What is Counterparty Risk?

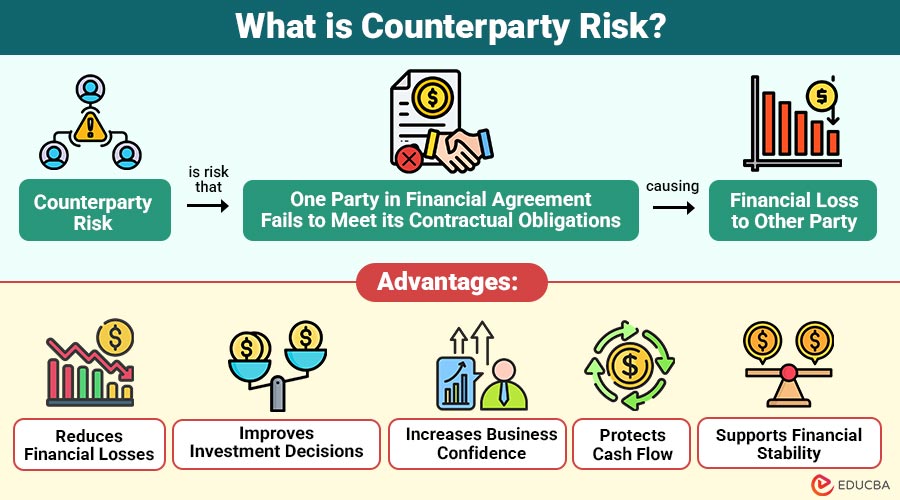

Counterparty risk is risk that one party in a financial agreement fails to meet its contractual obligations, causing financial loss to other party. In simple words, it is the chance that the person, company, or financial institution you are dealing with cannot pay or deliver what they promised.

For example, suppose a company issues bonds, and you invest in them. If the company cannot pay the interest or repay the principal on time, you face counterparty risk.

Table of Contents:

- Meaning

- Key Features

- Working

- Types

- Advantages

- Disadvantages

- Example

- How to Manage Conterparty Risk?

- Applications

Key Takeaways:

- Counterparty risk emerges when a party fails to fulfill agreed-upon financial obligations, resulting in potential losses.

- Creditworthiness, financial stability, and repayment capacity determine the overall level of counterparty risk exposure.

- Diversification, collateral, monitoring, and exposure limits help effectively reduce counterparty risk and financial losses.

- Understanding counterparty risk supports safer investing, lending, and trading, as well as stronger long-term financial decision-making.

Key Features of Counterparty Risk

The following points describe the main key features:

1. Exists in Financial Agreements

It arises whenever two parties enter into a financial agreement involving future payments or contractual obligations.

2. Common Across Financial Markets

It commonly exists in loans, bonds, derivatives, insurance contracts, trading transactions, and various other financial arrangements worldwide.

3. Depends on Financial Strength

The level depends on the other party’s financial stability, creditworthiness, and repayment capacity.

4. May Cause Payment Defaults

Counterparty failure can result in payment delays, missed obligations, contract breaches, or complete default, causing financial losses.

5. Manageable Through Risk Controls

It can be reduced through regular credit assessments, collateral, diversification, monitoring, and effective risk management practices.

How Does Counterparty Risk Work?

It usually follows these steps:

Step 1: Agreement

Two parties enter into a financial contract, establishing mutual obligations involving future payments, services, or asset exchanges together.

Step 2: Obligation

Each party agrees to make scheduled payments, deliver assets, or fulfill contractual commitments in accordance with the agreed terms and timelines.

Step 3: Financial Problems

One party experiences financial difficulties, reducing its ability to meet payment obligations or fulfill contractual obligations on time.

Step 4: Default

The financially troubled party fails to fulfill contractual obligations, missing payments or delivering agreed-upon assets as promised.

Step 5: Loss

The other party experiences financial losses because expected payments, assets, or contractual commitments are not successfully fulfilled as agreed.

Types of Counterparty Risk

Counterparty risk can arise in different forms depending on the type of financial transaction and the obligations involved. Below are the main types of counterparty risk:

1. Credit Risk

Credit risk occurs when a borrower doesn’t fulfill debt commitments or repay debts, which causes losses for lenders.

2. Settlement Risk

Settlement risk arises when one party has completed payment but the other party fails to deliver the agreed-upon financial asset.

3. Derivative Risk

Derivative risk arises when a counterparty fails to fulfill its obligations under derivative contracts, resulting in financial losses for participants.

