What is an Annuity?

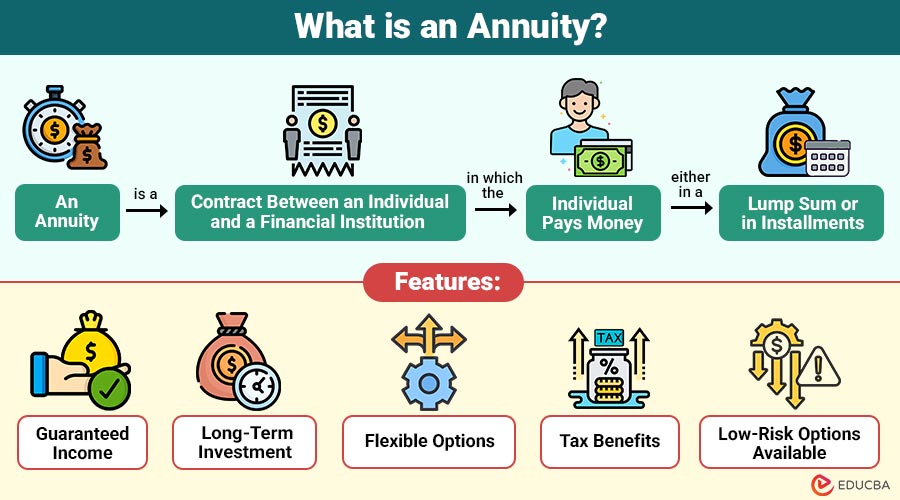

An annuity is a contract between an individual and a financial institution in which the individual pays money either in a lump sum or in installments. In return, the institution promises to provide regular income payments either for fixed period or for life.

Example: If a person invests ₹10 lakhs in an annuity plan, the insurance company may pay them ₹8,000 every month for 20 years or even for life, depending on the plan selected.

Table of Contents:

- Meaning

- Working

- Types

- Features

- Benefits

- Limitations

- Who Should Invest in Annuities?

- Real-World Example

- Difference

- How to Choose the Right Annuity Plan?

Key Takeaways:

- Annuities provide a steady income stream, making them an effective financial solution for retirement planning.

- They offer multiple plan options to match different income needs, goals, and risk preferences.

- Fixed annuities provide stability, while variable annuities offer growth potential but carry higher risk.

- Choosing the right annuity helps secure long-term financial stability and reduces retirement income uncertainty.

How Does an Annuity Work?

The work can be broken into two main phases:

1. Accumulation Phase

This is the stage at which the investor builds annuity value by contributing money over time or as a lump sum.

- Lump sum payment: One-time large investment at the start.

- Regular contributions: Small payments made monthly, quarterly, or yearly.

The insurance company invests the money and grows through interest or market returns. In many cases, growth is tax-deferred until withdrawal. The goal of this phase is to build a sufficient fund for future income needs, especially retirement.

2. Distribution Phase

This is the stage where the investor starts receiving regular income from the accumulated amount.

Payments can be received as:

- Monthly

- Quarterly

- Yearly

The payout depends on the total fund value, age, and contract terms. Some plans offer income for a fixed period, while others provide lifetime payments. This phase ensures a steady income stream for financial stability during retirement.

Types of Annuities

Annuities come in different forms depending on payout timing, investment type, and risk preference.

1. Immediate

An immediate annuity starts payments soon after investment, providing quick income, mainly useful for retirees needing immediate financial support.

2. Deferred

A deferred annuity defers payouts to a future date, allowing money to grow over time, and is ideal for long-term retirement planning.

3. Fixed

A fixed annuity offers guaranteed, stable returns with predictable payouts, protecting investors from market fluctuations and ensuring financial security.

4. Variable

A variable annuity links returns to market investments such as stocks or funds, offering higher growth potential but also increased financial risk.

5. Life

A life annuity ensures regular payments continue throughout the annuitant’s lifetime, providing long-term financial stability and protection against longevity risk.

6. Joint Life

A joint life annuity pays income until both individuals pass away, a common option for couples seeking shared lifelong financial security and support.

Features of Annuities

Here are the key features that makes it a reliable financial tool for long-term income and stability:

1. Guaranteed Income

Helps people manage routine expenses without financial uncertainty by offering a consistent and dependable income stream for a predetermined period of time or for life.

2. Long-Term Investment

They are mainly designed for long-term goals, such as retirement planning, to ensure financial stability during post-retirement years when active income stops.

3. Flexible Options

People can pick from a variety of annuities, including fixed, variable, immediate, and deferred, according on their income requirements, risk tolerance, and financial objectives.

4. Tax Benefits

In many cases, it offers tax-deferred growth, meaning earnings are not taxed until withdrawals begin, which can help in better wealth accumulation over time, depending on local tax laws.

