What is Wealth Management?

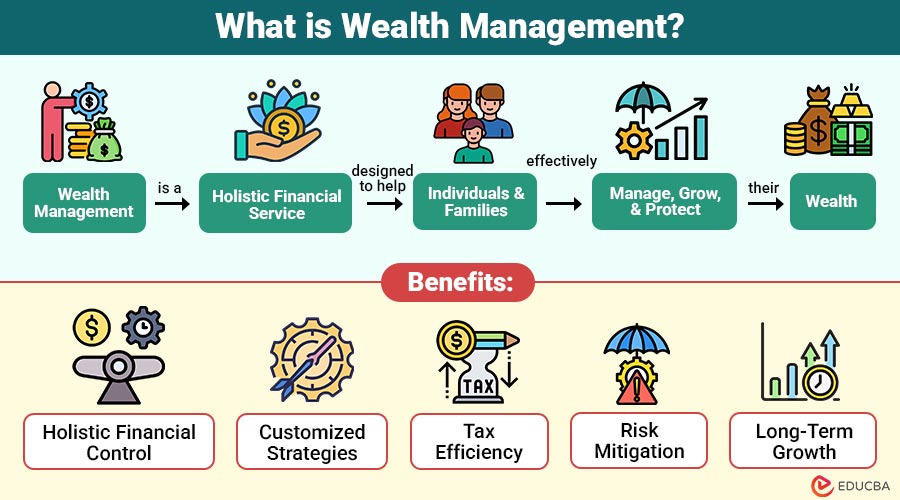

Wealth Management is a holistic financial service designed to help individuals and families effectively manage, grow, and protect their wealth. It goes beyond simple investment advice—it encompasses comprehensive financial planning, estate planning, tax optimization, risk management, and retirement planning.

A wealth manager typically provides tailored solutions that align with your financial goals, life stage, and risk tolerance. This approach ensures long-term economic stability and helps clients navigate market fluctuations with confidence.

Table of Contents:

- Meaning

- Key Components

- Process

- Benefits

- Types

- Strategies

- Real-World Examples

- Common Mistakes to Avoid

Key Takeaways:

- Wealth management combines financial planning, investments, taxes, and estate strategies to ensure long-term stability.

- Personalized strategies and diversification protect assets while optimizing growth according to individual goals and risk tolerance.

- Regular monitoring and review maintain alignment of investments with changing life circumstances and market conditions.

- Effective wealth management reduces stress, safeguards family legacy, and supports informed, confident financial decision-making.

Key Components of Wealth Management

Wealth management is built on multiple pillars, each addressing a different aspect of financial health. Below are the primary components:

1. Financial Planning

This is the foundation of wealth management. It entails evaluating your present financial situation, establishing specific objectives (such as retirement, education, or legacy), and developing a plan to reach those objectives.

2. Investment Management

Based on your goals, risk tolerance, and time horizon, wealth managers create and oversee diversified portfolios. This includes asset allocation across equities, bonds, mutual funds, and alternative investments.

3. Tax Planning

Efficient tax management helps minimize liabilities while maximizing post-tax returns. Strategies include utilizing tax-advantaged accounts, deductions, and long-term investment planning.

4. Retirement Planning

A core focus of wealth management is ensuring financial independence during retirement. For many parents, this includes a strategy to refinance Parent PLUS loans to obtain a lower interest rate, reducing their monthly debt obligations and allowing them to allocate more capital to their retirement accounts during their higher-income years.

5. Estate Planning

This entails arranging your assets to minimize taxes and legal issues and guarantee a seamless transfer of wealth to heirs. Examples of tools include wills, trusts, and power of attorney agreements.

6. Risk Management

Protecting wealth is as important as growing it. Wealth managers use insurance, diversification, and contingency funds to mitigate financial risks.

Wealth Management Process

A structured wealth management process ensures that financial goals are realistic, measurable, and achievable. The typical process includes:

1. Assessment

Collects comprehensive information on income, assets, liabilities, goals, and risk tolerance to establish a clear financial foundation.

2. Strategy Development

Designs a customized financial plan combining investments, savings, and insurance strategies tailored to personal goals and risk profile.

3. Implementation

Executes the planned strategy using suitable financial products, investment vehicles, and instruments to achieve targeted wealth objectives efficiently.

4. Monitoring and Review

Regularly tracks financial progress, evaluates performance, and adjusts strategies to stay aligned with evolving goals and market conditions.

Types of Wealth Management Services

Different individuals require different types of wealth management based on their financial situations:

1. Private Wealth Management

The company offers exclusive, personalized financial strategies for high-net-worth individuals, focusing on wealth preservation, growth, and legacy planning.

