What a Mortgage Broker Does?

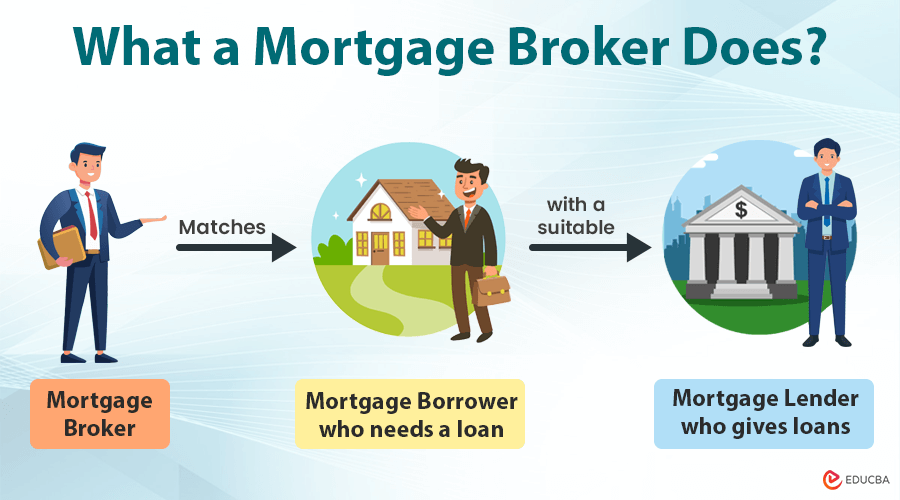

A mortgage broker is a person who connects the mortgage borrower (who needs a loan) with a suitable mortgage lender (who gives loans – banks and financial institutions).

They help borrowers get the most attractive loan offers and ensure that the borrower and the lender are an excellent match and suit each other.

In return for their services, the mortgage broker earns a commission, i.e., originating fees. This fee depends on the amount of loan which they have arranged.

Key Takeaways

- Mortgage brokers gather borrower’s details and help them find potential lenders.

- They simplify the loan process and reduce the required effort to complete formalities.

- They earn a commission after the loan processing is completed.

- While these brokers help borrowers secure good deals, sometimes deals may not meet expectations, causing potential losses for borrowers or lenders.

How Does a Mortgage Broker Work?

- When borrowers want to take out a loan, they search for a mortgage broker.

- Once appointed, the broker gathers all necessary information from the borrower, such as income, credit history, assets, and important documents.

- The broker then searches for a potential lender that suits the borrower’s needs.

- After finding a suitable lender, the broker submits the gathered information for loan approval.

- If the lender approves the loan, they provide it to the borrower.

- The broker earns a percentage of the loan amount as their fee.

Mortgage Broker Earnings/Fees

Mortgage brokers may work independently or for larger brokerage firms. They earn a commission, often called originating fees. Their fee ranges from 0.5% to 2% of the loan principal, depending on the size of the sanctioned loan. They typically receive these fees upon completing the loan transaction.

Advantages of Using a Mortgage Broker

- Mortgage brokers help both the borrower and the lender save time by efficiently managing the loan process.

- They can find a perfect match between the borrower and the potential lender so that the loan’s purpose and the transaction can be easily matched.

- Brokers quickly gather all necessary information about the borrower, such as assets, credit reports, income, and employment details, which helps lenders process loans.

- Brokers simplify the entire loan process, fostering trust between the borrower and the lender and ensuring the smooth completion of the loan transaction.

- They have access to restricted areas and information; thus, hiring a mortgage broker for any loan transaction is undoubtedly a better option.

- They can simplify the process of refinancing the loan.

- They work with multiple clients and know different lenders’ interest rates. This knowledge helps borrowers choose the best lenders based on interest rates.

- They act as experts for both borrowers and lenders, providing professional advice throughout the loan process.

Disadvantages of Using a Mortgage Broker

- Borrowers can face difficulty if they suffer from a complicated credit situation.

- Borrowers might secure lower loan rates directly from lenders compared to those obtained through brokers.

- Some lenders are unwilling to work with brokers, so the choice before the broker becomes less.

- Brokers charge for their services, and sometimes, they may not earn a commission, making each transaction risky.

- The broker will not be involved in the case of the borrower’s default, so lenders may not be very interested in hiring such brokers.

Final Thoughts

Mortgage brokers facilitate beneficial deals for both borrowers and lenders. However, some lenders prefer to avoid brokers, and brokers may occasionally provide false information. Therefore, borrowers must carefully understand the pros and cons of hiring a broker.

Moreover, brokers also face the challenge of satisfying both borrowers and lenders, and unsuccessful transactions mean wasted time and no commission. Therefore, scrutinizing the entire process before making any commitments ensures the outcome benefits borrowers, lenders, and mortgage brokers alike.

Recommended Articles

This is a guide to Mortgage Broker. Here we also discuss the definition, working, and cost of a mortgage Broker, along with advantages and disadvantages. You may also have a look at the following articles to learn more –