What is Double Gearing?

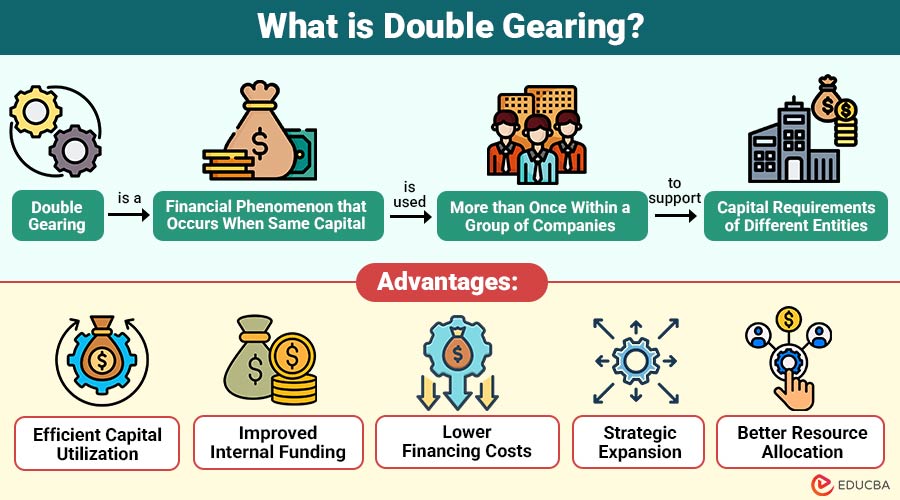

Double gearing is a financial phenomenon that occurs when the same capital is used more than once within a group of companies to support the capital requirements of different entities. It commonly arises in corporate groups, financial institutions, insurance companies, and banking conglomerates where one company invests in the capital of another group company, creating an overlap in capital recognition.

For example, a parent company injects capital into a subsidiary, which then uses that capital to meet its own regulatory or operational capital requirements. As a result, the same funds appear as capital in multiple entities, potentially overstating the group’s overall financial strength.

Table of Contents:

- Meaning

- Importance

- Working

- Key Features

- Types

- Advantages

- Disadvantages

- Real-World Examples

- Difference

Key Takeaways:

- Double gearing duplicates capital across entities, potentially significantly overstating a group’s financial strength.

- Regulators adjust for double gearing to ensure accurate capital adequacy assessments.

- Common in banking, insurance, and financial conglomerates with interconnected capital structures.

- Understanding double gearing helps evaluate solvency, risks, and overall financial stability.

Importance of Understanding Double Gearing

For investors, regulators, and financial analysts, understanding double gearing is essential because it helps:

1. Evaluate the True Strength of a Corporate Group

Helps determine actual financial strength by eliminating the effects of duplicated capital within groups.

2. Assess Capital Adequacy Accurately

Enables accurate measurement of available capital resources supporting regulatory and operational requirements.

3. Identify Hidden Financial Risks

Reveals potential vulnerabilities arising from interconnected capital structures and financial dependencies.

4. Improve Investment Decisions

Provides clearer insights into financial stability, helping investors make informed investment choices.

5. Understand Regulatory Disclosures

Helps interpret regulatory reports and capital disclosures more effectively and accurately.

6. Analyze Group Solvency More Effectively

Supports better evaluation of a group’s ability to absorb losses and remain solvent.

How Does Double Gearing Work?

The process generally follows these steps:

- A parent company raises capital from shareholders or external investors.

- The parent invests part of this capital in a subsidiary.

- The subsidiary records the investment as its capital.

- Both the parent and subsidiary include the same funds in their capital calculations.

- The capital effectively supports two balance sheets simultaneously.

Example:

Suppose Company A raises $100 million from investors.

- Company A invests the entire $100 million in Subsidiary B.

- Company A records the investment as an asset.

- Subsidiary B records the $100 million as equity capital.

If both companies count this amount toward their capital positions, the group appears to have $200 million in capital, even though only $100 million of external capital actually exists.

This duplication is known as double gearing.

Key Features of Double Gearing

The following features highlight how double gearing operates within corporate groups and why regulators and financial analysts closely monitor it:

1. Capital Duplication

The same capital is recognized by multiple entities, resulting in overlapping capital representations within a corporate group.

2. Common in Financial Groups

Double gearing frequently occurs in banking, insurance, and financial conglomerates operating through regulated subsidiaries.

3. Regulatory Concern

Regulators monitor and adjust double gearing to prevent overstated capital positions and financial stability risks.

4. Internal Capital Movement

Capital is transferred among related group entities rather than raised from external investors.

5. Impact on Capital Adequacy

It can inflate capital adequacy ratios, making institutions appear financially stronger than reality.

6. Group-Level Analysis

It becomes evident during consolidated financial analysis, where intra-group capital relationships are thoroughly examined.