4. Bank Counterparty Risk

Bank counterparty risk arises when a bank becomes insolvent and cannot meet its repayment obligations to depositors or investors.

Example of Counterparty Risk

The following example shows how counterparty risk can lead to financial losses when one party fails to fulfill its contractual obligations.

Imagine Company A enters into a contract with Company B to buy raw materials after three months. Before delivery, Company B faces financial problems and declares bankruptcy.

As a result:

- Company A does not receive the materials.

- It must find another supplier.

- The new supplier charges a higher price.

- Company A suffers additional costs.

This is a simple example of counterparty risk.

Advantages of Managing Counterparty Risk

Managing it offers several advantages.

1. Reduces Financial Losses

Evaluating counterparties before entering into agreements helps minimize default risk and protect businesses from significant financial losses over time.

2. Improves Investment Decisions

Assessing financial strength enables investors to select reliable companies with lower default risks and stronger long-term stability.

3. Increases Business Confidence

Partnering with trustworthy counterparties strengthens business relationships, enhances confidence, and encourages successful long-term commercial partnerships.

4. Protects Cash Flow

Timely payments from reliable counterparties improve cash flow, ensuring smooth operations and better financial planning for businesses.

5. Supports Financial Stability

Effective counterparty risk management reduces systemic risk, promotes stronger financial markets, and consistently maintains overall economic stability.

Disadvantages of Counterparty Risk

It also has some disadvantages.

1. Difficult to Predict

Unexpected financial problems can affect even strong counterparties, making future defaults challenging to identify and prevent early.

2. Requires Continuous Monitoring

Businesses must regularly evaluate counterparties’ financial health to identify emerging risks and mitigate potential future losses.

3. Can Cause Large Losses

A single counterparty default may cause substantial financial losses, significantly disrupting investments, contracts, and overall business profitability.

4. Increases Costs

Conducting risk assessments, obtaining insurance, and preparing legal agreements increase operational expenses for businesses and financial institutions.

5. Affects Business Operations

Counterparty defaults can delay payments, interrupt projects, and disrupt normal business operations, reducing overall organizational efficiency and performance.

How to Manage Counterparty Risk?

Businesses and investors can reduce it by following these practices:

1. Check Creditworthiness

Review financial statements, credit ratings, and payment history before entering agreements with any counterparty to reduce default risks.

2. Diversify

Spread business across multiple customers, suppliers, and financial institutions to significantly reduce dependence on any single counterparty.

3. Use Collateral

Request valuable collateral or security to recover potential losses if the counterparty fails to meet contractual obligations.

4. Set Exposure Limits

Limit financial exposure with each counterparty to minimize potential losses from a single default or business failure.

5. Monitor Regularly

Continuously monitor counterparties’ financial health and market conditions to identify risks and respond before problems worsen.

Applications of Counterparty Risk

Counterparty risk assessment is important in many areas.

1. Banking

Banks assess borrowers’ creditworthiness before approving loans to reduce default risks and protect lending portfolios from financial losses.

2. Investing

Investors evaluate companies’ financial strength before purchasing bonds or securities to minimize default risk and protect investment returns.

3. Insurance

Insurance companies review insurers’ and reinsurers’ financial stability to ensure that claims and contractual obligations are reliably fulfilled.

4. Trading

Traders monitor counterparty risk in stock, currency, and derivative transactions to effectively reduce settlement failures and financial exposure.

5. Business Contracts

Businesses assess suppliers’ and customers’ financial reliability before signing contracts to reduce payment defaults and operational disruptions.

Final Thoughts

Counterparty risk is the possibility that one party in financial transaction fails to meet its obligations. It affects banking, investing, insurance, and trading activities. Managing this risk through credit assessment, diversification, collateral, and regular monitoring helps reduce losses, protect investments, strengthen financial relationships, and support informed business and investment decisions.

Frequently Asked Questions (FAQs)

Q1. Can counterparty risk be eliminated?

Answer: No. It can only be reduced through proper risk management and regular monitoring.

Q2. Which financial products commonly involve counterparty risk?

Answer: Loans, corporate bonds, derivatives, insurance contracts, and OTC transactions.

Q3. Why is counterparty risk important?

It helps businesses and investors avoid losses and make safer financial decisions.

Q4. Who is exposed to counterparty risk?

Answer: Banks, investors, businesses, traders, insurers, and borrowers can all face counterparty risk.

Recommended Articles

We hope that this EDUCBA information on “Counterparty Risk” was beneficial to you. You can view EDUCBA’s recommended articles for more information.