What is Unitranche Debt?

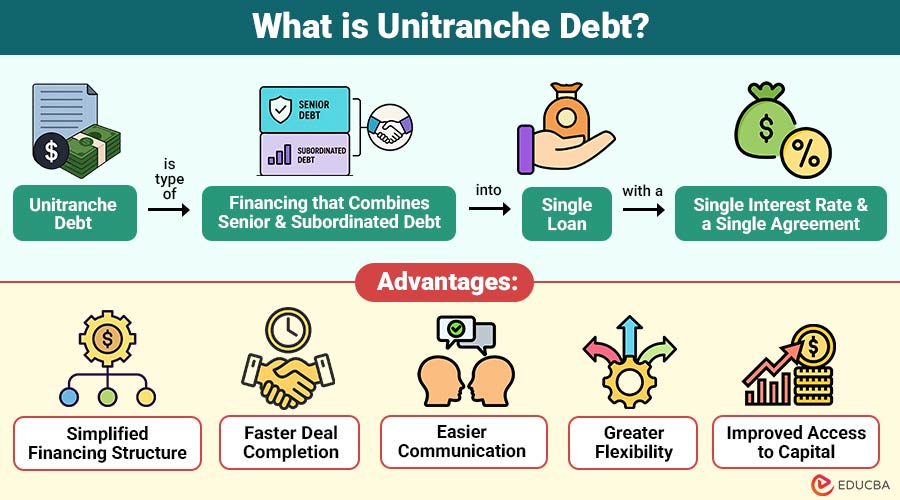

Unitranche debt is type of financing that combines senior and subordinated debt into single loan with a single interest rate and a single agreement.

The word “unitranche” comes from the following:

- “Uni” meaning one

- “Tranche” means layer or portion

Traditionally, companies seeking financing often borrow through multiple layers of debt.

Example:

- Senior loan from a bank

- Mezzanine loan from an investment firm

Each loan has different lenders, interest rates, repayment terms, and legal agreements. With unitranche debt, these multiple layers are consolidated into a single financing package, creating a simpler borrowing structure.

Table of Contents:

- Meaning

- Working

- Key Features

- Why do Companies Use Unitranche Debt?

- Advantages

- Disadvantages

- Who Provides Unitranche Debt?

- Common Uses

- Difference

- Real-World Example

- The Growing Popularity of Unitranche Debt

Key Takeaways:

- Unitranche debt combines senior and subordinated financing into one simplified loan facility structure.

- Borrowers benefit from faster funding, streamlined administration, and greater certainty in the execution of financing.

- Private credit lenders typically provide flexible terms tailored to business growth objectives.

- Higher borrowing costs may arise, but simplicity and flexibility often outweigh the costs.

How Does Unitranche Debt Work?

Instead of arranging separate senior and mezzanine loans, a company receives one combined loan from a group of lenders.

Example:

Traditional Structure:

- Senior Debt: ₹70 crore

- Mezzanine Debt: ₹30 crore

Unitranche Structure:

- Single Unitranche Loan: ₹100 crore

The borrower deals with:

- One lending group

- One loan agreement

- One repayment schedule

- One interest payment

Behind the scenes, lenders may divide the risk among themselves through private agreements, but the borrower experiences a much simpler financing process.

Key Features of Unitranche Debt

Below are the key features that make unitranche debt a popular financing option for businesses seeking simplified and flexible funding solutions.

1. Single Loan Facility

Combines multiple debt layers into one loan, simplifying management, reporting, and repayment processes.

2. One Interest Rate

Uses a blended interest rate across the loan, making budgeting and planning easier.

3. Faster Execution

Fewer lenders and agreements enable quicker approvals, funding, and transaction completion timelines.

4. Flexible Terms

Private lenders often provide customized repayment schedules, covenants, and financing structures.

5. Larger Financing Packages

Single lenders can provide substantial capital, reducing the need to coordinate with multiple financiers.

Why Do Companies Use Unitranche Debt?

Companies choose unitranche financing for several reasons.

1. Simplicity

Managing a single loan facility significantly reduces administrative work, documentation requirements, and overall financing complexity.

2. Speed

Unitranche lenders provide quicker approvals and funding, helping businesses seize opportunities without unnecessary delays.

3. Certainty of Funding

Single-source financing increases confidence that the required capital will be available when needed most.

4. Flexible Structures

Private lenders customize financing terms to match business goals, cash flows, and growth requirements.

Advantages of Unitranche Debt

The following advantages make unitranche debt an attractive financing option for many businesses and private equity-backed transactions.

1. Simplified Financing Structure

A single agreement replaces multiple loan contracts, reducing paperwork, complexity, and administrative responsibilities.

2. Faster Deal Completion

Fewer parties involved enable quicker approvals, negotiations, and funding for business transactions.

3. Easier Communication

Working with a single primary lender streamlines communication, coordination, and financing-related decision-making.

