What Is a Cash Generating Unit (CGU)?

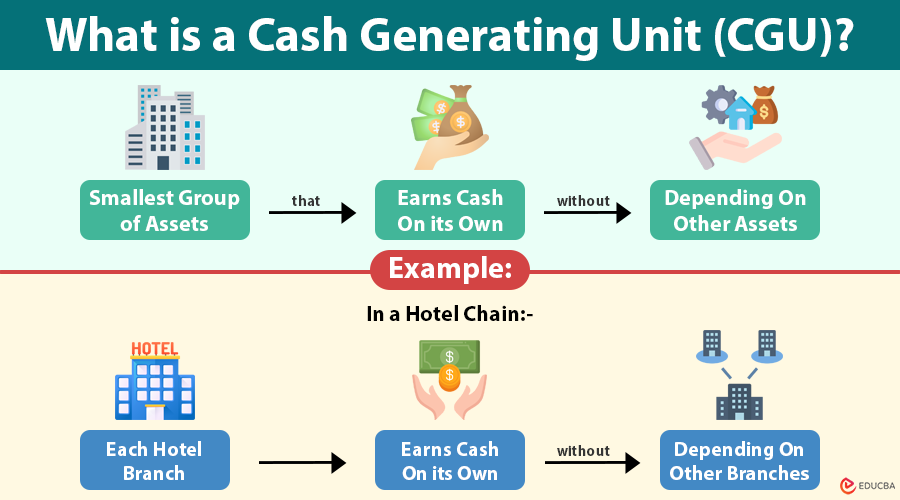

A Cash Generating Unit (CGU) is the smallest group of assets that generates cash independently, separate from other assets.

In simpler terms, a Cash Generating Unit is the lowest level where management monitors how assets generate cash. It helps management ensure that the recorded asset values do not exceed their recoverable amounts.

IAS 36 – Impairment of Assets under IFRS rules defines this concept and makes it important for financial reporting.

Identifying CGUs ensures that companies evaluate the value of their assets at the most realistic operational level, neither too broadly nor too narrowly.

Table of Contents

- Meaning

- Understanding the Concept

- Key Characteristics

- Why Are CGUs Important?

- How to Determine?

- Impairment Testing

- Cash Generating Units and Goodwill

- Challenges in Identifying CGUs

- Best Practices for CGU Identification and Testing

Understanding the Concept of a Cash Generating Unit

In most businesses, a single asset rarely generates cash on its own. For example, a conveyor belt or a single machine in a production line might not independently earn revenue without the other machines, staff, and supporting systems.

To address this, IFRS requires companies to identify the group of assets that collectively produce independent cash inflows, which becomes the Cash Generating Unit.

Example 1

A manufacturing company produces steel using multiple interdependent machines. The machines rely on each other, and none generates independent cash inflows. The company treats the entire production plant as one CGU.

Example 2

A retail company owns 25 stores across different cities. Each store has its own cash register, expenses, and management team. Since each store independently generates revenue, we can treat each store as a separate CGU.

By determining CGUs correctly, companies can assess which parts of their business are creating value and which may be losing money or facing impairment.

Key Characteristics of a Cash Generating Unit

A well-defined Cash Generating Unit shares certain fundamental traits that make it identifiable and measurable:

- Independent cash inflows: The primary feature of a CGU is that its cash inflows are largely independent of other units. It should be possible to track and forecast its earnings without interference from other operations.

- Operational interdependence: While assets inside a CGU depend on each other, the unit as a whole must function independently from other parts of the business.

- Consistent monitoring level: Management must use the same level of grouping for monitoring performance and for impairment testing to maintain consistency across reporting periods.

- Granularity and practicality: The CGU should not be defined too broadly (such as an entire corporation) or too narrowly (such as a single asset). It should reflect how management actually runs and evaluates business performance.

- Stable structure over time: Once defined, CGUs should remain consistent year after year, unless significant structural or operational changes occur.

Why Are Cash Generating Units Important?

1. Accurate Impairment Testing

CGUs allow organizations to perform impairment tests more accurately. Instead of evaluating every individual asset, companies assess whether the combined group of assets is generating sufficient value to justify its carrying amount.

Without CGUs, impairment could be either understated (by grouping assets too broadly) or overstated (by analyzing assets too narrowly).

2. Improved Financial Transparency

CGUs help provide a true and fair view of a company’s financial position. They allow investors, auditors, and regulators to understand which parts of the organization are profitable and which are underperforming.

3. Compliance with IFRS Standards

Under IAS 36, identifying CGUs is mandatory for impairment testing. Non-compliance can lead to misstated financial results and audit qualifications.

4. Better Strategic Decision-Making

CGU-level data helps management identify strong and weak areas within the business. This insight can guide investment decisions, asset disposals, or restructuring plans.

5. Fair Allocation of Goodwill

When companies acquire new businesses, they allocate goodwill to the CGUs that benefit from the acquisition. Accurate CGU identification ensures fair and consistent goodwill impairment testing.

How to Determine a Cash Generating Unit?

Identifying a Cash Generating Unit requires both financial analysis and professional judgment. According to IAS 36, companies must analyze how they generate, manage, and monitor cash flows.

