What is a Zero-Coupon Bond?

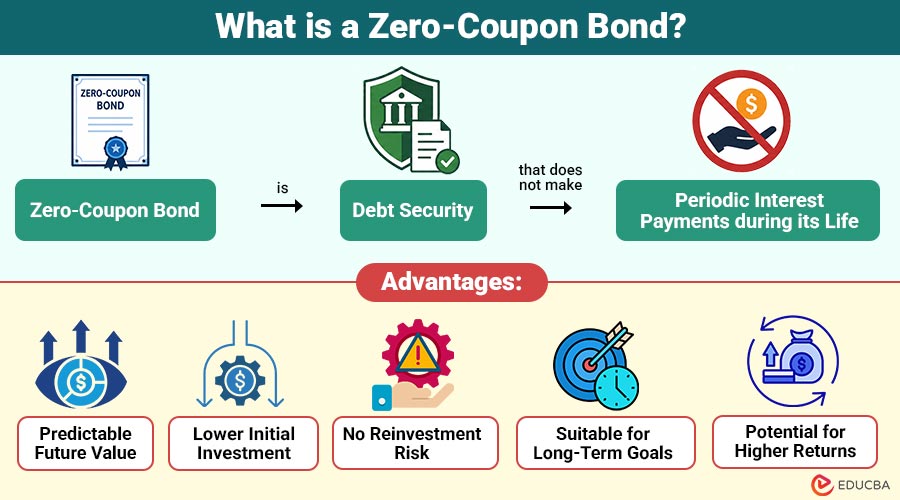

A zero-coupon bond is debt security that does not make periodic interest (coupon) payments during its life. Instead, the bond is sold at a price significantly lower than its face value and matures at par value. The investor earns a return from the difference between the purchase price and the bond’s face value at maturity.

For example, an investor purchases a zero-coupon bond for $6,000 with a face value of $10,000 and a maturity period of 10 years. At maturity, the investor receives $10,000. The $4,000 difference represents the investor’s earnings.

Table of Contents:

- Meaning

- Working

- Key Features

- Advantages

- Disadvantages

- Difference

- Real-World Examples

- Who Should Invest?

Key Takeaways:

- Zero-coupon bonds offer predictable returns through discounted purchases and maturity payments.

- Investors receive no periodic interest and earn profits solely at maturity.

- These bonds suit long-term financial goals requiring predetermined future amounts.

- Interest rate, inflation, credit, and tax risks require careful evaluation.

How Does a Zero-Coupon Bond Work?

It operates differently from conventional bonds.

Step 1: Bond Issuance

The issuer, such as a corporation or government entity, issues the bond at a discounted price.

Step 2: No Periodic Interest Payments

Unlike regular bonds, investors do not receive semiannual or annual interest payments.

Step 3: Value Appreciation

As the bond approaches maturity, its value gradually increases.

Step 4: Redemption at Maturity

On maturity date, the investor receives the bond’s full face value.

Example:

Suppose a company issues a zero-coupon bond with:

- Face value: $10,000

- Purchase price: $7,000

- Maturity: 8 years

The investor pays $7,000 initially and receives $10,000 after eight years, earning a total return of $3,000.

Key Features of Zero-Coupon Bond

The following features distinguish it from traditional bonds:

1. No Coupon Payments

During the investment period, zero-coupon bonds do not offer periodic interest payments.

2. Issued at a Discount

Investors can profit from these bonds because they are issued at a discount to face value.

3. Fixed Maturity Value

Investors receive the predetermined face value when the bond matures.

4. Long-Term Investment Instrument

Most zero-coupon bonds have medium- or long-term maturity periods for investors.

5. Predictable Returns

Predetermined maturity values enable investors to accurately estimate future investment returns.

6. Higher Price Sensitivity

Prices fluctuate significantly in response to changing interest rates.

Advantages of a Zero-Coupon Bond

It provides several advantages to investors.

1. Predictable Future Value

Investors knows exact amount they will receive when the investment matures successfully.

2. Lower Initial Investment

Issued at a discount, these securities require a lower upfront investment than many traditional bonds.

3. No Reinvestment Risk

Investors avoid reinvestment risk because no periodic interest payments are made.

4. Suitable for Long-Term Goals

They effectively support long-term financial goals like education, retirement, or home purchases.

5. Potential for Higher Returns

Holding them until maturity can generate attractive returns for investors over time.

Disadvantages of Zero-Coupon Bond

Despite their advantages, they also have certain disadvantages.

1. Interest Rate Risk

The price can fluctuate significantly due to its high sensitivity to changes in interest rates.

2. No Regular Income

Investors seeking consistent periodic income may find these investments unsuitable for their financial needs.

3. Credit Risk

Corporate issues may default if their issuers experience financial difficulties or file for bankruptcy unexpectedly.

4. Inflation Risk

Inflation can erode future purchasing power, significantly reducing the real value of maturity proceeds.

5. Phantom Income Tax

Investors may owe taxes annually on accrued interest even if they receive no cash payments.

Difference Between Zero-Coupon Bond and Coupon Bond

The table below highlights the key differences between the two bonds:

| Basis | Zero-Coupon Bond | Coupon Bond |

| Interest Payments | No periodic interest | Regular interest payments |

| Issue Price | Issued at a discount | Usually issued near face value |

| Cash Flow | Single payment at maturity | Periodic coupons plus principal |

| Reinvestment Risk | Minimal | Present |

| Price Volatility | Higher | Lower |

| Income Generation | No regular income | Regular income stream |

Real-World Examples

The following examples illustrate how zero-coupon bonds are commonly used for investment and financial planning purposes:

1. Treasury STRIPS

Governments often create zero-coupon securities by separating coupon payments from those of Treasury bonds. These are known as Treasury STRIPS and are popular among conservative investors.

2. Education Savings

Parents may purchase zero-coupon bonds maturing when their child reaches college age. The maturity proceeds can help fund tuition expenses.

3. Retirement Planning

Zero-coupon bonds that mature at retirement can be purchased by an investor who plans to retire in 20 years, guaranteeing a preset retirement corpus.

Who Should Invest?

Zero-coupon bonds are generally suitable for:

1. Long-Term Investors

Investors with long investment horizons can benefit from predictable returns and compounding growth.

2. Retirement planners

Individuals planning retirement can use these bonds to accumulate a fixed future corpus.

3. Parents Saving for Education Expenses

Parents can match bond maturities with future educational funding requirements.

4. Risk-Averse Investors

Conservative investors may prefer government-issued zero-coupon bonds because they offer predictable maturity values.

5. Goal-Oriented Investors

Investors saving for specific goals, such as buying a home, can benefit from these bonds.

Final Thoughts

Zero-coupon bonds are fixed-income securities that pay a predetermined lump sum at maturity rather than periodic interest payments. Their predictable returns and discounted purchase price make them suitable for long-term financial goals. However, investors should evaluate interest rate, inflation, credit, and tax risks before investing as part of a diversified portfolio.

Frequently Asked Questions (FAQs)

Q1. How do investors make money from zero-coupon bonds?

Answer: Investors profit from difference between the discounted purchase price and the bond’s face value received at maturity.

Q2. Can zero-coupon bonds be sold before maturity?

Answer: Yes. Investors can sell them in secondary market before maturity, although the selling price may differ from the original purchase price.

Q3. Are zero-coupon bonds suitable for retirees?

Answer: They may be suitable for retirees seeking future lump-sum payments but may not be ideal for those needing regular income.

Recommended Articles

We hope that this EDUCBA information on “Zero-Coupon Bond” was beneficial to you. You can view EDUCBA’s recommended articles for more information.