What is Amortization?

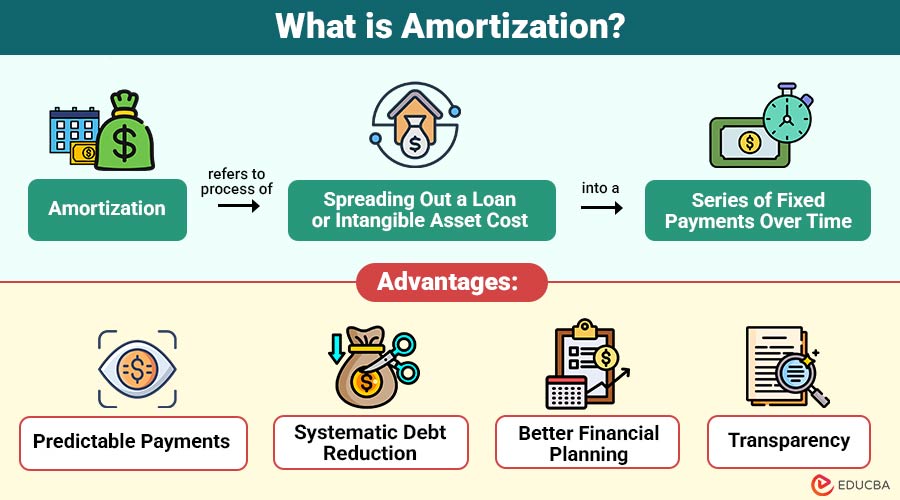

Amortization refers to process of spreading out a loan or intangible asset cost into a series of fixed payments over time. Each payment typically includes both principal repayment and interest expense, gradually reducing the outstanding balance.

In simple terms, amortization ensures that a loan is fully repaid by end of its term through regular payments.

Table of Contents:

Key Takeaways:

- Amortization spreads loan or asset costs into fixed payments, combining principal and interest over a defined period.

- Early payments focus on interest, while later payments increasingly reduce principal, ensuring complete loan repayment by maturity.

- It supports financial planning by offering predictable payments and structured schedules for individuals, businesses, and financial institutions.

- Despite higher initial interest and limited flexibility, amortization remains essential for managing debt and long-term financial stability.

Key Components of Amortization

To understand amortization clearly, you need to know its key components:

1. Principal

The principal is the original amount borrowed or invested, forming the basis for interest calculations and repayment schedules.

2. Interest

Interest is the cost lenders incur for borrowing money, expressed as a percentage rate applied to the outstanding principal balance.

3. Loan Term

A loan term is the agreed-upon repayment period, during which borrowers make payments until the loan is fully repaid.

4. Installment (EMI)

Installment EMI represents fixed payments by the borrower, including principal and interest, ensuring gradual repayment over the loan term.

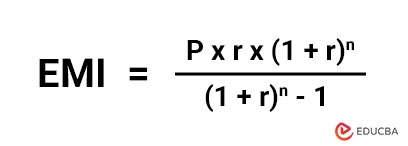

Amortization Formula

Here is the standard formula used to calculate fixed periodic payments for an amortized loan:

Where:

- P = Principal amount

- r = Periodic interest rate

- n = Number of payments

This formula ensures that each payment remains constant while the interest and principal portions vary over time.

How Does Amortization Work?

Amortization works by dividing a loan into equal periodic payments. However, the composition of each payment changes over time:

1. Early Stage

In the early stages, most of each payment goes toward interest because the outstanding principal remains significantly higher.

2. Mid-Stage

During the mid-stage, payments become balanced as the interest portion decreases while the principal repayment portion steadily increases.

3. Later Stage

In the later stage, most of the payment goes toward reducing the principal as interest charges become minimal due to the lower balance. This gradual shift ensures that the loan is completely paid off by the end of the term.

Types of Amortization

Amortization can be categorized into different types based on its application:

1. Loan Amortization

Loan amortization repays borrowed money through fixed periodic installments, gradually and steadily reducing both principal and interest over time.

