What is Deleveraging?

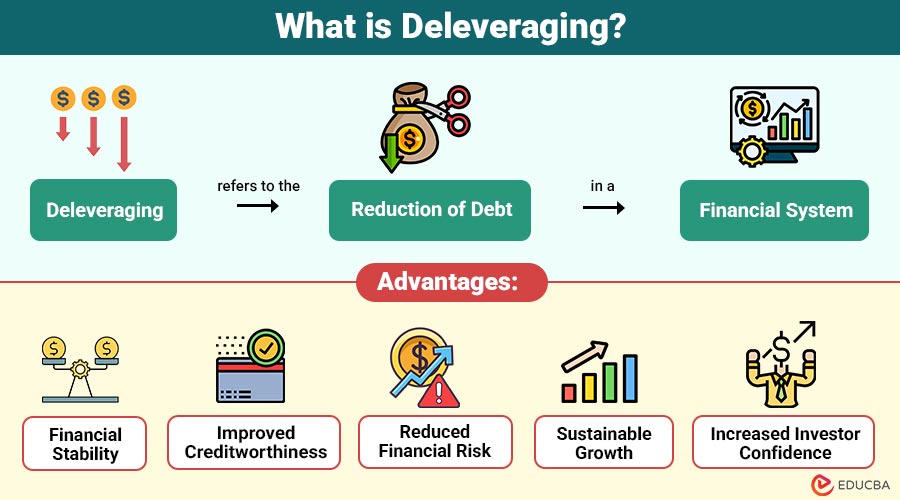

Deleveraging refers to the reduction of debt in a financial system. It happens when borrowers—such as households, corporations, banks, or governments—pay down their liabilities or restructure their financial obligations to lower risk.

It can be achieved through:

- Repaying outstanding loans

- Avoiding new debt

- Selling assets to reduce liabilities

- Increasing savings and cash flow

- Writing off or restructuring debt

Unlike normal debt repayment, deleveraging often happens on a large scale during economic downturns or financial crises.

Table of Contents:

- Meaning

- Why Does Deleveraging Happen?

- Types

- Methods

- Difference

- Advantages

- Disadvantages

- Real-World Example

Key Takeaways:

- Deleveraging reduces excessive debt, improving long-term financial stability and significantly lowering economic risks.

- Households, businesses, banks, and governments deleverage during periods of financial stress or economic uncertainty.

- It strengthens balance sheets but may temporarily reduce spending, investment, and global economic growth.

- Large-scale deleveraging commonly occurs after financial crises to restore economic balance and sustainability.

Why Does Deleveraging Happen?

Deleveraging is usually triggered by financial stress or changing economic conditions. Some key reasons include:

1. Economic Crises

During recessions or financial crises, income falls, and debt becomes harder to manage. Borrowers are forced to reduce debt to survive.

2. Excessive Borrowing

When debt levels rise too quickly in good times, they eventually become unsustainable, forcing a correction.

3. Rising Interest Rates

Higher interest rates increase the cost of borrowing, encouraging individuals and companies to reduce debt.

4. Regulatory Pressure

Governments and financial regulators may push banks and corporations to reduce leverage to improve stability.

5. Risk Management

Companies and investors often deleverage to reduce financial risk and improve credit ratings.

Types of Deleveraging

It can occur in different sectors of the economy:

1. Household Deleveraging

This happens when people pay off personal debt, including credit card debt, mortgage loans, and personal loans. It frequently results in lower consumption and more savings.

2. Corporate Deleveraging

Businesses reduce debt by selling assets, improving profitability, or issuing equity instead of borrowing. This strengthens their balance sheets.

3. Financial Sector Deleveraging

Banks and financial institutions reduce risky lending and improve capital reserves. This is common after banking crises.

4. Government Deleveraging

Governments reduce public debt through fiscal discipline, higher taxes, or controlled spending.

Methods of Deleveraging

Organizations and economies use several methods to reduce debt:

1. Debt Repayment

Organizations gradually repay outstanding loans using profits, savings, or excess cash generated from regular operations.

