What is Convexity?

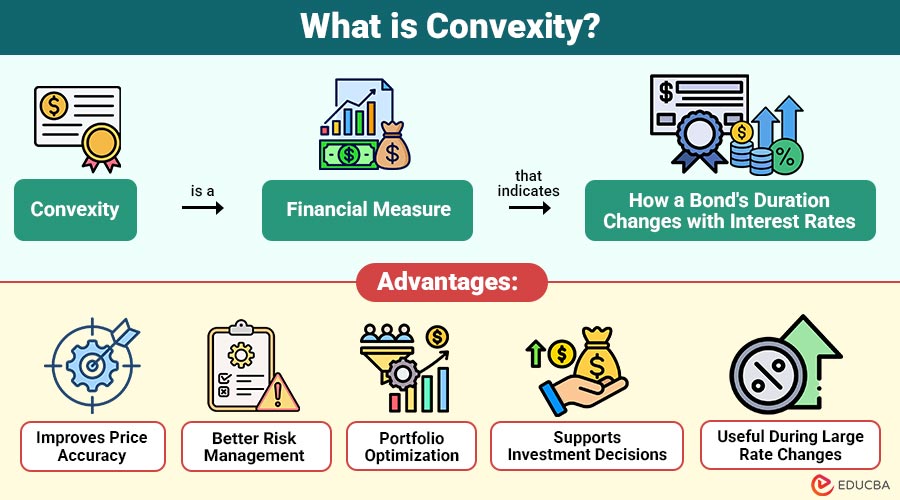

Convexity is a financial measure that indicates how a bond’s duration changes with interest rates. It provides a more accurate estimate of bond price movements than duration alone by accounting for the curved relationship between bond prices and yields, especially during large interest rate changes.

For example, if two bonds have the same duration but different convexity, the bond with higher convexity will typically gain more when interest rates fall and lose less when rates rise.

Table of Contents:

Key Takeaways:

- Convexity improves bond price estimates by adjusting duration to account for changes in interest rate sensitivity during market fluctuations.

- Higher positive convexity generally benefits investors through larger gains and smaller losses as interest rates change.

- Bond maturity, coupon rate, yields, and embedded options significantly influence overall convexity and price behavior.

- Investors use convexity alongside duration to manage interest rate risk and optimize fixed-income investment portfolios.

Why is Convexity Important?

Below are the key reasons why it is important:

1. Estimate Bond Price Changes

Helps estimate bond price movements more accurately, especially when interest rates change significantly in either direction.

2. Compare Similar Bonds

It enables investors to compare bonds with similar durations by evaluating differences in their interest rate sensitivity.

3. Measure Interest Rate Risk

Provides a more precise measure of interest rate risk than duration, improving the accuracy of investment decision-making.

4. Improve Portfolio Management

Portfolio managers use convexity to optimize bond allocations and manage interest rate exposure more effectively over time.

5. Reduce Forecasting Errors

Minimizes pricing errors by accounting for the curvature of relationship between bond prices and changing interest rates.

How does Convexity Work?

It helps investors understand the nonlinear relationship between bond prices and interest rates.

Here’s how it works:

- Interest rates change.

- Bond prices move in the opposite direction.

- Duration estimates the initial price change.

- Convexity adjusts the estimate for greater accuracy.

- Investors combine duration and convexity to estimate actual price movements.

The estimated percentage price change is:

This formula is widely used by portfolio managers and fixed-income analysts.

Types of Convexity

It is generally classified into three types based on how a bond’s price responds to changes in interest rates.

1. Positive Convexity

Occurs when bond prices rise more as interest rates fall than they decline when interest rates rise.

2. Negative Convexity

Occurs when bond prices rise less as interest rates fall because the issuer or borrower has option to repay the debt early.

3. Zero Convexity

Although uncommon, some financial instruments exhibit nearly zero convexity over a limited range of interest-rate changes, meaning their price changes are almost linear.

Factors Affecting Convexity

Several factors influence a bond’s convexity.

1. Maturity

Longer-maturity bonds generally have higher convexity because their prices respond more significantly to changing interest rates over time.

2. Coupon Rate

Lower-coupon bonds usually exhibit higher convexity because a larger portion of their value comes from future cash flows.

3. Yield Level

Lower bond yields generally increase convexity, making bond prices more sensitive to changes in market interest rates.

4. Embedded Options

Callable and puttable bonds have altered convexity because embedded options affect expected cash flows and price behavior.

5. Cash Flow Timing

Bonds with cash flows further in the future generally exhibit greater convexity and higher interest-rate sensitivity.

Advantages of Convexity

It offers several advantages for investors and portfolio managers.

1. Improves Price Accuracy

It estimates bond price changes more accurately than duration alone, especially during larger interest rate movements.

2. Better Risk Management

It helps investors better understand interest rate risk and manage fixed-income investment risk more effectively.

3. Portfolio Optimization

Portfolio managers use convexity to select bonds that better match investment objectives and desired risk-return profiles.

4. Supports Investment Decisions

It enables investors to compare bonds with similar durations but different sensitivities to interest rate changes.

5. Useful During Large Rate Changes

It becomes especially valuable when interest rates change significantly, improving bond price predictions and investment decisions.

Limitations of Convexity

Despite its usefulness, it has certain limitations.

1. More Complex

Calculating convexity requires additional data, formulas, and mathematical analysis, making it more complex than duration calculations.

2. Less Useful for Small Rate Changes

For minor interest rate changes, duration often provides sufficiently accurate estimates of bond prices without requiring convexity analysis.

3. Option-Embedded Bond

Callable and mortgage-backed securities exhibit changing convexity, making their price behavior more difficult to predict accurately.

4. Market Assumptions

Calculations assume smooth interest rate movements, which may not consistently reflect actual market volatility.

5. Requires Continuous Monitoring

It changes over time as bond yields, prices, and remaining maturities evolve with changing market conditions.

Applications of Convexity

It is widely used across the financial industry.

Real-World Examples

The following examples illustrate how convexity influences bond pricing and interest rate risk in real-world fixed-income investments.

1. Callable Corporate Bond

A corporation issues callable bonds that allow early redemption if interest rates fall. Although investors initially expect substantial price appreciation as interest rates decline, the callable feature limits gains because the issuer may refinance the debt. This results in negative convexity.

2. Pension Fund Management

A pension fund holds long-term bonds to match future retirement obligations. Portfolio managers evaluate both duration and convexity to reduce interest rate risk while maintaining stable funding levels over time.

Final Thoughts

Convexity is an essential concept in fixed-income investing because it provides a more precise measure of how bond prices respond to changing interest rates. While duration offers a useful first estimate of price sensitivity, convexity captures the curvature of the price-yield relationship, making forecasts more accurate during significant rate movements. By understanding convexity alongside duration, investors, portfolio managers, banks, and pension funds can better manage interest rate risk, optimize bond portfolios, and make more informed investment decisions.

Frequently Asked Questions (FAQs)

Q1. Which bonds have high convexity?

Answer: Long-term, low-coupon bonds without embedded options typically have higher convexity.

Q2. Can convexity be negative?

Answer: Yes. Callable bonds and mortgage-backed securities often exhibit negative convexity.

Q3. Does convexity replace duration?

Answer: No. It complements duration by providing a more precise price estimate.

Q4. Does convexity change over time?

Answer: Yes. It changes as interest rates, bond prices, and time to maturity change.

Recommended Articles

We hope that this EDUCBA information on “Convexity” was beneficial to you. You can view EDUCBA’s recommended articles for more information.