2. Negative Amortization

Negative amortization occurs when payments are insufficient to cover interest, causing unpaid interest to be added to the principal balance.

3. Amortization of Intangible Assets

Amortization of intangible assets spreads the costs of patents, trademarks, and copyrights over their useful economic life.

4. Balloon Amortization

Balloon amortization features small payments over the term, with a large final lump-sum payment due at maturity.

Real-World Examples

Here are some real-world examples that illustrate how amortization works in different real-life financial scenarios:

1. Home Loan

If you take a ₹50 lakh home loan:

- You pay EMIs monthly

- Initially, interest is higher

- Over time, principal repayment increases

2. Car Loan

A car loan of ₹10 lakh over 5 years:

- Fixed EMIs

- Gradual reduction of the loan balance

3. Business Accounting

A company purchases a patent:

- Cost is amortized over its useful life

- Recorded as an expense annually

Advantages of Amortization

Here are the key advantages that make amortization a valuable method for structured loan repayment and financial management:

1. Predictable Payments

Amortization provides fixed payment amounts, allowing borrowers to plan monthly expenses without uncertainty or unexpected financial surprises.

2. Systematic Debt Reduction

It ensures a gradual reduction of loan balances through structured payments, preventing sudden financial pressure, and maintaining repayment discipline.

3. Better Financial Planning

Helps individuals and businesses create accurate budgets, manage cash flows efficiently, and plan long-term financial goals.

4. Transparency

Schedules provide clear breakdown of principal and interest components, improving understanding and trust in the loan repayment structure.

Limitations of Amortization

Here are the key limitations that should be considered when using amortization for loan repayment and financial planning:

1. High Initial Interest

In the early stages, a larger share of payments goes toward interest rather than principal, significantly reducing the immediate loan balance.

2. Less Flexibility

Fixed installment amounts may not adjust with income changes, making it difficult during periods of financial instability or unexpected expenses.

3. Total Interest Cost

Longer repayment periods increase the overall interest paid, making loans more expensive than shorter-term borrowing options.

4. Complexity

Schedules involve detailed calculations and breakdowns, which can be confusing for beginners without financial knowledge or experience.

5. Early Repayment Penalties

Some amortized loans include prepayment charges, discouraging borrowers from paying off loans early and reducing interest savings.

Use Cases of Amortization

Here are common use cases where amortization plays an important role in financial planning and management:

1. Banking & Finance

Amortization structures loan repayments in banking, ensuring systematic installments that balance principal and interest over a defined loan tenure.

2. Real Estate

In real estate, amortization helps plan mortgage payments, enabling buyers to manage property financing and long-term ownership costs.

3. Corporate Accounting

Businesses use amortization to allocate intangible asset costs systematically, ensuring accurate financial reporting and compliance with accounting standards.

4. Personal Finance

Individuals apply amortization to manage debts efficiently, plan monthly budgets, and achieve financial stability through structured repayment strategies.

5. Student Loans

Amortization helps structure student loan repayments into manageable installments, allowing borrowers to repay education debt gradually over time.

Final Thoughts

Amortization is essential in financial management, as it provides a structured and predictable method for loan repayment and cost allocation. It enhances transparency and financial discipline for individuals and businesses. Despite certain limitations, its advantages outweigh its drawbacks. Understanding amortization helps in better loan management and enables smarter, more informed financial decisions over the long term.

Frequently Asked Questions (FAQs)

Q1. Why is amortization important?

Answer: Amortization is important because it enables structured loan repayment and supports effective financial planning.

Q2. What happens if I miss an amortized loan payment?

Answer: Missing a payment may lead to penalties, increased interest, and a higher outstanding balance, affecting your repayment schedule.

Q3. Is amortization the same as depreciation?

Answer: No, amortization applies to intangible assets and loans, while depreciation applies to physical assets.

Q4. Can amortization reduce interest costs?

Answer: Yes, by making extra payments toward the principal, total interest can be reduced.

Recommended Articles

We hope that this EDUCBA information on “Amortization” was beneficial to you. You can view EDUCBA’s recommended articles for more information.