5. Low-Risk Options Available

Some varieties, such as fixed annuities, offer little risk since they guarantee returns, which makes them appropriate for conservative investors who value security above large profits.

Benefits of Annuities

Here are the key benefits that makes it a valuable option for ensuring financial stability and retirement security:

1. Financial Security in Retirement

Provides a reliable retirement income, ensuring financial security and helping individuals maintain their desired lifestyle.

2. Protection Against Longevity Risk

Protects against longevity risk by ensuring income continues even if individuals live significantly longer than expected.

3. Stable and Predictable Income

Offers stable, predictable income streams over time, unlike the volatility of investments such as stocks or mutual funds.

4. Peace of Mind

Guaranteed regular income from annuities provides retirees with peace of mind and reduces financial stress during retirement years.

5. Customizable Plans

Plans are customizable, allowing individuals to adjust payouts to meet goals, needs, and risk preferences.

Limitations of Annuities

Here are the key limitations that individuals should consider before investing in annuities:

1. Lack of Liquidity

Once invested, annuity funds are locked, making withdrawal difficult and often incurring penalties for early access.

2. High Fees

Certain products, particularly variable ones, involve significant management, administrative, and additional hidden charges.

3. Complexity

Different structures and terms can be confusing, making it difficult for beginners to understand them fully.

4. Limited Growth Potential

Annuities generally offer lower returns than market-linked investments, limiting long-term wealth growth.

5. Irreversibility of Decision

Once an annuity is purchased, it is often difficult to change terms or exit the contract without financial loss or restrictions.

Who Should Invest in Annuities?

Here are the types of individuals for whom annuities can be a suitable financial choice:

1. Retirees

Provides a predictable monthly income, helping retirees manage expenses without worrying about market fluctuations or volatility risks.

2. Long-Term Planners

Helps build long-term financial stability by providing steady income growth and reducing future financial uncertainty.

3. Low-Risk Investors

Conservative investors who value safety, capital protection, and steady, predictable returns over time might consider annuities.

4. Guaranteed Return Seekers

Offers guaranteed income, making them ideal for individuals seeking to avoid market risk and the fluctuations in investment performance.

They may not be ideal for:

1. Young High-growth Investors

Young investors focused on high returns may find annuities unsuitable because of their limited growth potential over time.

2. People Needing Liquidity

Annuities are not liquid investments, so early withdrawals can result in penalties and reduced overall benefits value.

Real-World Example

Here is a simple example to understand how annuities work in real life:

Consider a 60-year-old individual retiring with savings of ₹50 lakhs. Instead of keeping the money in a savings account, they purchase a life annuity plan.

The insurance company agrees to pay ₹30,000 per month for the rest of their life. This ensures:

- Stable monthly income

- No worry about market fluctuations

- Financial independence during retirement

Difference Between Annuity and Fixed Deposit

Here is a clear comparison between both:

| Aspect | Annuity | Fixed Deposit |

| Purpose | Retirement income | Savings growth |

| Payout | Regular income | Lump sum at maturity |

| Duration | Long-term/lifetime | Fixed term |

| Liquidity | Low | Medium |

| Risk | Low to medium | Low |

How to Choose the Right Annuity Plan?

When selecting an annuity, consider the following:

1. Financial Goals

Understand your financial goals clearly, whether you need immediate retirement income or long-term future income, and plan accordingly.

2. Risk Tolerance

Choose fixed annuities for safety or variable annuities for higher returns, carefully considering your market risk and preference level.

3. Payout Options

Check whether you want monthly, quarterly, or yearly payouts depending on your income needs and financial planning goals.

4. Inflation Protection

Look for plans that offer increasing payouts over time to protect against inflation and maintain purchasing power effectively.

5. Insurance Provider Reputation

Always pick a reputable and trustworthy financial institution with a solid track record of returns, excellent customer service, and a solid reputation.

Final Thoughts

Annuities are financial tools that convert savings into a steady income, offering long-term security and peace of mind during retirement. Choosing the right plan depends on personal goals, risk tolerance, and financial needs. When selected wisely, it supports financial stability and help create a secure, stress-free, and comfortable retirement life overall.

Frequently Asked Questions (FAQs)

Q1. How does an annuity generate income?

Answer: An annuity generates income by investing your contributions and later distributing the accumulated amount as periodic payments.

Q2. Are annuities safe investments?

Answer: They are generally considered safe, especially fixed annuities, as they provide guaranteed returns and stable income.

Q3. Can I withdraw money from an annuity anytime?

Answer: No, annuities have limited liquidity, and early withdrawals may result in penalties and reduced benefits.

Q4. What are the risks associated with annuities?

Answer: Risks include inflation reducing purchasing power, high fees in some plans, and lower returns compared to market-linked investments.

Recommended Articles

We hope that this EDUCBA information on “Annuity” was beneficial to you. You can view EDUCBA’s recommended articles for more information.