What is a Floating Charge?

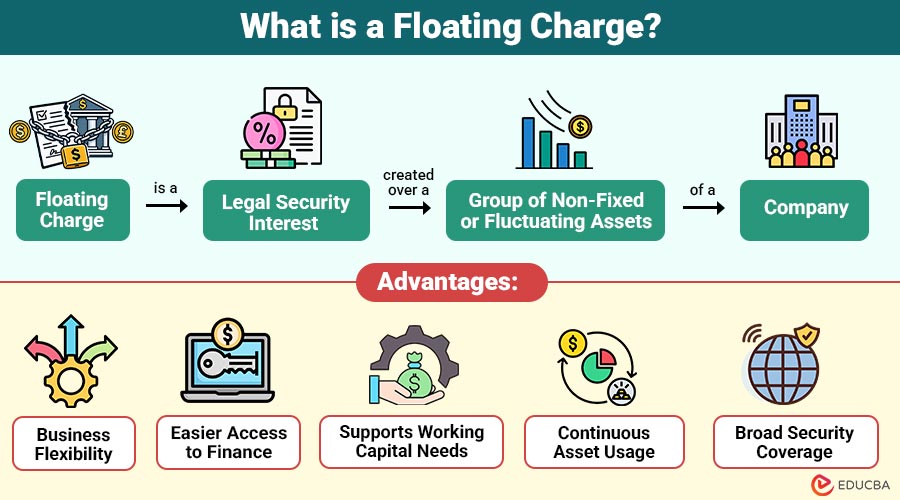

A floating charge is a legal security interest created over a group of non-fixed or fluctuating assets of a company. The company can continue to use and deal with these assets until certain events occur, such as a loan default, liquidation, or insolvency. When such triggering events occur, the floating charge becomes fixed on the assets. This process is known as crystallization.

Table of Contents:

- Meaning

- Importance

- Features

- Working

- Difference

- Crystallization of Floating Charge

- Advantages

- Disadvantages

- Examples

- Legal Requirements

Key Takeaways:

- A floating charge provides lenders with flexible security over changing company assets, effectively and widely.

- Crystallization converts a floating charge into a fixed security during insolvency or default events occurring.

- The borrower retains control over the assets until the triggering event occurs under the legal framework.

- Lenders receive lower priority than fixed charge-holders in the insolvency proceedings distribution hierarchy.

Importance of Floating Charge

Here are the points highlighting its importance in supporting business financing, operations, and creditor protection:

1. Facilitates Corporate Borrowing

It helps companies obtain financing easily by offering flexible security over movable-asset-based financing.

2. Promotes Business Growth

Borrowed funds secured by floating charges effectively support expansion, investment, and smooth day-to-day operations.

3. Protects Lenders

It provides lenders with legal protection and a security interest in company assets against the risk of default on repayment.

4. Encourages Commercial Activity

Companies can freely trade assets while still maintaining secured financing arrangements without operational restrictions imposed

5. Assists Insolvency Management

Clarify creditors’ priorities and rights during liquidation and insolvency proceedings, ensuring an orderly distribution of assets.

Features of a Floating Charge

Below are the key features that define how a floating charge operates in business and corporate finance.

1. Covers Changing Assets

It covers assets that frequently change in value and quantity, including inventory, stock-in-trade, receivables, cash, and raw materials that are continuously replaced or sold.

2. Company Retains Control

The borrower company retains control and continues to use the charged assets without lender approval for each transaction, providing flexibility compared to fixed charge arrangements.

3. Security for Loans

They are widely used as collateral security for business loans, debentures, and working capital financing across various commercial lending arrangements.

4. Crystallization

Crystallization occurs when a floating charge becomes fixed upon events such as default, insolvency, liquidation, or the appointment of a receiver, restricting the company’s ability to deal with its assets.

5. Applies to a Class of Assets

It applies to a general class of assets rather than a specific asset, covering an entire pool of business resources.

6. Priority in Insolvency

During insolvency proceedings, holders rank ahead of fixed charge holders and above unsecured creditors in the priority for repayment of outstanding debts.

How Does a Floating Charge Work?

The functioning can be understood in several stages.

Step 1: Creation of Charge

A company borrows money and creates a floating charge over its fluctuating assets, such as inventory and receivables.

Step 2: Normal Business Operations

The company continues normal business operations using assets freely, while the lender does not interfere in the management of daily activities

Step 3: Triggering Event Occurs

If the company defaults or becomes insolvent, the floating charge crystallizes and becomes enforceable over secured assets immediately, effective

Step 4: Conversion into Fixed Charge

After crystallization, assets become fixed security; the company loses control, and the lender can legally enforce a charge against them.

Step 5: Debt Recovery

The lender may sell assets, appoint a receiver, and recover debt from the proceeds of the asset liquidation process on an applicable basis.

