What is Invoice Discounting?

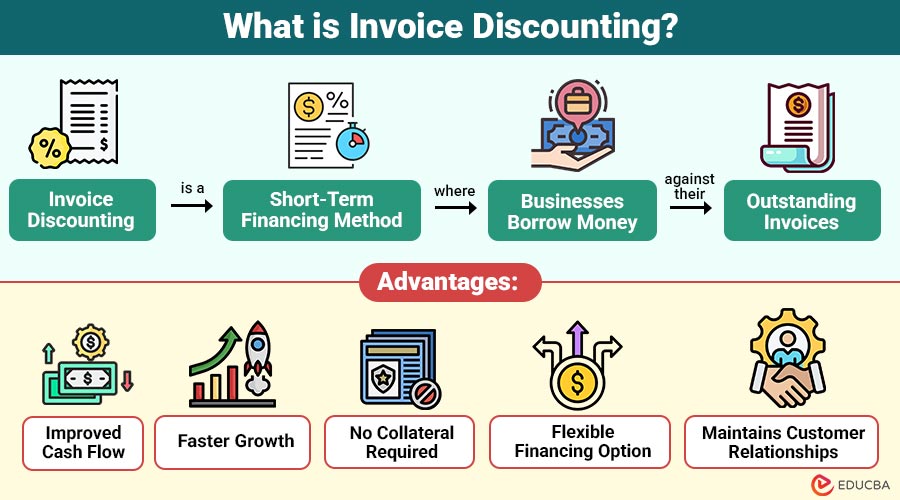

Invoice discounting is a short-term financing method where businesses borrow money against their outstanding invoices. A lender (usually bank or financial institution) advances a percentage of invoice value—typically 70% to 90%—before the customer pays.

Once the customer settles invoice, the remaining balance is released to the business after fees and interest are deducted.

Table of Contents:

- Meaning

- Key Features

- Working

- Types

- Advantages

- Disadvantages

- Use Cases

- Real-World Example

- When Should You Choose Invoice Discounting?

Key Takeaways:

- Invoice discounting provides immediate working capital by quickly unlocking funds tied up in unpaid customer invoices.

- Businesses retain control over customer relationships while improving cash flow without requiring collateral or long-term debt.

- Financing depends on customer credit worthiness, making reliable clients essential for smooth approval and risk management.

- It is ideal for managing delayed payments, supporting operations, and ensuring consistent liquidity for business growth.

Key Features of Invoice Discounting

Here are the key features that make invoice discounting a flexible and efficient financing solution for businesses:

- Quick Access to Funds: Businesses receive immediate working capital against invoices, reducing waiting time and ensuring smooth operational and financial continuity.

- Confidential Process: The process remains confidential, as customers are usually unaware of financing, preserving business relationships, and maintaining professional credibility.

- Flexible Financing: Financing is flexible, based on invoice value rather than on assets, allowing businesses to easily access funds tied to receivables.

- Improved Cash Flow: It improves cash flow by providing timely funds, helping businesses manage salaries, inventory purchases, rent, and daily expenses efficiently.

- Retained Control: Businesses retain full control over the sales ledger and customer interactions, ensuring independence while still benefiting from financing support.

How Does Invoice Discounting Work?

The process follows a structured approach:

- Sale on Credit: A company that offers products or services on credit issues an invoice with predetermined terms of payment, typically between thirty and ninety days.

- Submit Invoice to Lender: The business submits invoice details to the financing provider, initiating the process to quickly and efficiently receive funds against outstanding receivables.

- Advance Payment: The lender verifies invoice authenticity and advances a significant portion of the value, providing immediate working capital for the business’s operations.

- Customer Payment: In accordance with the initial terms of payment, the consumer pays the entire invoice amount directly to the company or lender on the scheduled due date.

- Final Settlement: The lender deducts applicable fees and interest, then releases the remaining balance to the business after successfully receiving the customer’s payment.

Types of Invoice Discounting

Here are the key types of invoice discounting businesses commonly use to manage cash flow effectively:

- Confidential Invoice Discounting: Customers remain unaware of the financing arrangements, while the business handles collections directly, thereby maintaining control and preserving strong customer relationships.

- Disclosed Invoice Discounting: Customers are informed about lender involvement and make payments directly to the financing provider, ensuring transparency and a structured payment process.

- Selective Invoice Discounting: Businesses choose specific invoices for financing, offering flexibility to manage cash flow without committing the entire sales ledger.

