What is Mezzanine Debt?

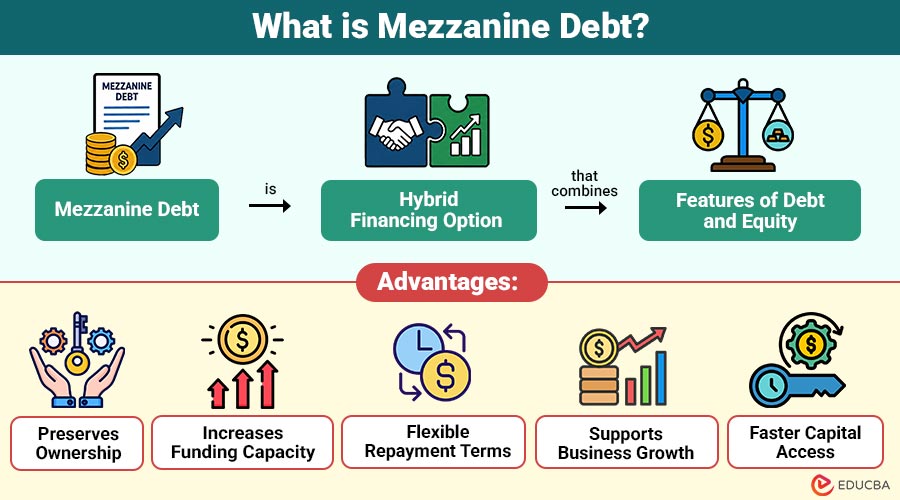

Mezzanine debt is hybrid financing option that combines features of debt and equity. It ranks below senior debt but above equity in a company’s capital structure and is commonly used to fund business expansion, acquisitions, and growth initiatives. In return for higher risk, lenders typically receive higher interest rates and may gain equity participation rights, such as warrants or conversion options.

Table of Contents:

- Meaning

- Working

- Key Features

- Types

- Advantages

- Disadvantages

- Real-World Examples

- Common Uses

- Who Provides Mezzanine Debt?

Key Takeaways:

- Mezzanine debt combines debt and equity features, providing flexible capital for business growth initiatives.

- It ranks below senior debt but above equity, increasing lender risk and returns.

- Lenders often receive warrants or conversion rights, enabling them to participate in future growth.

- Businesses use mezzanine financing effectively for acquisitions, expansions, buyouts, and recapitalizations.

How Does Mezzanine Debt Work?

Mezzanine debt is a subordinated to senior debt, meaning senior lenders are repaid first if the company experiences financial difficulties or enters bankruptcy.

The financing arrangement typically includes:

- Fixed or variable interest payments

- Longer repayment periods

- Flexible repayment structures

- Warrants or equity conversion rights

- Subordinated repayment priority

The lender receives periodic interest income and may also benefit from future company growth through equity participation.

Example:

A company seeks $100 million for expansion.

| Source of Funding | Amount |

| Senior Loan | $70 Million |

| Mezzanine Debt | $20 Million |

| Equity Investment | $10 Million |

In this structure, mezzanine debt helps bridge the financing gap while minimizing equity dilution.

Key Features of Mezzanine Debt

The following features highlight how mezzanine debt combines financing flexibility, higher returns for lenders, and growth-focused capital for businesses.

1. Subordinated Position

It ranks below senior loans but above equity holders, determining repayment priority in the event of liquidation or bankruptcy.

2. Higher Interest Rates

Lenders charge higher interest rates because mezzanine financing carries greater risk than traditional senior debt loans.

3. Equity Participation

Many agreements include warrants or conversion rights, allowing lenders to share in future company growth.

4. Flexible Terms

Repayment structures are typically more flexible, helping businesses manage cash flow and financial obligations effectively.

5. Long-Term Financing

Generally has maturity periods between five and ten years, supporting long-term business growth.

6. Limited Collateral Requirements

Financing often depends on a company’s cash flows and performance rather than on significant physical asset collateral.

Types of Mezzanine Debt

Mezzanine debt is available in several types, each offering a different balance of debt repayment obligations and potential equity participation.

1. Subordinated Debt

Traditional unsecured financing that ranks below senior debt in repayment priority and offers lenders higher potential returns.

2. Convertible Debt

Mezzanine debt that can convert into company equity under predetermined conditions, providing lenders potential ownership benefits.

3. Debt with Warrants

Financing that includes warrants, granting lenders the right to purchase company shares at predetermined prices later.

