What is Cash Pooling?

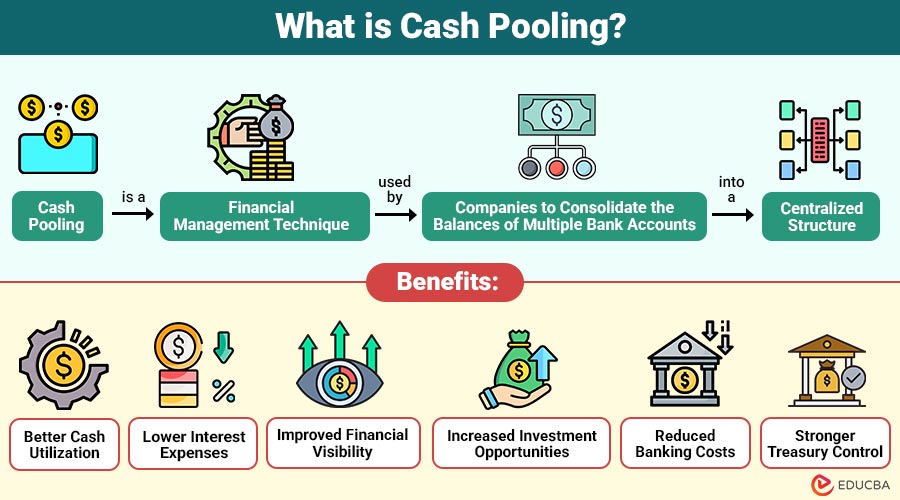

Cash pooling is a financial management technique used by companies to consolidate the balances of multiple bank accounts into a centralized structure. It helps businesses optimize liquidity, reduce financing costs, and improve overall cash management efficiency.

Large organizations with multiple subsidiaries, branches, or departments often maintain separate bank accounts. Some accounts may have excess cash, while others may face shortages. Cash pooling allows the company to combine these balances so surplus funds can offset deficits within the group.

For example, if one subsidiary has excess cash of $100,000 and another has a shortfall of $60,000, the pooled structure allows the surplus to cover the deficit instead of borrowing externally.

Table of Contents:

Key Takeaways:

- Cash pooling centralizes organizational funds, improving liquidity management, treasury control, and operational financial efficiency.

- Organizations reduce borrowing costs by using surplus internal cash rather than external financing.

- Physical and notional pooling structures help optimize interest earnings and overall cash utilization effectively.

- Successful cash pooling requires careful management of legal, tax, banking, and operational compliance risks.

Objectives of Cash Pooling

Organizations implement cash pooling to achieve several treasury and liquidity management goals.

1. Improve Liquidity Management

Cash pooling centralizes funds monitoring, helping businesses efficiently manage liquidity across multiple accounts and subsidiaries.

2. Reduce Borrowing Costs

Organizations use surplus internal funds instead of external loans, reducing borrowing costs and interest payments.

3. Maximize Interest Income

Combining account balances increases opportunities to earn higher interest income on surplus organizational cash reserves.

4. Enhance Operational Efficiency

Centralized treasury management simplifies financial operations, improves coordination, and supports accurate organizational cash planning.

5. Optimize Working Capital

Enables efficient allocation of funds among subsidiaries, improving working capital management and financial stability.

Features of Cash Pooling

The following features define cash pooling systems:

1. Centralized Cash Management

Funds from multiple accounts are managed through a single central treasury account for better financial control.

2. Balance Consolidation

Combines balances from different accounts to monitor overall cash positions more effectively and accurately.

3. Automated Transfers

Banks automatically transfer funds between accounts according to predefined rules and treasury management requirements.

4. Interest Optimization

Interest calculations are based on net balances, helping organizations reduce costs and maximize interest earnings.

5. Liquidity Support

Surplus funds from profitable accounts help support accounts facing temporary cash shortages or payment requirements.

6. Multi-Account Structure

Suitable for organizations operating multiple bank accounts, subsidiaries, or business entities simultaneously.

Types of Cash Pooling

It is mainly classified into two major types.

1. Physical Cash Pooling

Physical cash pooling transfers funds between accounts into a master account for centralized liquidity and treasury management.

How It Works:

- Surplus balances from subsidiary accounts are transferred to the central account.

- Deficit accounts receive funds from master account.

- Actual movement of money takes place daily or periodically.

2. Notional Cash Pooling

Notional pooling does not involve the physical transfer of money. Instead, the bank calculates interest based on the combined net balance of all accounts.

How It Works:

- Account balances remain separate.

- The bank notionally combines balances for interest calculation.

- Debit and credit balances offset each other virtually.

How Does Cash Pooling Work?

The process generally follows these steps:

Step 1: Multiple Accounts are Maintained

Different subsidiaries, branches, or departments maintain separate bank accounts for handling their individual operational financial transactions daily.

