What is Record-to-Report?

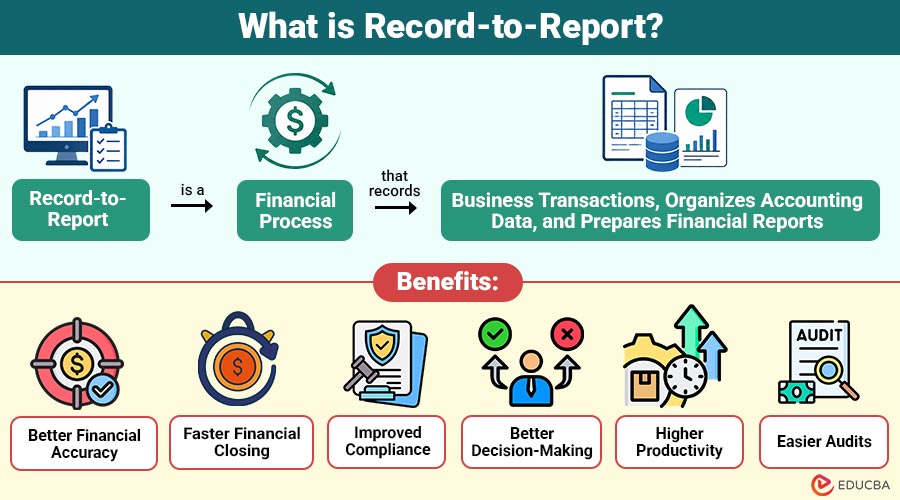

Record-to-Report (R2R) is a financial process that records business transactions, organizes accounting data, and prepares financial reports. It supports companies in keeping correct financial records, adhering to accounting rules, and making wise business decisions.

Daily financial transactions are recorded at the start of the record-to-report process, which concludes with the preparation of financial statements, including the balance sheet, income statement, and cash flow statement. It is an important part of the finance and accounting function because it ensures that financial information is complete, accurate, and available on time.

Table of Contents:

Key Takeaways:

- Record-to-Report improves financial accuracy through organized transactions, reconciliations, and reliable financial reporting processes effectively.

- R2R enables better decision-making by providing timely insights from accurate, structured financial data.

- Automation in R2R reduces errors, accelerates closing, and enhances overall accounting efficiency for businesses.

- Effective Record-to-Report ensures compliance, transparency, and improved control over organizational financial activities and performance.

Why is Record-to-Report Important?

Below are the key reasons why Record-to-Report is important for improving financial management, accuracy, compliance, and business performance.

1. Improves Financial Accuracy

Ensures reliable financial records by reducing discrepancies, improving data quality, and maintaining accurate reporting processes.

2. Supports Better Business Decisions

Provides timely financial insights that help leaders make informed strategic and operational decisions.

3. Ensures Compliance with Accounting Standard

Maintains adherence to financial regulations, reporting requirements, and established accounting principles.

4. Reduces Accounting Errors

Minimizes manual mistakes through standardized processes, automation, validation checks, and improved data management.

5. Speeds up Month-end and Year-end Closing

Accelerates closing activities by streamlining reconciliations, reporting, and financial consolidation.

6. Increases Transparency Across the Organization

Provides clear visibility into financial information, performance metrics, and organizational financial activities.

7. Makes Audits Easier

Simplifies audit procedures by maintaining organized records, accurate documentation, and complete financial transaction histories.

Record-to-Report Process

The record-to-report process consists of several simple steps.

1. Record Financial Transactions

The first step is recording all business transactions, such as sales, purchases, expenses, payroll, and payments, in the accounting system.

2. Post Journal Entries

After transactions are recorded, journal entries are created to classify them correctly in different accounts.

3. Update the General Ledger

All journal entries are posted to the General Ledger, which stores the company’s financial information in one place.

4. Reconcile Accounts

Finance teams compare accounting records with bank statements, invoices, and other documents to ensure everything matches correctly.

5. Close the Accounting Period

At the end of each month, quarter, or year, businesses review all transactions, make adjustments if needed, and close the accounting books.

6. Prepare Financial Reports

Finally, financial statements and management reports are generated. These reports help management, investors, auditors, and regulators understand the company’s financial performance.

Main Components of Record-to-Report

Below are the key components of the Record-to-Report process that help organizations manage financial data, maintain accuracy, and prepare reliable financial reports.

