What Are the Best Ways to Save for College?

If you are a parent, you have felt the pressure around college savings. Tuition rises every year. And so does the cost of housing and textbooks. With all of these mounting costs in the background, it is easy to feel like you are way behind on college savings. But is that true? You probably know all about 529 college savings plans and might even have one for your children but in light of the current economy and rising costs, it is worth mentioning that these are not the only option.

Saving for a child’s education does not have to be “529 or bust,” and your strategy depends on your priorities, financial situation, and the level of flexibility you want in the future. Ultimately, college savings works best when it fits into your broader financial life. That is why exploring different options can be especially valuable.

Why 529 Plans Are So Popular?

Before exploring alternatives, it helps to understand what makes 529s a popular choice. The biggest draw is the tax advantage. You contribute after-tax money, and it grows tax-free. As long as you use the funds for qualified education expenses things like tuition, room and board, books, and even certain K–12 costs you do not pay taxes on the growth. In some states, you also get a tax deduction or credit on your contributions. Beyond tax benefits, 529 plans are easy to set up, simple to automate, and wide-reaching in what they can cover. You can use 529 funds for:

- Trade schools

- Community colleges

- Registered apprenticeship programs

- Certain international schools

Another benefit of 529 plans is that if one child does not need the money, you can transfer the account to a sibling, a cousin, or even yourself if you decide to continue your education. This level of flexibility makes 529 plans a pretty solid foundation for most families. But they still have limitations, which is where alternative strategies come into play.

When a 529 Plan Might Not Be the Perfect Fit?

You may want more flexibility than a 529 can offer. For example, you might worry that your child will not attend college. Or you might want access to the money for something else if life takes an unexpected turn. While 529 plans have become more flexible over the years, using funds for non-education expenses can result in tax and penalty consequences.

Some families also want the chance to invest differently than what a 529 plan offers. Others need a simpler solution if they are saving late in the game or juggling other financial priorities. Whatever the reason, it helps to know that several other options exist.

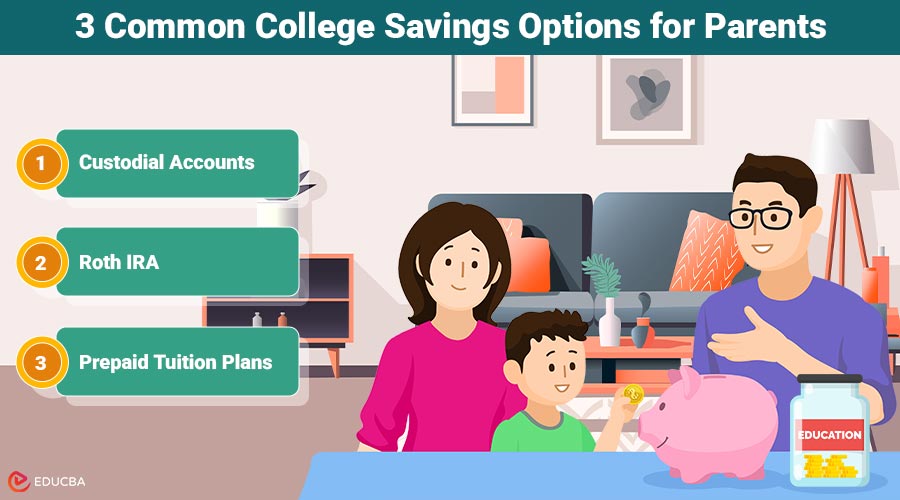

3 Common College Savings Options for Parents

Here are some of the most common alternatives, each offering different strengths depending on your goals:

1. Custodial Accounts (UGMA/UTMA)

A custodial account lets you invest for your child without the limitations of a 529 plan. You can use the funds for any expenses that benefit the child, not just education. That flexibility appeals to parents who want the option to support a first car, extracurricular expenses, or future travel. The downside is that custodial accounts lack the tax advantages of 529 plans, and the assets transfer to the child once they reach the age of majority. Once that happens, they have full control of the account. That is great if they are responsible, but less ideal if they are not.

2. Roth IRA

A Roth IRA is primarily a retirement tool, but it can also double as a supplemental college savings vehicle. You can withdraw contributions tax-free anytime, and you can use earnings for qualified education expenses without paying a penalty. This is useful if you want flexibility. If your child ends up receiving scholarships or choosing a more affordable path, the money remains in your Roth for retirement. The biggest limitation is the annual contribution cap, which may restrict how much you can save each year.

3. Prepaid Tuition Plans

Some states and universities allow you to “lock in” tuition at current rates. With college costs rising faster than inflation, this can offer peace of mind. However, prepaid plans are usually available only for specific schools or state systems. If your child decides not to attend those schools, options become limited.

Combining Strategies Can Strengthen Your College Savings Plan

Instead of choosing one option, many families take a blended approach. You might use a 529 plan for the bulk of your college savings because of its tax benefits, while adding a taxable account or a Roth IRA to maintain flexibility. Someone saving aggressively for multiple children might start with a 529 plan and supplement it with a custodial account for non-education needs.

This is where working with a financial planner becomes especially valuable. They can look at your entire financial landscape income, debt, retirement contributions, insurance, investments, cash flow and help you design a college savings strategy that fits within your long-term goals. A good advisor can help you determine how much you can comfortably save, which mix of accounts makes sense for your situation, and how to adapt your plan as your child grows.

Final Thoughts

A 529 plan remains one of the most tax-efficient college savings tools available, but it does not have to be your only option. Understanding custodial accounts, Roth IRAs, brokerage accounts, ESAs, and prepaid tuition plans enables families to design a well-rounded strategy tailored to their flexibility, risk tolerance, and financial goals. Saving for college is a long-term effort. With the right combination of tools and a thoughtful college savings plan that aligns with overall wealth-building and retirement goals, both parents and students are better positioned for future success.

Recommended Articles

We hope this guide to college savings helps you plan effectively for your child’s education. Check out these recommended articles for more tips and strategies to optimize your college journey.