Many taxpayers in India mix up two very different TDS rules. One is about rent, while the other relates to TDS on Property Purchase. They often assume that crossing the rent threshold changes what they owe when buying a house. This is not true.

These are two separate sections of the Income Tax Act. They have different thresholds, different rates, and different forms. One does not affect the other in any way.

This guide explains the rules for TDS on Property Purchase and TDS on rent in simple terms, helping you understand why these obligations are completely independent and why the common confusion is unfounded.

TDS on Rent: Who Does It Apply To?

There are two sections for TDS on rent in India. Which one applies to you depends on the type of taxpayer you are.

Section 194I covers businesses, companies, and individuals subject to a tax audit. The TDS on rent limit under this section is Rs. 6,00,000 per year. If the rent paid in a year exceeds this amount, TDS must be deducted at 10% on land and buildings and 2% on machinery.

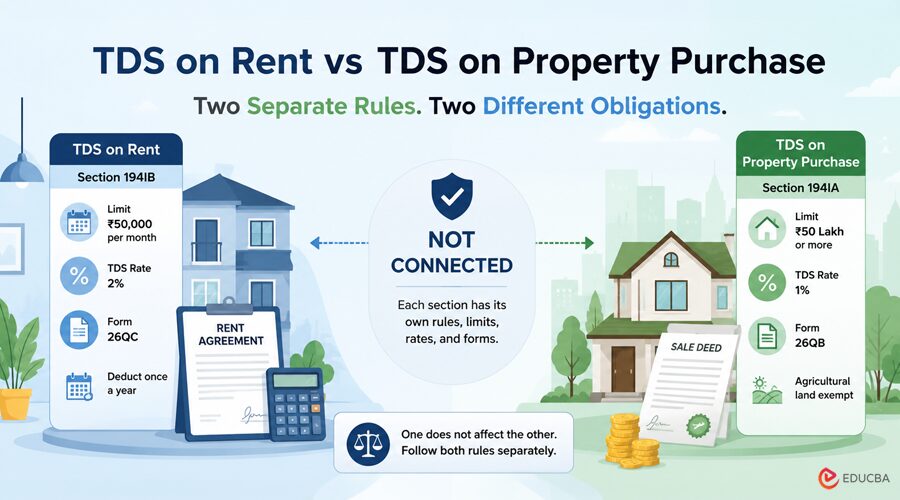

Section 194IB applies to individuals and Hindu Undivided Families (HUFs) that are not subject to a tax audit. This is the section most salaried people fall under. The TDS on rent limit here is Rs. 50,000 per month. If your monthly rent exceeds Rs. 50,000, you must deduct TDS at 2% of the total rent paid for the year.

This 2% rate was updated in late 2024 and is now fully applicable. Earlier it was 5%. Any blog or guide still quoting 5% for Section 194IB is outdated.

The deduction under Section 194IB is done once a year, usually in March or when the tenancy ends.

Here is the updated comparison:

| Section | Applicable To | Threshold | TDS Rate |

| 194I | Businesses and tax audit cases | Rs. 6,00,000 per year | 10% for land and building, 2% for machinery |

| 194IB | Individuals and HUFs not under audit | Rs. 50,000 per month | 2% |

| 194IA | Property buyers | Rs. 50 lakh total value | 1% of the sale value or stamp duty value |

TDS on Property Purchase: How It Works?

When you buy an immovable property worth Rs. 50 lakh or more you must deduct 1% TDS before paying the seller. This is under Section 194IA.

Here is what you need to know:

- The buyer deducts 1% and deposits it with the government

- The form used is Form 26QB, to be filed within 30 days of the month in which the payment was made

- The seller gets credit for this amount when filing their income tax return

- Agricultural land is exempt from this rule.

Two important points that many buyers miss:

First, the 1% TDS is calculated on whichever is higher, the property’s sale price or its stamp duty value. So if you buy a property for Rs. 55 lakh but the stamp duty value is Rs. 62 lakh, the TDS is calculated on Rs. 62 lakh, not Rs. 55 lakh.

Second, if a property is bought jointly by two or more buyers, the TDS on property purchase still applies if the total property value is Rs. 50 lakh or more. You cannot split the transaction to avoid TDS. Even if each co-buyer’s share is below Rs. 50 lakh individually, the rule applies to the full property value.

Why These Two Rules Are Not Connected?

Here is the core myth that needs to be cleared.

A person pays Rs. 60,000 rent per month. They know they have exceeded the Rs. 50,000 TDS limit on rent under Section 194IB and are deducting 2% TDS on their annual rent. Later, they buy a property for Rs. 80 lakh and wonder if their rental TDS rate of 2% somehow carries over or changes what they must deduct on the property.

It does not. Not in any way.

Section 194IB is triggered by rent. A property purchase triggers section 194IA. Depending on the transaction, the section, required forms, and timeline may vary.

Your rent TDS does not reduce your property TDS. Your property TDS does not cancel your rent TDS. No amount paid under one can be adjusted against the other.

The 1% rate on property purchases stays at 1% regardless of the TDS rate you follow for rent. It does not go up. It does not go down.

Why This Confusion Keeps Coming Up?

Two reasons.

One, both involve property. People assume that because rent and property purchase both relate to real estate, the tax rules must be connected somehow. They are not. Tax law looks at each transaction separately.

Two, both involve TDS. Since both require a deduction before payment, people assume the thresholds and rates are related. They do not. Each section has its own rules and works completely independently.

Mistakes to Avoid

These are common errors that happen because of this confusion:

- Trying to set off rental TDS credit against property purchase TDS payable — this is not allowed

- Using the 2% rent TDS rate for a property purchase instead of the correct 1%

- Thinking that never crossing the TDS on rent limit means you are also exempt from property purchase TDS

- Filing Form 26QB late because you thought it was linked to your annual rent TDS filing.

Each compliance is its own task. File each one on time. Do not link them in your head because they involve property.

Final Thoughts

TDS on rent and TDS on Property Purchase are completely separate obligations under the Income Tax Act.

If your monthly rent is above Rs. 50,000, Section 194IB applies, and you deduct 2% of the excess. If you buy a property worth Rs. 50 lakh or more, Section 194IA requires you to deduct 1% TDS on the higher of the property’s sale price or stamp duty value.

Crossing the rent threshold does not change your property TDS. Buying a property does not change your TDS on rent. They are two different rules solving two different problems.

Recommended Articles

We hope this guide on TDS on Property Purchase helps you understand the difference between property purchase TDS and rent TDS, ensuring accurate tax compliance. Explore these recommended articles for more insights on TDS provisions, property taxation, income tax rules, real estate transactions, and tax filing in India.