What are Baby Bonds?

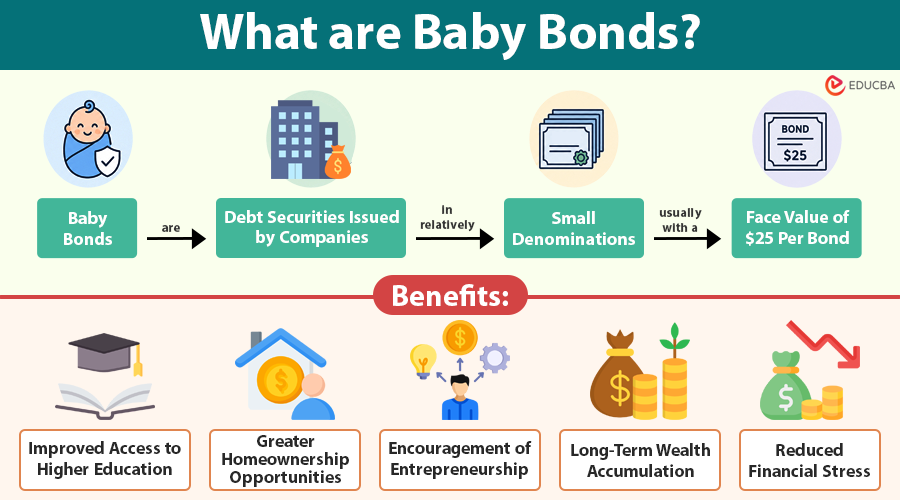

Baby bonds are debt securities issued by companies in relatively small denominations, usually with a face value of $25 per bond. Investors contribute money to the issuing company in exchange for recurring interest payments, just like with regular corporate bonds.

At maturity, the company repays the principal amount to bondholders. Unlike conventional corporate bonds, which often require a $1,000 or more investment, baby bonds are designed primarily for retail investors seeking affordable fixed-income investments.

Example:

Suppose a company issues baby bonds with:

- Face value: $25

- Interest rate: 6% annually

- Maturity period: 10 years

An investor purchasing 100 baby bonds would invest $2,500 and receive annual interest payments based on the coupon rate until maturity.

Table of Contents:

Key Takeaways:

- Baby bonds provide affordable fixed-income investments accessible to individual retail investors.

- Government-funded baby bond programs aim to reduce long-term wealth inequality nationwide.

- Funds typically remain invested until adulthood, benefiting significantly from compound growth.

- It supports education, homeownership, entrepreneurship, and long-term financial stability.

How do Baby Bonds Work?

Although program structures vary, most baby bond initiatives follow a similar framework.

1. Account Creation at Birth

When a child is born, a government agency automatically establishes an investment or trust account in the child’s name.

2. Initial Deposit

A predetermined amount is deposited into the account. Some programs provide equal deposits for all children, while others vary contributions according to family wealth or income.

For example:

- Children from lower-income families may receive larger deposits.

- Children from higher-income families may receive smaller contributions or none at all.

3. Investment Growth

Funds are invested in diversified portfolios, government securities, or other approved investment vehicles to generate long-term growth. Since the money remains invested for many years, compound growth can substantially increase account balances.

4. Restricted Access

Beneficiaries typically cannot withdraw funds during childhood. The restrictions help preserve the account for long-term wealth-building purposes.

5. Access in Adulthood

Upon reaching adulthood, account holders may use the accumulated funds for approved expenditures that support long-term financial stability.

Objectives of Baby Bonds

Baby bond programs are designed to achieve several important economic and social goals:

1. Reduce Wealth Inequality

One of the primary objectives is to narrow wealth gap between high-income and low-income households by providing financial assets to children from disadvantaged backgrounds.

2. Increase Economic Mobility

Offering young adults access to startup capital creates opportunities for higher education, homeownership, entrepreneurship, and long-term financial advancement.

3. Promote Asset Ownership

Encourage individuals to invest in appreciating assets such as homes, educational qualifications, and small businesses, helping build long-term wealth.

4. Support Financial Inclusion

Many low-income families have limited access to savings and investment opportunities. Baby bond programs ensure that every child participates in wealth-building systems regardless of family income.