Difference Between Floating Charge and Fixed Charge

The table below highlights the key differences between both.

| Basis | Floating Charge | Fixed Charge |

| Asset Type | Changing assets | Specific assets |

| Control | The borrower retains control | The lender has greater control |

| Flexibility | High | Limited |

| Disposal of Assets | Allowed during business | Restricted |

| Crystallization | Applicable | Not applicable |

| Risk Level | Higher | Lower |

| Examples | Inventory, receivables | Land, machinery |

Crystallization of Floating Charge

Crystallization is process by which a floating charge becomes a fixed charge.

1. Default in Loan Repayment

Failure to repay the loan on time triggers the crystallization of the floating charge over the secured assets immediately

2. Company Liquidation

When a company enters liquidation, a floating charge automatically crystallizes and converts into a fixed security over assets

3. Appointment of Receiver

If the receiver is appointed, a floating charge crystallizes immediately, and the lender gains control over secured assets

4. Business Closure

When a business ceases operations, a floating charge crystallizes, and the lender immediately enforces security over the company’s assets.

5. Contractual Provisions

Loan agreements may specify additional triggering events that cause crystallization of the floating charge, as agreed upon in the terms.

Advantages of a Floating Charge

Here are the key advantages that makes it a flexible and widely used form of security in business financing.

1. Business Flexibility

Companies continue normal trading operations, freely using assets without lender restrictions.

2. Easier Access to Finance

Businesses obtain loans easily, even without substantial fixed assets as collateral.

3. Supports Working Capital Needs

It helps finance day-to-day operational expenses and working capital requirements effectively.

4. Continuous Asset Usage

Companies freely use to sell and replace inventory and receivables while maintaining ongoing business operations.

5. Broad Security Coverage

Lenders receive security over the entire class of current and future assets, ensuring broad protection.

Disadvantages of a Floating Charge

Here are the disadvantages that can affect both lenders and borrowers in secured transactions.

1. Lower Priority

Holders rank below fixed charge holders during the insolvency distribution of company assets legally

2. Asset Value Fluctuation

The value of floating assets can change frequently and may decline unexpectedly, affecting overall security strength.

3. Higher Risk for Lenders

The borrower retains control over assets, increasing uncertainty and significantly raising risk exposure for lending institutions.

4. Complex Enforcement

The debt recovery process becomes legally complex and time-consuming during insolvency proceedings or liquidation situations.

5. Possible Insufficient Security

By default, remaining assets may be inadequate to fully repay outstanding loan or secured debt obligations.

Examples of Floating Charge

Here are some practical illustrations that show how it is commonly used across different types of businesses.

1. Retail Business

A retail company takes a bank loan secured by its inventory. The company continuously sells and replaces goods. The floating charge remains over the changing stock until repayment failure occurs.

2. Manufacturing Company

A manufacturer grants a floating charge over raw materials and receivables to obtain working capital financing.

3. Wholesale Distributor

A distributor secures a loan using warehouse inventory, which fluctuates daily based on sales and purchases.

Legal Requirements

Here are the key legal requirements that must be met to create a valid floating charge under applicable law.

1. Written Agreement

A floating charge must be created through a formal written contract clearly stating the terms between the lender and borrower parties

2. Registration

The charge must be registered with the authorities within the prescribed time, failing which it may become invalid against creditors legally

3. Clear Identification of Assets

An agreement must define the class of assets covered, such as inventory, receivables, or current assets, for legal clarity purposes

4. Compliance with Corporate Laws

It must comply with company and insolvency laws, ensuring validity, enforceability, and legal recognition under jurisdiction rules

Final Thoughts

A floating charge is a flexible security allowing companies to raise finance using changing assets while continuing operations. It strikes balance between the interests of lenders and borrowers and plays a vital role in deciding creditor priority during insolvency. Though useful, it carries risks like fluctuating asset values and a lower ranking. It remains vital in modern corporate finance.

Frequently Asked Questions (FAQs)

Q1. When does a floating charge become fixed?

Answer: It becomes fixed during events like loan default, insolvency, liquidation, or appointment of a receiver. This process is called crystallization.

Q2. Why do lenders use floating charges?

Answer: Lenders use floating charges because they provide security over a wide range of business assets while allowing the borrower to continue normal operations.

Q3. Who has control over assets under a floating charge?

Answer: The borrower company retains control and can freely use, sell, or replace the assets until crystallization occurs.

Q4. Is a floating charge risky for lenders?

Answer: Yes, it carries a higher risk because asset values fluctuate, and the borrower can deal with the assets until crystallization, which may reduce recoverable value.

Recommended Articles

We hope that this EDUCBA information on “Floating Charge” was beneficial to you. You can view EDUCBA’s recommended articles for more information.