4. Preferred Equity Mezzanine Financing

A hybrid financing structure combining regular payments with certain ownership rights and equity-related investment benefits.

Advantages of Mezzanine Debt

The following advantages makes it an attractive financing option for companies seeking growth capital while maintaining ownership control.

1. Preserves Ownership

Provides growth capital while minimizing immediate dilution of existing shareholders’ and founders’ equity.

2. Increases Funding Capacity

Enables businesses to raise additional capital beyond traditional senior lending limits.

3. Flexible Repayment Terms

Offers customized repayment structures that better align with business cash flow needs.

4. Supports Business Growth

Helps finance acquisitions, expansions, and strategic initiatives without major sacrifices in ownership.

5. Faster Capital Access

Often provides faster funding approvals than conventional bank financing processes.

Disadvantages of Mezzanine Debt

Despite its flexibility and growth benefits, mezzanine debt also presents several disadvantages and costs that businesses should carefully evaluate.

1. Higher Financing Costs

Carries significantly higher interest rates than traditional bank loans, increasing overall borrowing costs.

2. Potential Ownership Dilution

Conversion rights or warrants may reduce existing shareholders’ ownership percentages over time.

3. Cash Flow Burden

Regular interest payments can strain company cash flows during challenging financial periods.

4. Increased Financial Risk

Additional leverage raises debt obligations and may impact future borrowing capacity.

5. Complex Agreements

Financing structures often involve detailed terms, negotiations, and higher legal compliance requirements.

Real-World Examples

The following examples illustrate how businesses and investors use mezzanine debt to finance acquisitions, expansion projects, and large-scale developments.

1. Leveraged Buyout

A private equity firm uses stock, mezzanine financing, and senior loans to purchase a business.

2. Business Expansion

A retail chain obtains mezzanine financing to open new stores and expand operations into additional markets.

3. Real Estate Development

A property developer uses mezzanine debt to supplement construction financing for a large commercial project.

Common Uses of Mezzanine Debt

Organizations utilize mezzanine debt for:

1. Business Expansion

Companies use mezzanine financing to fund expansion projects, increase production capacity, and enter new market segments.

2. Mergers and Acquisitions

Businesses obtain mezzanine capital to finance acquisitions, bridge funding gaps, and support strategic growth objectives.

3. Leveraged Buyouts

Investors utilize mezzanine debt to supplement acquisition financing, reducing equity requirements while maximizing potential returns.

4. Management Buyouts

Management teams secure mezzanine financing to acquire ownership stakes without contributing substantial personal capital.

5. Real Estate Projects

Developers use mezzanine financing to fund construction, property acquisitions, and large-scale real estate developments.

6. Corporate Recapitalizations

Companies employ mezzanine debt to restructure capital, improve liquidity, and optimize financial balance sheets.

Who Provides Mezzanine Debt?

Several financial institutions and investors specialize in mezzanine financing, including:

1. Mezzanine Investment Funds

Dedicated investment funds provide mezzanine capital to businesses seeking flexible financing for expansion and acquisitions.

2. Private Equity Firms

Private equity firms offer mezzanine financing to support portfolio companies, buyouts, and strategic growth initiatives.

3. Asset Management Companies

Asset managers allocate capital to mezzanine debt investments to consistently generate attractive risk-adjusted returns.

4. Insurance Companies

Insurance companies invest in mezzanine financing opportunities to diversify portfolios and earn stable income.

5. Business Development Companies

Business development companies provide mezzanine loans to middle-market businesses requiring growth capital and acquisition financing.

6. Specialized Credit Funds

Credit-focused funds offer customized mezzanine financing solutions for companies with unique funding requirements.

Final Thoughts

Mezzanine debt is a flexible financing solution that combines features of debt and equity, helping businesses fund growth, acquisitions, and expansion. While it involves higher costs than traditional loans, it minimizes ownership dilution and increases financing capacity. When used strategically, mezzanine debt can support long-term growth, value creation, and business success.

Frequently Asked Questions (FAQs)

Q1. Is mezzanine debt secured?

Answer: It is often unsecured or only lightly secured, making it riskier than senior debt.

Q2. What interest rates are common for mezzanine debt?

Answer: Rates are typically higher than traditional bank loans due to increased risk and may include additional equity-related returns.

Q3. Can mezzanine debt convert into equity?

Answer: Yes. Many agreements include conversion features or warrants that allow lenders to acquire ownership interests.

Recommended Articles

We hope that this EDUCBA information on “Mezzanine Debt” was beneficial to you. You can view EDUCBA’s recommended articles for more information.