5. Break Cycles of Intergenerational Poverty

Accumulated savings can help prevent poverty from being passed from one generation to the next, fostering greater financial stability and economic security.

Key Features of Baby Bonds

The following features highlight how baby bond programs are structured and how they support long-term wealth creation for individuals from birth.

1. Government Funding

Baby bond accounts are typically financed through government funds rather than individual family contributions.

2. Universal or Progressive Coverage

Programs may provide benefits to all children universally, or contributions may vary based on family income, with larger deposits for lower-income households.

3. Long-Term Investment

Funds are invested over an extended period, often from birth until early adulthood, allowing savings to grow through compound returns.

4. Restricted Usage

Account holders can generally withdraw funds only for approved purposes such as higher education, homeownership, starting a business, or retirement savings.

5. Asset-Building Focus

Unlike income-support programs, baby bonds are designed to build long-term wealth and improve financial security.

6. Automatic Enrollment

Most baby bond proposals include automatic account creation at birth, ensuring broad participation without requiring families to enroll manually.

Benefits of Baby Bonds

The following benefits demonstrate how it can support financial stability, promote wealth creation, and expand economic opportunities over the long term.

1. Improved Access to Higher Education

To pay for their education, a lot of students rely significantly on loans. By paying for tuition, books, and associated costs, baby bonds can lessen reliance on student debt.

2. Greater Homeownership Opportunities

One of the best strategies for accumulating wealth is still homeownership. Young people may be able to pay for closing fees and down payments with the aid of baby bonds.

3. Encouragement of Entrepreneurship

Starting a business often requires significant capital. It can provide aspiring entrepreneurs with the financial resources necessary to launch ventures.

4. Long-Term Wealth Accumulation

Early investments benefit from compound growth, potentially resulting in substantial savings by adulthood.

5. Reduced Financial Stress

Having access to financial assets can improve economic confidence and reduce stress associated with major life transitions.

Challenges of Baby Bonds

Despite their potential advantages, baby bond programs face several challenges.

1. High Government Costs

Large-scale programs require significant public funding. Policymakers must determine sustainable financing methods.

2. Administrative Complexity

Managing millions of accounts, monitoring investments, and enforcing spending restrictions can create administrative burdens.

3. Political Debate

Baby bond proposals often generate political disagreements regarding government spending, taxation, and social policy priorities.

4. Investment Risk

If accounts are invested in financial markets, returns may fluctuate due to market volatility.

5. Limited Immediate Impact

Since beneficiaries cannot access funds until adulthood, baby bonds do not directly address the immediate financial hardships families face.

Examples of Baby Bond Programs

The following examples illustrate how different governments have implemented or proposed baby bond programs to promote long-term wealth building and financial inclusion.

1. United Kingdom Child Trust Fund

The UK government deposited money into savings accounts for children born between 2002 and 2011, helping them build savings for adulthood.

2. United States Baby Bonds Proposal

Several U.S. policymakers have proposed government-funded accounts for children, with larger contributions provided to children from lower-income families.

3. Connecticut Baby Bonds Program (United States)

In 2023, the state of Connecticut launched a program that deposits funds for eligible newborns enrolled in Medicaid, which can later be used for education, housing, or business purposes.

Final Thoughts

Baby bonds are government-funded accounts designed to reduce wealth inequality by providing children with financial assets from birth. Despite funding and implementation challenges, these programs can enhance economic mobility, support education and homeownership, encourage entrepreneurship, and promote long-term financial inclusion and equity.

Frequently Asked Questions (FAQs)

Q1. Who qualifies for baby bonds?

Answer: Eligibility depends on program rules. Some initiatives cover all children, while others prioritize low-income families.

Q2. When can beneficiaries access baby bond funds?

Answer: Most programs allow access when beneficiaries reach adulthood, typically between ages 18 and 21.

Q3. Are baby bonds the same as savings bonds?

Answer: No. Traditional savings bonds are purchased investments, whereas modern baby bonds are generally government-funded asset-building programs.

Recommended Articles

We hope that this EDUCBA information on “Baby Bonds” was beneficial to you. You can view EDUCBA’s recommended articles for more information.