. 10 crores.

Education Cess: it is 3% of the total Income Tax and Surcharge.

VIII. Company other than a Domestic Company

Income Tax:

• At 50% of so much of the total income as comprise of (a) royalties received from Government or an Indian concern in fulfillment of an agreement made by it with the Government or the Indian concern after the 31st day of March 1961 but before the 1st day of April 1976; or (b) fees for technical adaptation services received from Government or an Indian concern in fulfillment of an agreement made by it with the Government or the Indian concern after the 29th day of February 1964 but before the 1st day of April 1976, and where such agreement has, in either case, been accepted by the Central Government.

• At 40% of the balance.

Surcharge:

The amount of income tax as calculated in agreement with the above rates, and after being abridged by the amount of tax rebate shall be increased by a surcharge as under:

• At the rate of 2% of such income tax, on condition that the total income goes beyond Rs. 1 crore.

• At the rate of 5% of such income tax, on condition that the total income exceeds Rs. 10 crores.

Education Cess: it is 3% of the total Income Tax and Surcharge.

Marginal Relief: When an assessee’s taxable income surpasses Rs. 1 crore, he is accountable for paying Surcharge at the agreed rates mentioned above on his income tax. However, the Income Tax and Surcharge amount shall not raise the income tax payable on a taxable income of Rs. 1 crore by further than the increase in taxable income.

Narendra Modi-led BJP government may offer sops to taxpayers

Imagine if the basic tax exemption is elevated up to Rs 3 lakh (additional Rs 50,000 exemption for women and senior citizens), interest on bank deposits is tax-free, and there is no tax on pension if you are over 60. The BJP had promised all this and more in its 2009 proposal.

This time the party reduced its promises, expressing them in imprecise statements without mentioning exact measures. Its 2019 policy said that the UPA government has “unleashed tax terrorism” and promised that the BJP would “provide a non-adversarial and favorable tax environment, and justify and make simpler the tax rule”.

Experts believe that the tax outgo of lower and middle-income earners may be reduced this year. Given the current economic state of affairs, there is little scope for the government to cut taxes. But the public is spinning under the high inflation, and some respite might be on the cards for lower and middle-income groups.

Taxpayers can expect the spreading of tax slabs, justification of certain exemption limits, and levitating the deduction limit under Section 80C. The additional Rs 1 lakh investment can be specifically reserved for infrastructure bonds and retirement products.

The big challenge before the Narendra Modi government would be to get hitched to these expectations with the reality of the loss in tax collections. Though direct tax collections outdid the revised target of Rs 6,41,835 crores during tax slabs of 2018-19, they were still about Rs 23,000 crore below the original target. If the government wants to amend taxes or improve deductions this year, it must balance the inevitable tax by increasing collections and ensuring stricter compliance.

For taxpayers, this means a greater examination of their income. The CBDT has already warned by putting salary slips under the scanner. In October 2018, salaried taxpayers who sought tax exemption for HRA of more than Rs 8,333 a month were asked to mention the PAN of their landlord. The new tax slabs forms were notified last month to seek a breakup of the exempted income received and capital gains earned by an individual.

Generously, most tax experts don’t think the government will broaden the service tax net or increase the rate. There is no scope for further growing the tax burden on services as they are already besieged with a high tax burden and the impact of the economic slowdown. Others point out that broadening the service tax or increasing its rate will have a tumbling effect on inflation. Any rise in indirect taxes will hit the rich and poor with equal force.

The tax experts and the industry are hopeful that the BJP will keep its statement promise of providing non-adversarial tax management. With more than Rs 4 lakh crore sealed in income tax disputes alone, the increasing number of disputes is a serious concern to the industry and the government. The industry faiths the new government would adopt non-adversarial policies.

Tax professionals are also expected that some out-of-date and unfair tax laws will be thrown out. Self-employed professionals should also be able to title HRA exemptions like salaried taxpayers. Right now, the exemption is stopped at Rs 2,000 per month. Tax laws should not be changed often because it creates confusion without adding any noteworthy benefit.

The Direct Taxes Code introduced in 2013 and revised in 2014 could not see the light of day because the UPA constituents had differing views on the offers. The huge majority with which the NDA has come to supremacy and that BJP alone has crossed the 272-mark specifies that the new government will not face such problems.

The concerns of Prime Minister Narendra Modi would be very diverse now. So, the Goods and Services Tax, which he had opposed as chief minister of Gujarat, might soon come into force.

Learn the juice of this article in just a single minute, Tax Slabs Infographics.

Recommended Articles

Here are some articles that will help you to get more detail about the Latest Tax Slabs & Rates, so just go through the link.

{kind=link}