What is Defeasance?

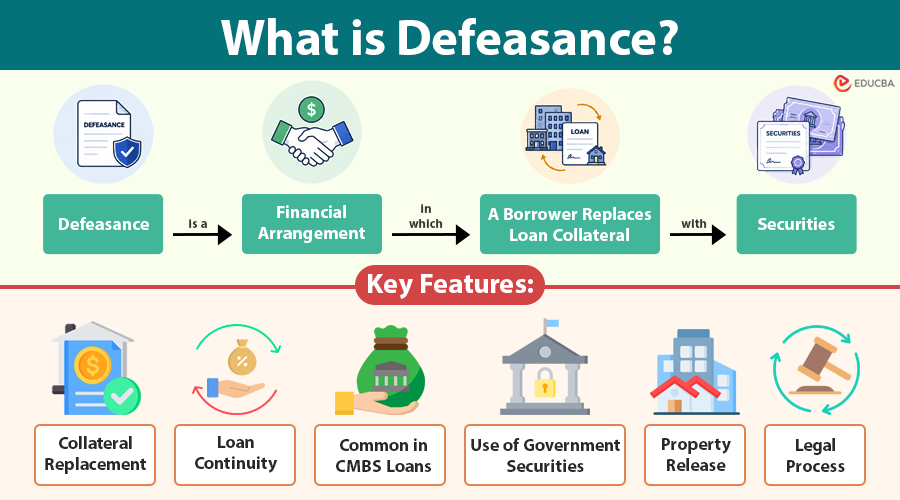

Defeasance is a financial arrangement in which a borrower replaces loan collateral with securities. This allows the original collateral to be released while loan payments continue as scheduled. It is commonly used in the commercial real estate, particularly for Commercial Mortgage-Backed Securities (CMBS) loans, when borrowers want to sell or refinance a property before the loan matures.

For example, a company selling an office building before its CMBS loan matures may replace the property collateral with treasury securities, allowing the sale to proceed while preserving lender cash flows.

Table of Contents:

Key Takeaways:

- Defeasance replaces loan collateral with government securities while preserving scheduled debt payments.

- It enables property sales or refinancing without terminating existing commercial loan agreements.

- Defeasance primarily applies to CMBS loans and protects lenders’ expected cash flows.

- Although beneficial, defeasance involves complex procedures, strict requirements, and significant transaction costs.

Why is Defeasance Important?

Defeasance plays an important role in commercial lending and real estate transactions because it offers flexibility while protecting lenders’ interests.

Some important reasons include:

1. Enables Early Property Sale

Borrowers can sell properties before loan maturity without violating loan agreements.

2. Preserves Lender Cash Flows

Lenders and investors continue to receive the expected payments throughout the original loan term.

3. Avoids Prepayment Restrictions

Helps borrowers bypass certain prepayment penalties and contractual limitations

4. Facilitates Refinancing Opportunities

Property owners can refinance assets more easily while maintaining existing loan obligations.

5. Supports Market Liquidity

Promotes smoother transactions and greater liquidity within commercial real estate markets.

6. Protects Securitized Structures

It minimizes disruptions to commercial mortgage-backed securities and associated investment portfolios.

How Does Defeasance Work?

The defeasance process generally involves the following steps:

Step 1: Review Loan Documents

The borrower examines the loan agreement to determine whether defeasance is permitted and to understand the specific requirements.

Step 2: Hire Professionals

Borrowers usually engage legal advisors, accountants, defeasance consultants, and securities brokers to manage the transaction.

Step 3: Purchase Replacement Securities

The borrower buys a portfolio of government securities, typically U.S. Treasury or agency bonds, that generate cash flows matching the remaining loan payments.

Step 4: Substitute Collateral

The purchased securities replace the original property as collateral for the loan.

Step 5: Release of Property

Once the lender approves the substitution, the lender releases its lien on the property, enabling the borrower to sell or refinance it.

Step 6: Loan Payments Continue

The cash generated by the replacement securities continues to satisfy the remaining loan obligations until maturity.

Key Features of Defeasance

The following are the major features of defeasance:

1. Collateral Replacement

Original collateral is replaced with approved securities that generate cash flows that match loan obligations.

2. Loan Continuity

The existing loan remains active, and scheduled payments continue until the original maturity date.

3. Common in CMBS Loans

Primarily used in commercial mortgage-backed securities loans to facilitate property transactions.

4. Use of Government Securities

Replacement collateral generally consists of low-risk government securities, ensuring reliable future payment streams.