2. Personal Wealth Management

Provides customized financial planning for professionals and families, addressing investments, savings, insurance, and long-term wealth accumulation goals.

3. Corporate Wealth Management

Manages business wealth through investment planning, employee benefit structuring, succession strategies, and optimizing corporate financial performance.

4. Family Office Services

Delivers integrated management of family wealth, including estate planning, philanthropy, tax efficiency, and multi-generational financial continuity.

Benefits of Wealth Management

Wealth management offers more than just financial returns—it provides structure, peace of mind, and financial clarity. Below are the key benefits:

1. Holistic Financial Control

This approach integrates investments, taxes, estate planning, and insurance under one cohesive strategy, ensuring all financial decisions support long-term personal and family goals.

2. Customized Strategies

Creates personalized financial plans aligned with your income, lifestyle, and priorities, ensuring strategies reflect your unique objectives and evolving economic circumstances.

3. Tax Efficiency

Implements effective tax planning techniques to reduce liabilities, enhance returns, and maximize overall wealth growth through efficient income and investment structuring.

4. Risk Mitigation

Diversifies assets, manages portfolio risks, and incorporates insurance solutions to protect wealth from market fluctuations, legal claims, or unforeseen financial disruptions.

5. Long-Term Growth

This approach encourages consistent investment, disciplined saving, and compounding returns to build sustainable wealth and ensure steady financial progress over time.

Wealth Management Strategies

Here are some key strategies commonly used by wealth managers to grow, protect, and optimize wealth:

1. Diversification

To reduce risk and safeguard portfolio stability, invest in a variety of asset types, including stocks, bonds, real estate, and alternatives.

2. Asset Allocation

Strategically adjust investment mix according to age, financial goals, and market conditions to optimize returns while managing overall portfolio risk.

3. Tax-Efficient Investing

Utilize tax-advantaged accounts and long-term investment strategies to reduce tax liabilities, improving after-tax wealth growth and portfolio efficiency.

4. Estate Structuring

Create trusts, wills, and legal frameworks to ensure smooth wealth transfer, protect beneficiaries, and minimize estate taxes or legal complications.

5. Regular Portfolio Review

Continuously monitor and adjust investments to ensure alignment with evolving financial goals, risk tolerance, and changes in market conditions.

Real-World Examples

Here are practical scenarios illustrating how wealth management strategies are applied in everyday life:

1. Professional Athlete

A footballer nearing retirement partners with a wealth manager to invest earnings wisely, plan for reduced future income, and create a legacy fund for his family.

2. Business Owner

A startup founder diversifies assets into real estate, bonds, and a trust fund to protect against business risks while securing personal wealth.

3. Retired Couple

They work with an advisor to ensure a stable retirement income through annuities, dividend-paying stocks, and tax-efficient withdrawals.

Common Mistakes to Avoid

Here are some common mistakes people make in wealth management and how they can impact financial goals:

1. Neglecting Diversification

Putting all of your money into one asset class exposes you to more market swings, which raises the risk and could result in large portfolio losses.

2. Ignoring Tax Implications

Failing to plan for taxes can reduce investment returns, as capital gains, income taxes, and penalties may erode overall wealth.

3. Lack of Regular Review

Failing to review financial plans and portfolios periodically may misalign investments with changing life circumstances, goals, or evolving market conditions.

4. Emotional Investing

Making investment decisions driven by fear, greed, or short-term market movements often leads to poor outcomes and financial setbacks.

5. No Estate Plan

Absence of wills, trusts, or legal estate planning can create disputes, delays, and higher taxes, jeopardizing wealth transfer to heirs.

Final Thoughts

Wealth management is not just about accumulating money—it is about managing it wisely to achieve financial independence, family security, and legacy goals. A well-structured wealth management plan integrates investments, taxes, estate planning, and risk control under one umbrella, ensuring that your wealth works for you across every stage of life. Partnering with a qualified wealth manager empowers you to make informed decisions, balance risk and reward, and secure your financial future with confidence.

Frequently Asked Questions (FAQs)

Q1. Who needs wealth management services?

Answer: Anyone with multiple financial goals, assets, or sources of income can benefit—especially professionals, entrepreneurs, and high-net-worth individuals.

Q2. Can small investors use wealth management services?

Answer: Yes. Many firms offer scalable wealth management solutions tailored to smaller portfolios.

Q3. How often should a wealth plan be reviewed?

Answer: At least once a year, or after significant life or market changes.

Q4. What is wealth management’s primary objective?

Answer: To preserve, grow, and transfer wealth efficiently while minimizing risks and taxes.

Recommended Articles

We hope that this EDUCBA information on “Wealth Management” was beneficial to you. You can view EDUCBA’s recommended articles for more information.