2. Asset Sales

Companies sell unnecessary assets or properties to generate funds and reduce overall financial liabilities effectively.

3. Equity Financing

Businesses issue new shares to investors and use the raised capital to reduce existing debt obligations.

4. Cost Reduction

Reducing operational and administrative expenses improves cash flow, helping organizations repay debts more quickly.

5. Debt Restructuring

Borrowers renegotiate repayment terms, lower interest rates, or extend loan durations to manage debt better.

6. Inflation Effect

Rising inflation decreases the real value of debt over time, making repayment financially easier for borrowers.

Difference Between Deleveraging and Leveraging

Understanding the difference between leverage and deleveraging is important:

| Deleveraging | Leveraging |

| Reducing debt to stabilize finances | Increasing debt to expand growth |

| Used during downturns or risk reduction | Used during expansion phases |

| Lower risk but slower growth | Higher potential returns and risk |

| Focus on repayment and savings | Focus on borrowing and investment |

Advantages of Deleveraging

Although deleveraging can slow economic activity in the short term, it offers long-term advantages:

1. Financial Stability

Lower debt levels reduce bankruptcy risk and improve overall financial strength amid economic uncertainty.

2. Improved Creditworthiness

Entities with lower debt appear financially reliable, attracting lenders, investors, and better borrowing opportunities.

3. Reduced Financial Risk

Lower leverage significantly reduces exposure to interest rate changes, market volatility, and economic downturns.

4. Sustainable Growth

Healthy balance sheets consistently support stable expansion, long-term profitability, and stronger future business performance.

5. Increased Investor Confidence

Investors prefer organizations with controlled debt because they appear financially secure and economically stable.

Disadvantages of Deleveraging

Despite its benefits, deleveraging can have negative short-term effects:

1. Economic Slowdown

Reduced borrowing and spending decreases investments, slowing business activities and overall economic growth temporarily.

2. Lower Consumer Demand

Households prioritizing debt repayment often significantly reduce spending on goods, services, and non-essential purchases.

3. Deflationary Pressure

Lower consumer spending can reduce prices, increasing the risk of deflation and weakening overall economic activity.

4. Job Losses

Businesses reducing costs and investments may temporarily downsize operations, resulting in unemployment and workforce reductions.

5. Credit Contraction

Banks become cautious about lending, reducing market liquidity, and limiting access to business financing opportunities.

Real-World Example

The following example illustrates how deleveraging works in a real-world economic context.

A well-known example of deleveraging occurred after the 2008 global financial crisis. Many households, banks, and corporations across the world had accumulated high levels of debt during the credit boom.

When the crisis hit:

- Credit markets tightened

- Asset prices fell

- Income levels declined

As a result:

- Households reduced spending and increased savings

- Banks reduced risky lending

- Companies focused on paying down debt instead of expansion

This widespread deleveraging slowed global economic growth but eventually led to stronger financial systems.

Final Thoughts

Deleveraging is an important financial process that reduces excessive debt and improves long-term economic stability. Although it may temporarily slow growth and spending, it strengthens financial systems by reducing risk, increasing savings, and managing liabilities effectively. It helps households, businesses, and economies maintain sustainable growth and stronger financial resilience over time.

Frequently Asked Questions (FAQs)

Q1. How does deleveraging affect the economy?

Answer: In the short term, deleveraging may slow economic growth and reduce spending, but it creates a healthier and more stable financial system over time.

Q2. Who can undergo deleveraging?

Answer: Households, businesses, banks, financial institutions, and governments can all undergo deleveraging to reduce debt burdens.

Q3. Can deleveraging lead to recession?

Answer: Large-scale deleveraging can reduce spending and investments, which may contribute to slower economic growth or a temporary recession.

Q4. How does inflation help deleveraging?

Answer: Inflation reduces real value of the debt over time, making it easier for the borrowers to repay their liabilities.

Recommended Articles

We hope that this EDUCBA information on “Deleveraging” was beneficial to you. You can view EDUCBA’s recommended articles for more information.