What is Financial Planning?

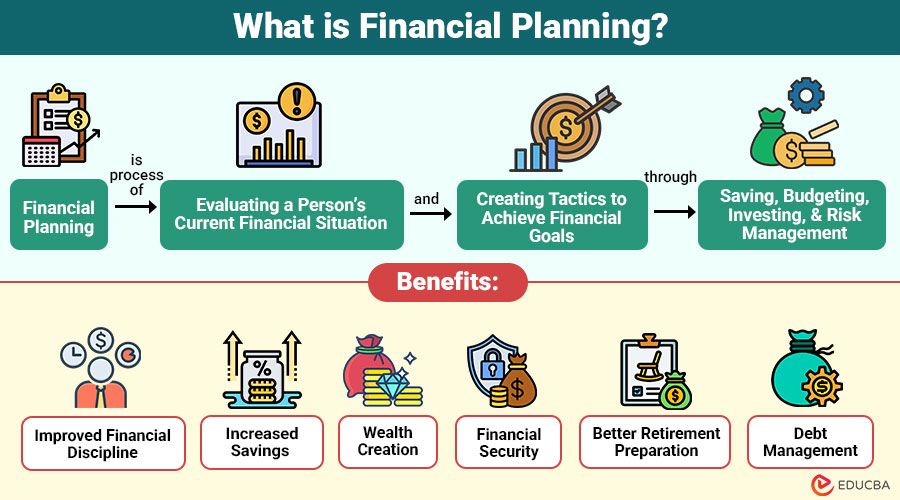

Financial planning is process of evaluating a person’s current financial situation and creating tactics to achieve financial goals through saving, budgeting, investing, and risk management. It helps individuals allocate their resources effectively while preparing for future financial needs such as education, home ownership, retirement, or emergencies.

Table of Contents:

- Meaning

- Importance

- Key Components

- Types

- Process

- Benefits

- Strategies

- Common Mistakes

- Tools

- Real-World Example

Key Takeaways:

- Financial planning helps individuals manage income, control expenses, build savings, and achieve financial security effectively.

- Setting clear financial goals and following structured plans improve decision-making, reduce risk, and support stability.

- Regular saving, early investing, and proper risk management allow money to grow steadily through compounding.

- Reviewing financial plans periodically ensures adjustments for life changes, economic conditions, and evolving personal goals.

Importance of Financial Planning

Here are the key reasons why it is important for individuals and organizations.

1. Better Money Management

Helps individuals track their income and expenses, ensuring that money is used efficiently.

2. Goal Achievement

Whether it is purchasing property, starting a business, or planning retirement, planning helps prioritize and achieve these goals.

3. Emergency Preparedness

A successful financial plan includes emergency funds to handle unexpected events such as medical emergencies, job loss, or economic downturns.

4. Reduced Financial Stress

Proper planning provides financial clarity and reduces anxiety related to money management.

5. Improved Investment Decisions

Assists people in selecting investments that complement their financial goals and risk tolerance.

Key Components of Financial Planning

Consists of several components that work together to create a comprehensive financial strategy.

1. Budgeting

Budgeting is the foundation. It involves tracking income and expenses to ensure spending does not exceed earnings. A budget helps individuals identify unnecessary expenses and allocate funds toward savings and investments.

2. Saving

Saving money is an essential part. It entails allocating a percentage of income for unforeseen expenses like crises, significant purchases, or schooling.

3. Investment Planning

The primary objective of investment planning is to make investments in financial instruments such as stocks, bonds, mutual funds, or real estate. Effective investing techniques enable people to produce long-term financial gains.

4. Risk Management

Risk management entails using insurance plans, such as life, health, or property insurance, to safeguard financial assets against unforeseen circumstances.

5. Retirement Planning

Retirement planning guarantees that people have enough money to support their way of life once they retire. It involves long-term investments and savings plans designed to generate retirement income.

6. Tax Planning

Tax planning helps individuals legally reduce their tax liabilities by taking advantage of deductions, exemptions, and tax-saving investment options.

7. Estate Planning

Estate planning guarantees that a person’s assets are allocated in accordance with their final desires. Wills, trusts, and other legal documents might be involved.

Types of Financial Planning

It can be categorized by financial goals and time horizons.

1. Short-Term

Short-term planning focuses on financial goals that can be achieved within one to three years. Creating an emergency fund or settling minor debts are two examples.

2. Medium-Term

Medium-term planning typically covers goals that require three to ten years, such as buying a car or saving for children’s education.

3. Long-Term

Long-term focuses on goals that take more than ten years to achieve, such as retirement planning or wealth creation.

Financial Planning Process

Follows a structured process to ensure effective results.

1. Assessing the Current Financial Situation

This step involves evaluating income, expenses, savings, assets, debts, insurance, and investments to clearly understand the individual’s present financial health and stability.

2. Setting Financial Goals

In this step, individuals define clear, realistic, and measurable short-term and long-term financial goals to guide their saving, spending, investing, and overall financial decisions.

3. Developing a Financial Plan

A structured financial plan is created, including budgeting, saving strategies, investment options, risk management, and tax planning to achieve the defined financial goals efficiently.

