Updated July 25, 2023

Definition of EBITDA

EBITDA stands for Earnings before Interest, Tax, Depreciation, and Amortization. When preparing a company’s financial statements, analysts and stakeholders frequently discuss the EBITDA margin and the number of EBITDA as the most prominent line item in the income statement for judging the business’s profitability.

It refers to the earnings for any business that comes solely from its operations, and it comes after gross profit and deduction of various overheads, selling, and distribution expenses.

Types and Components of EBITDA

To calculate the (Earnings before Interest, Tax, Depreciation, and Amortization) of the company, we need to follow the following steps.

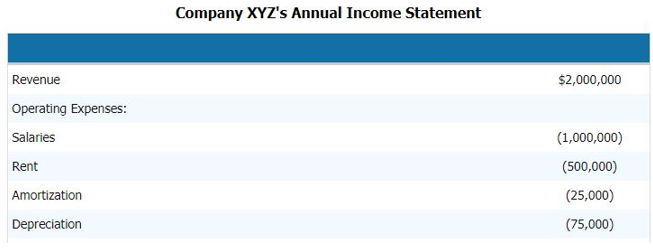

The company’s income statement below offers a clear picture of the components comprising EBITDA, allowing us to understand its composition.

To compute the EBITDA of the above company, we need to deduct all the operating and non-operating expenses of the company from the revenue.

Hence,

Revenue – Operating Expenses – Salaries – Rent – Amortization – Depreciation

By deducting this, we can arrive at the EBITDA component.

- EBITDA = $2,000,000 – $1,000,000 – $500,000 – $25,000 – $75,000

- = $400,000

Hence the component of the EBITDA is revenue, operating expense, salaries, rent, depreciation and amortization, and other direct and indirect expenses.

EBITDA Formula

Alternatively, we can calculate (Earnings before Interest, Tax, Depreciation, and Amortization) backward by adding the interest and the non–cash expense component to EBT, i.e. earnings before tax, or PBT, i.e. profit before tax.

So the formula will be:

Examples of EBITDA

Let’s take an example to understand the calculation of (Earnings before Interest, Tax, Depreciation, and Amortization) in a better manner.

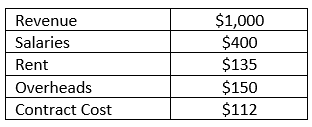

Company RMZ Corp prepares their income statements per the U.S. GAAP, and the Income statement for 2003 – 2004 is given below. First, calculate the (Earnings before Interest, Tax, Depreciation, and Amortization) and the EBITDA margin of the company for the fiscal year.

Solution:

In this case, you can calculate Earnings before Interest, Tax, Depreciation, and Amortization by deducting all the direct and indirect expenses the business has incurred from the revenue it generated during that fiscal year.

EBITDA calculation:

- = 1000 – 400 – 135 – 150 – 112

- = 203

EBITDA Margin is calculated as:

EBITDA Margin = EBITDA/Revenue

- = 203 / 1000

- = 20.3%

Advantages and Disadvantages of EBITDA

Advantages

- It is the business’s most important line item, which is why it is widely used for financial analysis and peer group analysis.

- It is the only line item that tells the analyst the strength of the business and whether the business can recover all the expenses it is incurring to generate revenue. Internal management uses it for reporting, discussing, and analyzing.

- It also tells the management and the executive of the business how well it is generating the revenue to recover the cost incurred if any business’s (Earnings before Interest, Tax, Depreciation, and Amortization) are negative. It becomes an alarming situation for the business to operate.

Disadvantages

- It is widely used in valuation techniques, especially when using the discounted cash flow method. It can also give misleading results at times because each company can report its Earnings before Interest, Tax, Depreciation, and Amortization differently and have a separate definition of Earnings before Interest, Tax, Depreciation, and Amortization.

- Earnings before Interest, Tax, Depreciation, and Amortization is also misleading sometimes when annual financial reports use different accounting principles to calculate the Earnings before Interest, Tax, Depreciation, and Amortization or to compute the cost components of their business, in that case, the Earnings before Interest, Tax, Depreciation, and Amortization of the companies under comparison doesn’t become alike hence EBIT is now widely been used these days.

Limitations

- Earnings before Interest, Tax, Depreciation, and Amortization have a limitation: it does not account for changes in working capital. Liquidity fluctuates because of interest, taxes, and capital expenditures.

- Determine how difficult it would be to turn assets into cash. This could highlight low liquidity, but we have different liquidity measures and ratios.

Conclusion

Hence, the business should not judge the company’s financial strength and weakness by just looking at the Earnings before Interest, Tax, Depreciation, and Amortization margin or the number. Instead, a detailed analysis of the company’s profit line items should be done to complete and good analysis.

Recommended Articles

This is a guide to EBITDA Example. Here we discuss types & components, examples, advantages and disadvantages. You may also look at the following articles to learn more –