4. Greater Flexibility

Private lenders often customize terms to accommodate unique business needs and circumstances.

5. Improved Access to Capital

Businesses may secure funding more easily when traditional financing options are unavailable.

Disadvantages of Unitranche Debt

While unitranche financing offers many benefits, it also has disadvantages.

1. Higher Interest Costs

Combined risk levels often result in higher interest rates than traditional senior bank loans.

2. Potentially Stricter Covenants

Lenders may impose performance requirements and restrictions, with penalties for non-compliance issues.

3. Limited Availability

Lenders prefer businesses with stable cash flows, strong management, and proven operating models.

4. Reduced Competition Among Lenders

Single-source financing limits lender competition, potentially reducing borrowers’ negotiating power and flexibility.

Who Provides Unitranche Debt?

Unitranche loans are commonly offered by:

1. Private Credit Funds

Private credit funds provide customized financing solutions directly to businesses outside traditional banking channels.

2. Direct Lending Funds

Direct lending funds offer loans directly to companies, simplifying borrowing and funding processes.

3. Asset Management Firms

Asset management firms invest capital through debt financing opportunities to generate attractive returns.

4. Alternative Investment Funds

Alternative investment funds provide flexible financing structures tailored to business growth requirements.

5. Specialized Financing Companies

Specialized financing companies focus on delivering customized lending solutions for specific industries and needs.

Common Uses of Unitranche Debt

Unitranche debt is commonly used in a variety of corporate financing transactions where speed, flexibility, and simplified funding structures are important.

1. Business Acquisitions

Companies use unitranche financing to acquire businesses quickly through streamlined funding and simplified processes.

2. Leveraged Buyouts

Private equity firms utilize unitranche debt to simplify financing structures during company acquisition transactions.

3. Growth Capital

Businesses obtain unitranche financing to support expansion, innovation, market growth, and technology investments.

4. Recapitalizations

Companies refinance existing debt with unitranche facilities to simplify and optimize capital structures.

Difference Between Unitranche Debt and Traditional Debt

The table below highlights the key differences between unitranche debt and traditional debt financing structures.

| Feature | Unitranche Debt | Traditional Debt |

| Loan Structure | Single facility | Multiple debt layers |

| Number of Agreements | One | Several |

| Approval Speed | Faster | Slower |

| Administration | Simpler | More complex |

| Interest Rate | Blended rate | Multiple rates |

| Flexibility | Higher | Lower |

| Cost | Usually higher | Often lower |

Real-World Example

The example below demonstrates how a unitranche financing structure can simplify a business acquisition.

Imagine a manufacturing company wants to purchase a smaller competitor for ₹200 crore.

Traditional Approach:

The company might arrange the following:

- ₹140 crore senior loan from a bank

- ₹60 crore mezzanine financing from another lender

This process may involve lengthy negotiations and multiple legal documents.

Unitranche Approach:

A direct lending fund provides a single ₹200 crore unitranche loan.

Benefits include:

- Faster transaction completion

- Simplified documentation

- One lender relationship

- Greater certainty of financing

The acquisition can proceed more efficiently, helping the company capitalize on the opportunity.

The Growing Popularity of Unitranche Debt

Over the past decade, unitranche debt has grown significantly worldwide.

Several factors have contributed to this growth:

- Expansion of private credit markets

- Increased demand for flexible financing

- Faster acquisition activity

- Desire for simplified capital structures

Private equity firms, middle-market businesses, and growing companies increasingly view unitranche financing as an attractive alternative to traditional lending arrangements.

As private credit continues to expand globally, unitranche debt is expected to remain an important financing tool for businesses seeking efficient access to capital.

Final Thoughts

Unitranche debt offers a streamlined financing solution by consolidating multiple layers of debt into a single facility, reducing complexity and accelerating transactions. Its flexibility, faster execution, and simplified management make it particularly attractive for acquisitions, growth initiatives, and buyouts, despite potentially higher borrowing costs than traditional financing options.

Frequently Asked Questions (FAQs)

Q1. Is unitranche debt secured or unsecured?

Answer: Most unitranche loans are secured debt, meaning they are backed by the borrower’s assets. If the borrower defaults, lenders may have the right to recover funds through those assets.

Q2. Is unitranche debt more expensive than traditional bank loans?

Answer: Generally, yes. Unitranche debt often carries a higher interest rate than senior bank loans because lenders assume greater risk. However, borrowers benefit from faster execution and simplified financing.

Q3. Can startups obtain unitranche debt?

Answer: Some startups may qualify, but lenders usually prefer businesses with established operations, consistent cash flow, strong management teams, and predictable revenue streams.

Q4. How long does a unitranche loan typically last?

Answer: The maturity period varies, generally ranging from 5 to 7 years, depending on lender and financing arrangement.

Recommended Articles

We hope that this EDUCBA information on “Unitranche Debt” was beneficial to you. You can view EDUCBA’s recommended articles for more information.