What is a Cashless Economy?

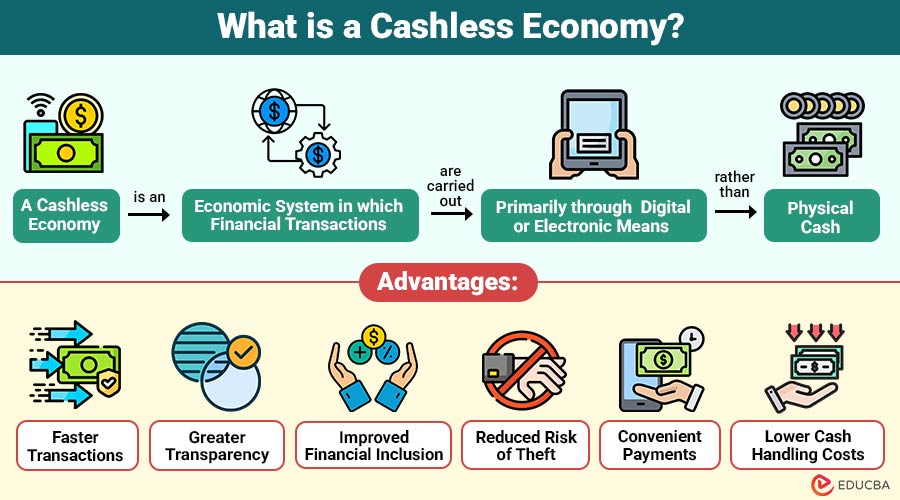

A cashless economy is an economic system in which financial transactions are carried out primarily through digital or electronic means rather than physical cash.

In a cashless economy, people use:

- Debit and Credit Cards: Cards allow users to make secure online and offline cashless transactions easily.

- Mobile Wallets: Digital wallets store money electronically for quick and convenient payments.

- UPI Payments: UPI enables instant bank transfers through secure smartphone-based payment systems.

- Internet Banking: Online banking helps users transfer funds and pay bills anytime securely.

- QR Code Payments: Users scan QR codes to make fast and secure digital payments.

- Contactless Payments: NFC technology enables quick tap-and-pay transactions using compatible devices.

The primary goal of a cashless economy is to create a faster, safer, and more transparent financial environment.

Table of Contents:

Key Takeaways:

- Cashless economies improve transaction speed, financial transparency, and digital accessibility across businesses and consumers globally.

- Digital payment systems reduce cash-handling costs while effectively supporting economic growth and financial modernization.

- Cashless economies help governments monitor transactions more effectively, reducing corruption, tax evasion, and other illegal financial activities.

- Growing smartphone and internet usage continues accelerating the adoption of cashless transactions across urban and rural economies.

Importance of a Cashless Economy

A cashless economy plays an important role in economic modernization and development.

1. Promotes Economic Growth

Efficient digital financial systems increase business productivity, consumer spending, and overall economic development significantly worldwide.

2. Supports Digital Transformation

Growing digital payment adoption encourages technological innovation, modernization, and advancement across businesses and financial sectors.

3. Enhances Tax Collection

Governments accurately monitor digital transactions, improving tax compliance, revenue collection, and financial transparency within economies.

4. Reduces Black Money

Transparent digital transaction records make illegal cash dealings, corruption, and unreported financial activities increasingly difficult to conceal.

5. Boosts Banking Sector Efficiency

Banks process transactions faster while reducing paperwork, manual operations, operational costs, and processing errors effectively.

Features of a Cashless Economy

A cashless economy has several important features that distinguish it from traditional cash-based systems.

1. Digital Transactions

Payments are completed electronically using smartphones, debit cards, computers, online banking platforms, and mobile payment applications.

2. Reduced Use of Physical Cash

People rely less on paper currency and coins for regular daily purchases, payments, and financial transactions.

3. Real-Time Payments

Digital payment systems enable instant money transfers and faster processing of transactions between individuals, businesses, and banks.

4. Financial Transparency

Electronic transaction records improve financial tracking, reduce fraud risks, and increase accountability in economic activities.

5. Banking Integration

Cashless payments are directly linked with bank accounts, digital wallets, and secure financial service platforms.

6. Use of Technology

Advanced technologies such as internet banking, payment gateways, encryption, and mobile applications support cashless-economy operations.

How Does a Cashless Economy Work?

Here are the key steps that explain how transactions are processed in a cashless economy through digital payment systems.

1. Customer Initiates Payment

A customer initiates digital payments using mobile banking, cards, UPI applications, or online payment platforms.

2. Transaction Verification

The payment platform securely verifies transaction details, account information, and payment amount before processing transactions.

3. Payment Authentication

The bank or payment gateway authenticates payment requests using encryption, passwords, OTPs, or biometric verification methods.