5. Property Release

After collateral substitution, borrowers can freely sell, transfer, or refinance the encumbered property.

6. Legal Process

Requires extensive legal documentation, regulatory compliance, and coordination among multiple involved parties.

Types of Defeasance

The following are the main types of defeasance:

1. Commercial Real Estate Defeasance

This is the most common type and occurs when borrowers substitute collateral in commercial property loans, particularly CMBS loans.

2. Bond Defeasance

Companies or governments may set aside sufficient funds or securities to repay outstanding bonds. Once adequate assets are reserved, the debt is considered economically defeased.

3. Legal Defeasance

Legal defeasance occurs when debt is legally removed from the borrower’s balance sheet because sufficient assets have been irrevocably placed in trust for repayment.

4. In-Substance Defeasance

In this form, debt remains legally outstanding, but accounting standards may permit removal of the liability from financial statements because repayment funds have been set aside.

Advantages of Defeasance

It offers several advantages to borrowers, lenders, and investors.

1. For Borrowers

- Provides flexibility to sell or refinance properties.

- May be less expensive than certain prepayment penalties.

- Allows access to better financing opportunities.

- Preserves business expansion plans.

2. For Lenders and Investors

- Maintains scheduled loan cash flows.

- Minimizes reinvestment risk.

- Preserves the stability of securitized investments.

- Ensures continued debt servicing.

3. Overall Benefits

- Increases market liquidity.

- Facilitates property transactions.

- Maintains contractual obligations.

- Offers an alternative to loan prepayment.

Challenges of Defeasance

Despite its benefits, defeasance also presents several challenges.

1. High Transaction Costs

The process often involves legal fees, consulting expenses, accounting fees, and securities acquisition costs.

2. Complex Procedures

Defeasance transactions require coordination among multiple parties, making the process complicated and time-consuming.

3. Interest Rate Risk

The cost of purchasing replacement securities may increase when market interest rates decline.

4. Strict Loan Requirements

Not all loans permit defeasance, and lenders may impose detailed conditions.

5. Timing Constraints

Loan agreements often specify exact windows during which defeasance can occur.

Difference Between Defeasance and Prepayment

The table below highlights the key differences between defeasance and prepayment:

| Basis | Defeasance | Prepayment |

| Meaning | Replaces collateral with securities | Pays off the loan early |

| Loan Status | Loan remains active | Loan terminates |

| Collateral | Substitute assets are provided | No substitute collateral required |

| Cash Flow to Lender | Continues unchanged | Stops after payoff |

| Common Usage | CMBS loans | Traditional loans |

| Complexity | High | Relatively low |

Real-World Example

The example below illustrates how defeasance works in practice within a commercial real estate transaction.

A real estate investment firm owns a shopping center financed through a 10-year CMBS loan. After six years, the firm receives an attractive purchase offer for the property.

The loan agreement prohibits early repayment but allows defeasance. To complete the sale, the firm purchases Treasury securities that generate sufficient cash flows to cover the remaining four years of loan payments. These securities replace the shopping center as collateral.

After the substitution is approved, the lender releases its claim on the property, thereby enabling the sale while investors continue to receive scheduled payments.

Final Thoughts

Defeasance is an important financial mechanism that allows borrowers to unlock assets tied to long-term loans while protecting lenders and investors from disruptions in expected cash flows. Although the process can be complex and costly, it offers substantial flexibility, particularly in commercial real estate financing. Careful planning and professional guidance can help borrowers determine whether defeasance is the most suitable option for their financial objectives.

Frequently Asked Questions (FAQs)

Q1. Is defeasance available for all types of loans?

Answer: No. Defeasance is primarily associated with commercial mortgage-backed securities (CMBS) loans. Traditional residential mortgages and many conventional loans generally do not permit defeasance.

Q2. Who typically uses defeasance?

Answer: Commercial property owners, real estate investment firms, and businesses with long-term secured loans commonly use defeasance when they wish to sell or refinance properties before the loan matures.

Q3. How long does a defeasance transaction usually take?

Answer: The process typically takes between 30 and 60 days, depending on the loan’s complexity, documentation requirements, and coordination among the parties involved.

Q4. Can a borrower perform defeasance without professional assistance?

Answer: Although technically possible, defeasance transactions are highly complex. Most borrowers hire attorneys, accountants, defeasance consultants, and securities specialists to ensure compliance and the smooth execution of the transaction.

Recommended Articles

We hope that this EDUCBA information on “Defeasance” was beneficial to you. You can view EDUCBA’s recommended articles for more information.