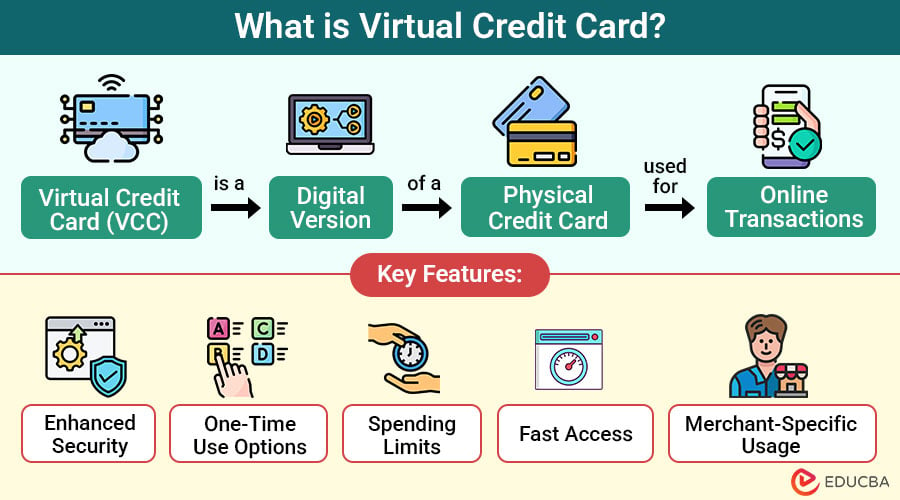

What is a Virtual Credit Card?

A Virtual Credit Card (VCC) is a digital version of a physical credit card, used primarily for online transactions.

It is generated via the app or website of your bank and includes a unique card number, expiration date, and CVV. Unlike a physical card, it does not exist in a tangible form and is designed for temporary or limited use, offering enhanced security and control. Virtual cards help protect your real card details from fraud, especially during online shopping, subscriptions, or when dealing with unfamiliar merchants.

Table of Contents:

- Meaning

- Working

- Benefits

- Differences

- Popular Banks Offering Virtual Credit Cards

- How to Get a Virtual Credit Card?

- Use Cases

- Safety Tips

Key Takeaways:

- Virtual credit cards enhance online payment security by masking your real card details during transactions.

- They offer customizable features, such as spending limits, expiration dates, and merchant-specific usage, for better control.

- Ideal for subscriptions, online shopping, and business use, preventing unauthorized charges or recurring payments.

- Virtual cards are instantly available through banking apps, eliminating the wait times associated with physical card delivery.

How Does a Virtual Credit Card Work?

The process is simple and user-friendly. Here is how it typically works:

1. Issuance

Access your bank or credit card provider’s app or website, then select the option to generate a virtual card. Many services offer instant setup upon approval.

2. Generation

For your virtual card, a distinct card number, expiration date, and CVV are generated. These credentials differ from your physical card and can be used securely for online transactions.

3. Usage

Enter your virtual card’s details at checkout for online purchases. It provides a secure and practical digital payment option and functions exactly like a conventional credit card.

4. Control Settings

Many virtual cards offer features such as setting transaction limits, blocking specific merchants, or selecting expiration dates. These controls enhance security and let users customize card usage precisely.

5. Expiry or Deactivation

Virtual cards expire automatically after a transaction or after a specified time, thereby reducing the risk of fraud. This temporary nature makes them safer for one-time purchases or unfamiliar websites.

Key Features of Virtual Credit Cards

Virtual credit cards offer a host of features that make them ideal for modern consumers. Some of the most notable include:

1. Enhanced Security

Virtual cards use randomized numbers distinct from those on your physical card, ensuring intercepted details become useless quickly and offering strong protection against fraud and online theft attempts.

2. One-Time Use Options

Some cards are valid for only a single transaction, making them ineffective for subsequent use and ideal for safer one-time or high-risk online purchases.

3. Spending Limits

You can set specific transaction or daily limits on your virtual card, helping control expenses, avoid unauthorized charges, and stick to a strict budget plan.

4. Fast Access

It enable consumers to shop online without expecting a physical card to arrive in the mail because they are instantaneously accessible through banking apps or websites.

5. Merchant-Specific Usage

Assign a virtual card to a specific vendor or subscription service, helping prevent accidental renewals, misuse, or charges from unauthorized or unfamiliar merchants.

Benefits of Using a Virtual Credit Card

Using a card can significantly improve your online transaction experience. Here is why:

1. Fraud Protection

Virtual cards do not expose your actual card number, even if your virtual card details are stolen, your main account remains safe.

2. Safe for Subscriptions

Set expiration dates or usage limits on virtual cards used for free trials or subscription services to avoid unwanted auto-renewals.

3. Ideal for International Transactions

Worried about foreign websites or unknown vendors? Use a VCC to minimize the risk associated with sharing your real card data.

4. Easy Deactivation

You can deactivate a virtual card instantly without canceling your main account, making it a convenient tool for managing digital spending.

5. Track Spending Efficiently

Most VCC platforms provide clear reports of virtual card transactions, helping with budgeting and financial planning.