4. Electronic Fund Transfer

Funds are transferred electronically between sender and receiver accounts through secure digital banking networks instantly.

5. Digital Confirmation

Both parties receive digital confirmation messages, receipts, or notifications after successful completion of financial transactions.

This entire process usually takes only a few seconds.

Common Modes of Digital Payments

Here are some of the most widely used digital payment methods that support transactions in a cashless economy.

1. Debit and Credit Cards

Banks provide cards that enable customers to make secure online and offline financial transactions conveniently, everywhere.

2. Mobile Wallets

Digital wallet applications securely store electronic money for faster, easier, and cashless daily payment transactions.

3. UPI Payments

The Unified Payments Interface enables instant bank transfers on smartphones via secure, real-time digital payment systems.

4. Internet Banking

Online banking portals help users transfer funds, pay bills, and manage accounts safely anytime.

5. QR Code Payments

Customers scan QR codes in mobile applications to complete secure, instant digital payments without cash.

6. Contactless Payments

NFC technology enables users to complete secure tap-and-pay transactions quickly using compatible digital payment devices.

Advantages of a Cashless Economy

A cashless economy provides many advantages to individuals, businesses, and governments.

1. Faster Transactions

Digital payments process instantly, saving valuable time for customers, businesses, and financial institutions.

2. Greater Transparency

Electronic transaction records effectively help minimize corruption, tax evasion, fraud, and other illegal financial activities.

3. Improved Financial Inclusion

Digital banking services enable unbanked populations to access secure financial systems and banking opportunities easily.

4. Reduced Risk of Theft

People avoid carrying physical cash, significantly reducing the risk of theft, robbery, and financial loss during travel.

5. Convenient Payments

Users conveniently pay bills, shop online, and transfer money anytime from any internet-connected digital device.

6. Lower Cash Handling Costs

Governments and banks reduce expenses related to printing, transporting, storing, and managing physical currency operations.

Disadvantages of a Cashless Economy

Despite its advantages, a cashless economy also has certain disadvantages.

1. Cybersecurity Risks

Digital payment systems remain vulnerable to hacking, online fraud, cyberattacks, and unauthorized financial data breaches.

2. Dependence on Internet Connectivity

Poor internet connections or network failures can significantly disrupt digital payments and financial transactions.

3. Digital Illiteracy

Some individuals struggle using digital payment applications, online banking platforms, and modern financial technologies effectively.

4. Privacy Concerns

Electronic transactions create digital records that may expose personal financial information and reduce user privacy.

5. Technical Failures

Server crashes, software errors, or technical malfunctions can completely disrupt digital financial transaction services.

6. Exclusion of Rural Populations

Remote populations may lack smartphones, internet access, or banking infrastructure required for digital payment services.

Real-World Examples

Here are some countries that have successfully adopted digital payment systems and are moving toward becoming cashless economies.

1. Sweden

Sweden is considered one of the world’s leading cashless societies, where digital transactions dominate daily life.

2. India

India experienced rapid growth in digital payments following demonetization and the introduction of UPI.

3. South Korea

South Korea encourages digital payments through an advanced banking infrastructure.

Applications of a Cashless Economy

A cashless economy is widespread across various sectors.

1. Retail Businesses

Retail stores and supermarkets use digital payments to provide faster, secure, and convenient customer checkout experiences.

2. Banking Sector

Banks provide mobile banking, internet banking, and secure online transaction services to customers worldwide daily.

3. Transportation

Transportation services are increasingly using digital tickets, online fare payments, and contactless payment systems efficiently.

4. Healthcare

Hospitals and clinics accept electronic payments for consultations, treatments, medications, and other healthcare-related services.

5. Education

Educational institutions enable students and parents to pay fees securely through online digital payment platforms.

6. E-Commerce Platforms

Online shopping platforms rely heavily on digital payment systems to enable secure, seamless customer transactions globally.

Final Thoughts

A cashless economy promotes faster, transparent, and convenient digital financial transactions across businesses and consumers worldwide. Despite challenges such as cybersecurity risks and digital literacy issues, ongoing technological advancements are improving digital payment systems. As global economies become increasingly connected, cashless transactions will play crucial role in future economic growth and modernization.

Frequently Asked Questions (FAQs)

Q1. Can small businesses benefit from a cashless economy?

Answer: Yes, digital payments help small businesses improve transaction speed, customer convenience, and financial record-keeping.

Q2. What is the role of banks in a cashless economy?

Answer: Banks provide secure digital payment services, transaction processing, mobile banking, and online financial management systems regularly.

Q3. Is a cashless economy completely free from fraud?

Answer: No, although digital payments reduce cash theft, cyber fraud and online scams can still occur.

Recommended Articles

We hope that this EDUCBA information on “Cashless Economy” was beneficial to you. You can view EDUCBA’s recommended articles for more information.