Step 2: Central Treasury Monitors Balances

The central treasury team regularly monitors account balances to maintain proper organizational liquidity and financial control systems.

Step 3: Surplus and Deficit Identification

Accounts with excess cash and those facing shortages are identified to enable efficient internal fund allocation and management.

Step 4: Consolidation Process

Balances from multiple accounts are consolidated, either physically or notionally, to improve liquidity management and optimize organizational cash utilization.

Step 5: Interest Optimization

Banks calculate interest using the net consolidated balance, helping organizations maximize earnings and reduce borrowing-related financial expenses.

Benefits of Cash Pooling

Cash pooling provides several financial and operational benefits.

1. Better Cash Utilization

Idle funds in one account can efficiently support accounts facing temporary shortages or operational funding requirements.

2. Lower Interest Expenses

Companies reduce reliance on external borrowing, loans, and overdrafts by utilizing internally available surplus organizational funds.

3. Improved Financial Visibility

Treasury departments gain better visibility into organization-wide cash positions, liquidity levels, and overall financial resource allocation.

4. Increased Investment Opportunities

Consolidating surplus cash enables organizations to invest available funds more efficiently, improving financial returns and growth.

5. Reduced Banking Costs

Efficient balance management and fewer intercompany transactions help organizations minimize banking fees and related operational expenses.

6. Stronger Treasury Control

Centralized cash management improves financial discipline, policy implementation, liquidity monitoring, and the treasury’s overall operational efficiency.

Challenges of Cash Pooling

Despite its advantages, it also involves certain challenges.

1. Regulatory Restrictions

Certain countries impose legal limitations on intercompany fund transfers, affecting cash-pooling structures and operational flexibility.

2. Tax Implications

Cross-border cash pooling may create transfer pricing issues, withholding taxes, and additional corporate tax compliance requirements.

3. Operational Complexity

Managing multiple subsidiaries, currencies, and banking arrangements can make treasury operations more complex and difficult to coordinate.

4. Counterparty Risk

Financial instability among participating entities may negatively impact the overall cash pool and the effectiveness of the liquidity management system.

5. Banking Dependency

Organizations depend heavily on banking infrastructure, automated systems, and treasury technologies for efficient cash pooling operations.

Real-World Examples of Cash Pooling

Here are some common real-world examples of how organizations use cash pooling to improve liquidity management and optimize cash flow.

1. Multinational Corporations

Global companies use cash pooling to manage liquidity efficiently across subsidiaries operating in multiple countries and financial systems.

2. Banking Groups

Banks and financial institutions pool funds between branches to maintain liquidity levels and meet operational funding requirements.

3. Retail Chains

Retail companies consolidate daily sales collections from multiple stores into centralized treasury accounts for efficient cash management.

4. Manufacturing Companies

Manufacturers use pooled cash systems to efficiently finance inventory purchases, production activities, and ongoing operational expenses.

Best Practices for Effective Cash Pooling

Companies can improve the effectiveness by following these practices:

1. Maintain Clear Treasury Policies

Organizations should establish clear rules for fund transfers, approvals, liquidity management, and financial risk control procedures.

2. Ensure Regulatory Compliance

Companies must review legal, banking, and tax regulations before effectively implementing domestic or cross-border cash pooling structures.

3. Use Advanced Treasury Systems

Treasury management software improves automation, reporting accuracy, cash visibility, and overall operational efficiency within pooling arrangements.

4. Monitor Liquidity Regularly

Daily liquidity monitoring helps organizations maintain optimal cash balances and effectively avoid unnecessary borrowing or cash shortages.

5. Coordinate with Banking Partners

Strong relationships with banking partners support smooth implementation, operational efficiency, and reliable cash pooling management services.

Final Thoughts

Cash pooling is a treasury management technique that centralizes organizational funds to improve liquidity, reduce borrowing costs, and optimize cash utilization. By consolidating account balances, businesses strengthen financial control and working capital management. Successful implementation requires careful handling of legal, tax, operational, and banking risks through effective planning and treasury systems.

Frequently Asked Questions (FAQs)

Q1. Why do companies use cash pooling?

Answer: Companies use cash pooling to improve cash utilization, lower borrowing costs, and centralize treasury management.

Q2. Is cash pooling legal in all countries?

Answer: No. Regulatory, tax, and banking rules differ across countries, and some jurisdictions restrict certain pooling structures.

Q3. Can cash pooling reduce borrowing needs?

Answer: Yes. Cash pooling allows organizations to use internal surplus funds instead of relying heavily on external loans or overdrafts.

Q4. Is cash pooling suitable for small businesses?

Answer: Cash pooling is generally more suitable for medium and large organizations managing multiple accounts, subsidiaries, or operational entities.

Recommended Articles

We hope that this EDUCBA information on “Cash Pooling” was beneficial to you. You can view EDUCBA’s recommended articles for more information.