4. Implementing the Plan

This step involves putting the financial plan into action by following the budget, investing regularly, controlling expenses, and consistently applying recommended financial strategies.

5. Monitoring and Reviewing

Requires regular review of income, expenses, investments, and goals to make necessary adjustments in response to life changes, risks, and economic conditions.

Benefits of Financial Planning

Offers numerous advantages for individuals and businesses.

1. Improved Financial Discipline

Promotes responsible spending habits, controlled budgeting, and regular saving, helping individuals maintain discipline and avoid unnecessary expenses or financial mistakes.

2. Increased Savings

A proper financial plan encourages consistent saving by setting clear targets, helping individuals build emergency funds, and prepare for future financial needs effectively.

3. Wealth Creation

Helps individuals choose suitable investment options, manage risks, and grow their money steadily over time to achieve long-term wealth and stability.

4. Financial Security

With proper financial planning, individuals can prepare for unexpected situations by maintaining savings, insurance, and emergency funds to ensure financial stability during difficult times.

5. Better Retirement Preparation

Long-term helps individuals invest and save regularly, ensuring they have sufficient funds to maintain a comfortable, secure lifestyle after retirement.

6. Debt Management

Helps track liabilities, manage borrowing, and develop repayment strategies, allowing individuals to reduce their debt burden and maintain a healthy financial condition.

Financial Planning Strategies

To achieve financial success, individuals should adopt practical strategies.

1. Create a Realistic Budget

A realistic budget helps track income, control expenses, avoid overspending, and ensure proper allocation of money for savings and investments.

2. Build an Emergency Fund

Saving three to six months of living expenses as emergency funds provides financial support during unexpected situations like job loss or emergencies.

3. Diversify Investments

Investing in variety of asset classes, including stocks, bonds, and real estate, lowers risk and raises the possibility of steady long-term gains.

4. Manage Debt Wisely

Avoid unnecessary borrowing, pay high-interest debts first, and maintain a proper repayment plan to reduce financial burden and improve financial stability.

5. Plan for Retirement Early

Starting retirement savings early allows money to grow through compounding, helping individuals build sufficient funds for a comfortable retirement.

6. Review Financial Plans Regularly

Financial situations change over time, so reviewing financial plans regularly helps adjust them to income, expenses, goals, and economic conditions.

Common Financial Planning Mistakes

Many people make mistakes that can affect their stability.

1. Lack of Budgeting

Without a proper budget, individuals may overspend, lose control of finances, and fail to save money for future needs.

2. Ignoring Emergency Funds

Without emergency savings, unexpected expenses like medical bills, repairs, or job loss can cause financial stress.

3. Delaying Investment

Postponing investments reduces the benefit of compounding, limiting long-term wealth growth, and making it harder to achieve future financial goals.

4. Poor Risk Management

Failing to purchase adequate insurance coverage can result in serious financial loss due to accidents, illness, property damage, or other unexpected emergencies.

5. Not Reviewing Financial Plans

Financial plans should be reviewed regularly to adjust goals, investments, and budgets in response to changing income, expenses, and life circumstances.

Financial Planning Tools

Various tools can help individuals manage their finances effectively.

1. Lack of Budgeting

Without a proper budget, individuals may overspend, lose control of finances, and fail to save money for future needs.

2. Ignoring Emergency Funds

Lack of emergency savings can create financial stress when unexpected expenses such as medical bills, repairs, or job loss occur.

3. Delaying Investment

Postponing investments reduces the benefit of compounding, limiting long-term wealth growth, and making it harder to achieve future financial goals.

4. Poor Risk Management

Failing to purchase adequate insurance coverage can result in serious financial loss due to accidents, illness, property damage, or other unexpected emergencies.

5. Not Reviewing Financial Plans

Should be reviewed regularly to adjust goals, investments, and budgets in response to changing income, expenses, and life circumstances.

Real-World Example

Consider a young professional who earns a stable monthly income. Through financial planning, they allocate their income into different categories such as living expenses, savings, investments, and insurance.

They build an emergency fund, invest in retirement plans, and gradually increase their investment portfolio. Over time, disciplined financial planning helps them achieve financial independence and long-term wealth.

Final Thoughts

Financial planning is an important process for achieving financial stability and long-term prosperity. By effectively managing income, expenses, investments, and risks, individuals can build a secure financial future. A well-structured financial plan helps individuals achieve life goals, handle financial emergencies, and prepare for retirement. By adopting disciplined saving habits, making informed investment decisions, and regularly reviewing financial plans, individuals can ensure sustainable financial growth and stability.

Frequently Asked Questions (FAQs)

Q1. What is the first step in financial planning?

Answer: First step is assessing the current financial situation by analyzing assets, income, expenses, debts, and savings.

Q2. When should someone start financial planning?

Answer: Should start as early as possible to maximize savings and investment growth over time.

Q3. How often should financial plans be reviewed?

Answer: It should ideally be reviewed at least once a year or whenever major life changes occur.

Q4. Is financial planning only for high-income individuals?

Answer: No, it is important for everyone regardless of income level, as it helps manage money wisely and achieve financial stability.

Recommended Articles

We hope that this EDUCBA information on “Financial Planning” was beneficial to you. You can view EDUCBA’s recommended articles for more information.