Types of Double Gearing

Double gearing can occur in several forms depending on how capital is transferred and recognized within a corporate group. The most common types include:

1. Direct Double Gearing

A parent company invests capital into a subsidiary, allowing both entities to recognize the same capital simultaneously.

2. Indirect Double Gearing

Capital duplication occurs through multiple ownership layers, where subsidiaries reinvest funds into other group companies.

3. Cross-Holding Double Gearing

Group entities hold each other’s capital instruments, resulting in the same capital base being counted multiple times.

4. Regulatory Double Gearing

The same capital instrument qualifies as regulatory capital for multiple regulated entities within a corporate group.

Advantages of Double Gearing

Although regulators often view it cautiously, double gearing may offer certain advantages to corporate groups.

1. Efficient Capital Utilization

Corporate groups can leverage existing capital across multiple subsidiaries, maximizing resource usage without frequently raising additional funds.

2. Improved Internal Funding

Subsidiaries receive financial support from the parent company, reducing dependence on external lenders and capital markets.

3. Lower Financing Costs

Internal capital allocation decreases borrowing needs, helping organizations reduce interest expenses and overall financing costs.

4. Strategic Expansion

Groups can efficiently finance acquisitions, market expansion, and growth initiatives by using available internal capital.

5. Better Resource Allocation

Management can allocate capital strategically to high-performing subsidiaries, supporting growth opportunities and improving returns.

Disadvantages of Double Gearing

Despite its advantages, double gearing can create significant financial and regulatory concerns.

1. Overstatement of Financial Strength

The same capital may be counted multiple times, creating an inflated impression of financial stability and solvency.

2. Increased Financial Risk

Losses in one group entity can affect others because capital resources are interconnected across the organization.

3. Regulatory Restrictions

Regulators often require capital adjustments, reducing reported capital levels and limiting potential financial flexibility.

4. Reduced Transparency

Complex ownership structures can obscure capital duplication, making financial positions harder for investors to evaluate.

5. Potential Capital Shortfalls

During financial stress, actual loss-absorbing capacity may be lower than reported capital figures initially suggest.

6. Investor Concerns

Excessive double gearing may raise concerns about aggressive capital practices and the group’s financial resilience.

Real-World Examples

The following examples illustrate how double gearing can arise in different types of financial groups and why regulatory adjustments are often necessary:

1. Banking Group

A bank holding company raises ₹1,000 crore through equity issuance and injects the funds into its banking subsidiary.

- A holding company records an investment asset.

- Banking subsidiary records equity capital.

- Both entities appear well-capitalized.

Regulators may deduct the investment from group capital calculations to avoid double counting.

2. Insurance Conglomerate

An insurance parent company invests capital into a life insurance subsidiary. The subsidiary uses the funds to meet solvency requirements, while the parent continues to recognize the investment as an asset. This creates a double-gearing situation that regulators typically adjust during group supervision.

3. Financial Conglomerate

A diversified financial services group owns a bank, an insurance company, and an investment firm. Capital moves between entities to support regulatory requirements.

Difference Between Double Gearing and Multiple Gearing

The table below highlights the key differences:

| Basis | Double Gearing | Multiple Gearing |

| Definition | The same capital is counted twice within a group | The same capital is counted multiple times across several entities |

| Complexity | Relatively simple structure | More complex ownership chains |

| Number of Entities | Usually two entities | Three or more entities |

| Capital Duplication | Occurs twice | Occurs several times |

| Regulatory Impact | Significant | More severe |

| Risk Level | Moderate to high | Higher due to extensive capital overlap |

| Common Usage | Parent-subsidiary structures | Large financial conglomerates |

| Monitoring Difficulty | Easier | More challenging |

Final Thoughts

Double gearing occurs when the same capital is counted by multiple entities within a corporate group. Although it can enhance capital efficiency and support growth initiatives, it may overstate financial strength and increase risk. Understanding double gearing helps investors, regulators, and analysts accurately assess solvency, capital adequacy, and overall financial stability.

Frequently Asked Questions (FAQs)

Q1. Why is double gearing considered risky?

Answer: It can overstate financial strength and reduce the accuracy of capital adequacy assessments.

Q2. Where is double gearing commonly found?

Answer: It is most common in banking groups, insurance companies, and financial conglomerates.

Q3. How do regulators deal with double gearing?

Answer: Regulators typically deduct intra-group investments or use consolidated supervision methods to prevent double counting.

Q4. Is double gearing illegal?

Answer: No. However, regulators closely monitor and adjust for it to ensure accurate reporting of capital positions.

Recommended Articles

We hope that this EDUCBA information on “Double Gearing” was beneficial to you. You can view EDUCBA’s recommended articles for more information.