Steps to Identify a CGU:

- Assess cash flow sources: Determine which assets or groups of assets produce distinct cash inflows.

- Review internal reporting structure: Look at how management tracks performance internally. CGUs often align with business segments, profit centers, or divisions.

- Evaluate market factors: Determine whether the products or services are sold in distinct markets or rely on a common customer base.

- Consider interdependencies: If two assets or groups cannot generate cash without one another, they belong to the same CGU.

- Review historical and forecast data: Use historical performance and projected financial statements to validate that the unit can generate independent cash inflows.

Impairment Testing for CGUs

Once companies identify CGUs, they must regularly test them for impairment to ensure that the carrying amount of each CGU does not exceed its recoverable amount.

- Carrying amount: The total book value of assets (after depreciation and amortization) included in the CGU.

- Recoverable amount: The higher of:

- Fair Value Less Costs of Disposal (FVLCD)

- Value in Use (VIU) – the present value of expected future cash flows from the CGU.

Steps in CGU Impairment Testing

- Identify indicators of impairment: Triggers could include declining sales, obsolescence, economic downturns, or regulatory changes.

- Calculate carrying amount: Sum the book values of all assets within the CGU, including goodwill (if applicable).

- Estimate recoverable amount: Forecast future cash flows and discount them to present value (using VIU) or determine market value (using FVLCD).

- Compare calues:

- If carrying amount > recoverable amount, the CGU is impaired.

- If carrying amount ≤ recoverable amount, no record of impairment.

- Allocate impairment losses: Apply impairment losses first to goodwill, then distribute the remaining amount proportionately among other assets in the CGU.

Example of Cash Generating Unit Impairment Testing

Scenario:

A technology company operates three divisions: Software, Hardware, and Cloud Services.

The Hardware division (a CGU) has a carrying amount of $100 million.

Due to declining demand, analysts estimate its recoverable amount at $85 million.

Calculation:

Impairment Loss = $100M – $85M = $15M

Recognize this $15 million loss as an expense in the income statement and apply it first to goodwill, then distribute the remaining amount proportionately among other assets within the Hardware CGU.

Cash Generating Units and Goodwill

When a company acquires a business, it creates goodwill by paying a premium above the fair value of the acquired net assets. Under IAS 36, companies must always test goodwill for impairment at the CGU level.

Assign goodwill to the CGUs or groups of CGUs that will benefit from the acquisition. This ensures that impairment testing reflects the economic benefits of the acquired business.

Challenges in Identifying CGUs

- Shared corporate assets: Assets such as headquarters, brand names, or IT systems support multiple CGUs and do not generate direct cash inflows, which complicates allocation.

- Integrated operations: Post-merger, combining overlapping processes can blur the boundaries between CGUs.

- Management structure changes: If a company reorganizes its divisions or changes its internal reporting structure, it may need to redefine its CGUs.

- Goodwill allocation complexity: Allocating goodwill fairly among multiple CGUs often requires significant estimation and professional judgment.

Best Practices for CGU Identification and Testing

- Align with management view: Ensure CGUs reflect how management monitors business performance.

- Maintain consistency: Use the same CGU structure each year unless major changes occur.

- Document assumptions: Keep detailed records showing how you identified CGUs and calculated impairment.

- Perform a sensitivity analysis: Test key assumptions, such as the discount rate, growth rate, and cash flow projections.

- Comply with disclosure requirements: Disclose key assumptions, impairment losses, and CGU recoverable amounts in financial statements as per IAS 36.

Final Thoughts

A Cash Generating Unit (CGU) is a cornerstone of modern financial reporting and impairment testing under IFRS.

By defining CGUs accurately, businesses ensure transparency, compliance, and realistic valuation of assets.

Proper CGU identification not only fulfills accounting standards but also provides deeper insights into operational performance, helping management make informed, strategic decisions about the company’s future direction.

Frequently Asked Questions (FAQs)

Q1. Can one asset be treated as a Cash Generating Unit?

Answer: Yes, if a single asset generates cash inflows that are largely independent of other assets. For example, a toll bridge or a power plant with its own revenue stream can be considered an individual CGU.

Q2. How do shared corporate assets fit into CGU impairment testing?

Answer: Shared assets, such as corporate offices or IT systems, do not generate independent cash flows. Companies allocate these assets to multiple CGUs on a reasonable and consistent basis (such as usage, revenue contribution, or headcount) during impairment testing.

Q3. Can a company change how it defines its CGUs?

Answer: Yes, but only if there is a significant change in the company’s structure, operations, or internal reporting. Any change must be justified, disclosed, and applied consistently in future reporting periods.

Q4. How do CGUs relate to asset valuation and investment decisions?

Answer: CGU performance helps management identify profitable and unprofitable units. This information supports decisions about expansion, divestment, restructuring, or additional investment.

Q5. Can intangible assets, such as brands or licenses, form a CGU?

Answer: Yes, intangible assets such as brands, customer relationships, or licenses can form a CGU if they generate independent cash inflows, for example, a standalone franchise or a licensed broadcasting channel.

Recommended Articles

We hope this guide on Cash Generating Units (CGUs) helps you understand how businesses assess asset value and test for impairment effectively. Explore these related articles to gain deeper insights into financial reporting, asset valuation, and IFRS compliance: