What is Nonaccrual Loan?

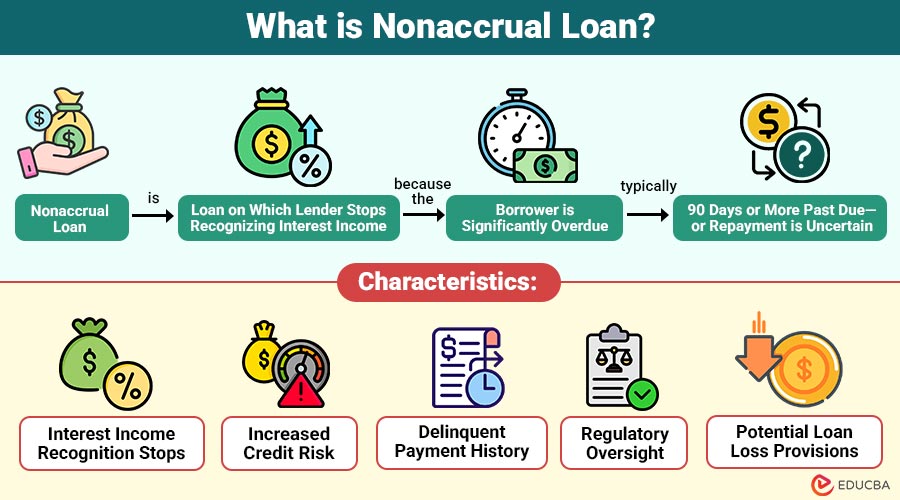

A nonaccrual loan is a loan on which the lender stops recognizing interest income because the borrower is significantly overdue—typically 90 days or more past due—or repayment is uncertain. Interest is no longer recorded as revenue until the borrower resumes regular payments and the loan returns to good standing.

For example, if a borrower misses loan payments for several months and repayment appears doubtful, the lender may classify the loan as nonaccrual and stop accruing interest income.

Table of Contents:

- Meaning

- Working

- Characteristics

- Causes

- Advantages

- Challenges

- How are Nonaccrual Loans Managed?

- Examples

Key Takeaways:

- A nonaccrual loan is a loan for which interest income is no longer recognized because repayment is uncertain.

- Loans typically enter nonaccrual status after significant payment delinquency or evidence of collection risk.

- Nonaccrual classification promotes accurate financial reporting and regulatory compliance.

- These loans reduce lender profitability and may require additional loss reserves.

How Does a Nonaccrual Loan Work?

Under normal circumstances, lenders accrue interest income over time, even if the borrower has not yet made the payment. However, when a loan becomes highly delinquent and repayment appears doubtful, accounting and regulatory rules require the lender to stop accruing interest.

The process generally follows these steps:

Step 1: Loan Origination

Bank or financial institution issues a loan to a borrower.

Step 2: Payment Delinquency

The borrower begins missing scheduled principal or interest payments.

Step 3: Loan Classification

After a specified period—often around 90 days past due—the lender reviews the loan’s collectability.

Step 4: Nonaccrual Status

The lender stops recognizing interest income and may reverse previously accrued but unpaid interest.

Step 5: Recovery or Resolution

The loan may be restructured, collected, refinanced, returned to accrual status, or written off if recovery is unlikely.

Characteristics of a Nonaccrual Loan

The following characteristics help identify a nonaccrual loan and highlight the associated risks and reporting requirements.

1. Interest Income Recognition Stops

Lenders stop recognizing interest revenue until borrowers resume payments or make actual repayments.

2. Increased Credit Risk

Nonaccrual status signals elevated default risk and greater potential financial losses for lenders.

3. Delinquent Payment History

Borrowers typically miss multiple scheduled payments before loans are classified as nonaccrual.

4. Regulatory Oversight

Financial institutions must comply with regulatory standards when classifying and reporting nonaccrual loans.

5. Potential Loan Loss Provisions

Banks often increase reserve allocations to cover anticipated losses from troubled loans.

Causes of Nonaccrual Loans

Several factors can cause a loan to enter nonaccrual status.

1. Borrower Financial Difficulties

Loss of income, reduced business revenue, or cash flow shortages can consistently prevent timely loan repayments.

2. Economic Downturns

Recessions, inflation, and industry slowdowns often weaken borrowers’ finances, increasing the number of missed payments and defaults.

3. Business Failure

Operational challenges, declining profitability, or business closures can make debt repayment obligations difficult.

4. Unemployment

Job loss reduces household income, limiting borrowers’ ability to meet regular loan payment commitments.

5. Poor Credit Management

Excessive debt, overspending, and poor financial planning can lead to long-term repayment difficulties for borrowers.

6. Unexpected Events

Medical emergencies, natural disasters, or legal issues may suddenly disrupt financial stability and repayments.

Advantages of Nonaccrual Loans

Although nonaccrual status is generally unfavorable, it offers certain advantages from accounting and risk-management perspectives.

1. Accurate Financial Reporting

Stopping interest accrual prevents reporting income that may never be collected from borrowers.

2. Improved Risk Assessment

Helps lenders identify troubled loans and evaluate credit risk more accurately and effectively.

3. Regulatory Compliance

Ensures that questionable loans are classified in accordance with regulatory rules and accounting standards.

4. Better Portfolio Monitoring

Highlights problematic loans that require closer monitoring, corrective actions, and prompt recovery efforts.

5. Enhanced Transparency

Provides investors and regulators with clearer insights into the institution’s financial health and performance.

Challenges Associated with Nonaccrual Loans

Managing nonaccrual loans presents several challenges for lenders, as repayment uncertainty, regulatory obligations, and economic conditions can complicate recovery efforts.

1. Recovery Uncertainty

Determining the likelihood and timing of loan recovery remains difficult for financial institutions.

2. Valuation of Collateral

Collateral values may decline over time, reducing protection against potential loan losses.

3. Regulatory Requirements

Institutions must comply with strict reporting, classification, and reserve requirement standards.

4. Resource-Intensive Management

Collection activities, loan restructuring, and legal actions often require significant resources and costs.

5. Economic Volatility

Changing economic conditions can weaken borrower repayment capacity and reduce recovery prospects.

How are Nonaccrual Loans Managed?

Financial institutions use several strategies to manage nonaccrual loans effectively.

1. Loan Restructuring

Lenders modify repayment schedules, interest rates, or terms to help borrowers regain affordability.

2. Enhanced Monitoring

Financial institutions regularly track borrower performance, cash flows, and repayment behavior.

3. Collateral Evaluation

Banks assess collateral value to estimate recovery amounts if the borrower defaults permanently.

4. Collection Efforts

Dedicated recovery teams contact borrowers and pursue overdue payments through various methods.

5. Charge-Offs

Loans may be written off when recovery becomes unlikely despite collection attempts.

6. Return to Accrual Status

Loans regain accrual status after borrowers demonstrate sustained repayment ability and financial stability.

Examples of Nonaccrual Loans

The following examples illustrate situations in which lenders may classify loans as nonaccrual due to uncertainty regarding repayment.

1. Commercial Loan

A manufacturing company borrows $500,000 from a bank. Due to declining market demand, the company stopped making payments for several months. After determining that the collection is uncertain, the bank classifies the loan as nonaccrual and stops recording interest income.

2. Mortgage Loan

A homeowner loses employment and misses mortgage payments for over 90 days. The lender places the mortgage in nonaccrual status until payments resume or the loan is restructured.

3. Business Expansion Loan

A restaurant chain obtains financing to open new locations. Unexpected economic conditions reduce revenue, making loan payments difficult. The lender moves the loan to nonaccrual status due to repayment concerns.

Final Thoughts

A nonaccrual loan is an important indicator of credit risk and repayment uncertainty within a lending portfolio. While it negatively affects lender profitability, it ensures accurate financial reporting and regulatory compliance. Effective monitoring, timely intervention, and borrower recovery efforts can improve loan performance and reduce potential financial losses.

Frequently Asked Questions (FAQs)

Q1. Can a nonaccrual loan return to normal status?

Answer: Yes. If the borrower resumes payments and demonstrates the ability to repay, the lender may restore the loan to accrual status.

Q2. Are nonaccrual loans the same as nonperforming loans?

Answer: They are closely related but not always identical. Most nonaccrual loans are nonperforming, though classification standards may vary by institution and jurisdiction.

Q3. How do nonaccrual loans affect borrowers?

Answer: Borrowers may face credit score damage, collection actions, loan restructuring, or reduced access to future credit.

Recommended Articles

We hope that this EDUCBA information on “Nonaccrual Loan” was beneficial to you. You can view EDUCBA’s recommended articles for more information.