- Whole Turnover Invoice Discounting: All invoices are financed under a single agreement, ideal for businesses with consistent invoicing and predictable cash flow requirements.

Advantages of Invoice Discounting

Here are the key benefits that make invoice discounting a popular financing option for businesses:

- Improved Cash Flow: Businesses maintain steady cash flow, meeting daily expenses and operational needs without waiting for customer payments or invoice cycles.

- Faster Growth: Immediate access to funds enables businesses to invest in expansion, marketing, and new opportunities, supporting overall business growth.

- No Collateral Required: Does not require physical assets as collateral; instead, it relies on receivables, making it accessible to growing businesses.

- Flexible Financing Option: Financing is flexible and increases with sales volume, enabling businesses to access higher funds as invoice values and revenues grow.

- Maintains Customer Relationships: Businesses handle collections independently, ensuring customer relationships remain strong, professional, and unaffected by third-party financing involvement.

Disadvantages of Invoice Discounting

Here are the disadvantages businesses should consider before opting it:

- Cost of Financing: Interest rates and service fees increase overall costs, reducing profit margins and impacting business profitability, especially for small enterprises.

- Dependence on Customer Creditworthiness: Approval depends on customers’ creditworthiness, making financing difficult if clients have poor payment history or unreliable financial standing.

- Risk of Non-Payment: If customers delay payments or default, businesses may still be responsible, affecting cash flow and creating financial strain.

- Limited Suitability: Not suitable for businesses with low invoice volumes or irregular sales, as consistent receivables are required for effective financing.

Use Cases of Invoice Discounting

It is widely used across industries:

- Manufacturing: Manufacturers use invoice discounting to manage raw material procurement and production costs and maintain smooth operations without cash-flow disruptions.

- Wholesale & Distribution: Businesses maintain inventory levels efficiently by accessing funds quickly, ensuring a continuous supply and meeting customer demand without financial delays.

- IT & Services: Service-based companies use invoice discounting to manage payroll and operational expenses and maintain a steady cash flow during delayed client payments.

- Export Businesses: Exporters use invoice discounting to manage long international payment cycles, ensuring liquidity while waiting for overseas customer payments.

Real-World Example

Imagine a manufacturing company supplies goods worth ₹10,00,000 to a retailer with a 60-day credit period. Instead of waiting for two months, the company opts for invoice discounting.

- Lender advances 80% = ₹8,00,000 immediately

- Customer pays ₹10,00,000 after 60 days

- Lender deducts fees (say ₹20,000)

- Business receives the remaining ₹1,80,000

When Should You Use Invoice Discounting?

Invoice discounting is ideal when:

- Delayed Customer Payments: Use when customers pay more slowly, helping maintain steady cash flow and avoid operational disruptions.

- Urgent Working Capital Needs: It is ideal when businesses need immediate working capital to manage expenses, payroll, inventory, or day-to-day operations efficiently.

- Avoiding Long-Term Debt: Businesses can avoid long-term loans and interest costs by using short-term financing tied to outstanding invoices instead.

- Reliable Customer Base: Suitable when your business has financially stable and reliable customers, ensuring timely payments and smoother approval from financing providers.

- Maintain Ownership and Control: It is beneficial when businesses want to retain control over operations, customer relationships, and collections without third-party interference.

Final Thoughts

Invoice discounting is an efficient financing solution that helps businesses manage delayed payments and maintain steady cash flow. It serves as a bridge between invoicing and cash realization. With digital platforms like Trade Receivables Discounting System, access has improved, enabling MSMEs to enhance liquidity, support growth, and remain competitive in the market.

Frequently Asked Questions (FAQs)

Q1. Is invoice discounting a loan?

Answer: No, it is not a traditional loan. It is a financing method based on unpaid invoices.

Q2. Is invoice discounting suitable for small businesses?

Answer: Yes, especially for SMEs facing cash flow issues due to delayed payments.

Q3. How quickly can funds be received through invoice discounting?

Answer: Funds are usually disbursed within 24 to 72 hours after the lender verifies the invoice.

Q4. Does invoice discounting affect customer relationships?

Answer: No, especially in confidential invoice discounting, customers are unaware of the financing arrangement, preserving relationships.

Recommended Articles

We hope that this EDUCBA information on “Invoice Discounting” was beneficial to you. You can view EDUCBA’s recommended articles for more information.