1. Financial Transaction Recording

Captures and organizes all financial transactions to maintain accurate and complete accounting records.

2. Journal Entries

Records financial activities by systematically documenting debits, credits, adjustments, and transaction details.

3. General Ledger

Maintains a centralized record of all accounts, balances, and financial transactions for reporting purposes.

4. Account Reconciliation

Compares financial records with supporting documents to accurately identify and resolve discrepancies.

5. Financial Close

Completes accounting activities to finalize financial records during monthly, quarterly, and yearly periods.

6. Financial Reporting

Produces financial reports and statements that provide light on the health and performance of the company’s finances.

7. Compliance and Audit Support

Ensures proper documentation, regulatory adherence, and smooth audit processes through organized financial records.

Benefits of Record-to-Report

A well-managed record-to-report process offers many benefits.

1. Better Financial Accuracy

Standardized processes reduce errors and enhance the reliability and quality of financial information.

2. Faster Financial Closing

Automation streamlines closing activities, enabling finance teams to complete month-end and year-end tasks quickly.

3. Improved Compliance

Helps businesses follow accounting standards, regulations, and reporting requirements with greater ease.

4. Better Decision-Making

Provides accurate financial insights that support effective planning, strategy, and business growth decisions.

5. Higher Productivity

Automation minimizes repetitive tasks, allowing finance teams to focus on valuable analytical activities.

6. Easier Audits

Organized financial records simplify audit procedures, improve transparency, and reduce audit preparation efforts.

Common Challenges in Record-to-Report

Organizations may face several challenges while managing the record-to-report process.

1. Manual Processes

Manual data entry consumes time, increases workload, and increases the likelihood of financial reporting errors.

2. Multiple Systems

Different accounting systems can create data inconsistencies, integration issues, and difficulties in financial reporting.

3. Slow Financial Close

Delayed approvals and missing information can extend closing cycles and impact reporting timelines.

4. Data Errors

Incorrect or incomplete financial information can reduce reporting accuracy and affect business decisions.

5. Compliance Requirements

Businesses must continuously adapt to changing accounting standards, tax rules, and regulatory requirements.

Technologies Used in Record-to-Report

Modern technology makes the record-to-report process faster and more efficient. Some commonly used technologies include:

1. Enterprise Resource Planning

Integrates financial data and processes to improve accuracy, visibility, and operational efficiency.

2. Robotic Process Automation

Automates repetitive accounting tasks, reduces manual effort, and improves processing speed.

3. Artificial Intelligence

Analyzes financial data, detects patterns, and supports smarter accounting decisions.

4. Cloud Accounting Software

Provides secure access to financial information with flexible, scalable, and efficient management.

5. Business Intelligence Tools

Converts financial data into insights through reports, dashboards, and performance analysis.

Example of Record-to-Report

A practical example below shows how Record-to-Report helps businesses automate financial processes, improve reporting accuracy, and achieve faster financial closing.

A retail company records thousands of sales and purchase transactions every month. Previously, the finance team entered data manually, delaying financial reporting.

After implementing an ERP system with automated reconciliation and reporting, the company reduced manual work, completed month-end closing faster, improved reporting accuracy, and gained better visibility into its financial performance.

Final Thoughts

Record-to-Report (R2R) helps organizations manage financial transactions, maintain accurate records, and generate reliable reports. It improves compliance, decision-making, and financial control. Through automation, standardized workflows, and advanced accounting technologies, businesses can reduce errors, accelerate financial closing, enhance reporting efficiency, and achieve better overall financial performance.

Frequently Asked Questions (FAQs)

Q1. Who is responsible for managing the Record-to-Report process?

Answer: The R2R process is usually managed by finance professionals, accountants, controllers, and financial reporting teams within an organization.

Q2. How does automation improve the record-to-report process?

Answer: Automation reduces manual work, speeds up transaction processing, improves data accuracy, and helps finance teams complete reporting activities more efficiently.

Q3. Which financial reports are generated through Record-to-Report?

Answer: R2R generates key reports, including balance sheets, profit and loss statements, cash flow statements, financial summaries, and management reports.

Q4. Can small businesses use Record-to-Report processes?

Answer: Yes, small businesses can use simplified R2R practices with accounting software to organize financial data and improve reporting accuracy.

Recommended Articles

We hope that this EDUCBA information on “Record-to-Report” was beneficial to you. You can view EDUCBA’s recommended articles for more information.