Difference Between Virtual Credit Card and Physical Credit Card

Below is a clear comparison highlighting the key differences between virtual and physical credit card:

| Feature | Virtual Credit Card | Physical Credit Card |

| Tangibility | Digital only | Physical card issued |

| Security | High (temporary/limited use) | Standard (permanent number) |

| Ideal Use | Online/phone transactions | In-store and online |

| Risk | Lower (masking the real card number) | Higher (exposed data) |

| Availability | Instant (in many cases) | Requires shipping |

Popular Banks and Fintechs Offering Virtual Credit Cards

Many global and local financial institutions now offer Virtual Currency Control (VCC) services. Some notable providers include:

1. Capital One Eno

Eno is a browser extension from Capital One that instantly generates secure virtual card numbers for online purchases, enhancing privacy and reducing fraud risks.

2. Citi Virtual Account Numbers

Citi customers can create virtual card numbers directly from their online accounts, allowing safer online shopping without exposing their actual credit card information.

3. American Express

American Express collaborates with digital wallets to provide tokenized virtual card details, offering added security for online payments across supported platforms and devices.

4. Revolut, Wise, and Payoneer

These fintech platforms offer virtual cards that are favored by global users and freelancers for international transactions, expense management, and enhanced security when shopping or working online.

5. HDFC Bank

HDFC’s NetSafe virtual card enables users to generate temporary card details for online payments, providing an added layer of safety without exposing their main account credentials.

6. SBI and ICICI

Through internet banking, SBI and ICICI customers can generate virtual cards for secure online use, protecting actual card data during digital transactions.

How to Get a Virtual Credit Card?

Getting a virtual credit card is relatively straightforward. Follow these general steps:

1. Check Eligibility

Confirm that your bank or credit card provider supports virtual cards. Not all institutions offer this service, so it is important to verify beforehand.

2. Log In to the Account

Access your internet banking portal or mobile app using your credentials to begin the process of creating a secure virtual credit card.

3. Select Virtual Card Option

Navigate to the card services or digital banking section, then select the option for creating or managing a virtual credit card.

4. Generate Card

Provide the necessary inputs, such as the transaction amount, validity period, or specific merchant details, and then proceed to generate your card instantly.

5. Start Using

Once generated, use the virtual card details (number, CVV, expiration date) for secure online payments and subscriptions.

Use Cases for Virtual Credit Cards

Virtual cards are not just a trendy innovation—they solve real-world problems.

1. Online Shopping

When buying on unknown or foreign websites, use virtual cards to safeguard your primary card, lowering the possibility of data breaches and illegal transactions.

2. Mobile Subscriptions

Ideal for managing app store purchases, streaming services, or free trial subscriptions. Cancel or expire the virtual card to avoid unexpected renewals or charges.

3. Student Expenses

Parents can create virtual cards with spending limits for children, offering a secure way to teach financial responsibility while controlling online purchases and subscriptions.

4. Business Transactions

Companies issue virtual cards to employees for software tools or subscriptions, enabling transaction tracking, budget control, and preventing unauthorized use of the company’s main account.

Safety Tips for Using Virtual Credit Cards

Although designers create cards with security in mind, users should still follow safety tips:

1. Use Secure Networks

Always ensure you are connected to a secure, private network when making online purchases to prevent data theft or hacking attempts.

2. Avoid Saving Card Details

Do not save card information on websites or browsers unless necessary to minimize the risk of unauthorized access.

3. Monitor Transactions

Regularly check your bank account and card statements for unusual activity to quickly identify and report any unauthorized or suspicious transactions.

4. Set Controls

Choose virtual cards with expiration dates or merchant-specific limits to control where and how you use your card.

5. Deactivate Unused Cards

Immediately deactivate any virtual cards you no longer need to reduce potential vulnerabilities and maintain tighter control over your digital finances.

Final Thoughts

A virtual credit card offers a powerful blend of convenience, security, and control for online transactions. Whether you are a frequent online shopper, a subscription manager, or someone simply looking for safer financial tools, VCCs are an excellent addition to your digital wallet. As financial technology continues to evolve, adopting tools like virtual credit cards is not just smart—it is essential.

Frequently Asked Questions (FAQs)

Q1: Is it possible to use a virtual credit card for in-store purchases?

Answer: Most virtual credit cards are intended for online or phone transactions only. Some digital wallets (like Google Pay or Apple Pay) allow users to use tokenized virtual cards in-store by linking them to a contactless payment method.

Q2: Does using a Virtual Credit Card affect my credit score?

Answer: Using a virtual credit card does not directly impact your credit score. It functions as an extension of your existing credit account, so only your overall card usage, payment history, and credit behavior influence your score.

Q3: Can I get a Virtual Credit Card without having a physical credit card?

Answer: Yes, some fintech platforms and banks offer standalone virtual cards linked to your bank account or prepaid balance, without requiring a physical credit card. However, traditional banks often issue VCCs only to existing credit cardholders.

Q4: What happens if a refund is issued to a Virtual Credit Card?

Answer: Refunds to a virtual credit card typically go back to the source account (your main credit or bank account), even if the virtual card is expired or deactivated. The bank tracks transactions internally to ensure correct crediting.

Recommended Articles

We hope that this EDUCBA information on “Virtual Credit Card” was beneficial to you. You can view EDUCBA’s recommended articles for more information.