Introduction

Understanding how different types of assets function is essential for effective financial planning. Among the most fundamental classifications are liquid assets and illiquid assets. These categories determine how quickly you can access your money and how flexible your financial position is in emergencies or when pursuing investment opportunities.

This guide provides a detailed comparison of liquid assets vs illiquid assets, their characteristics, advantages, disadvantages, and practical examples in real-world financial decision-making.

Table of Contents:

- Introduction

- What are Liquid Assets?

- What are Illiquid Assets?

- Key Differences

- Advantages and Disadvantages

- Real-World Example

- How to Balance Liquid and Illiquid Assets?

- When Should you Choose Liquid Assets and Illiquid Assets?

- Comon Mistakes to Avoid

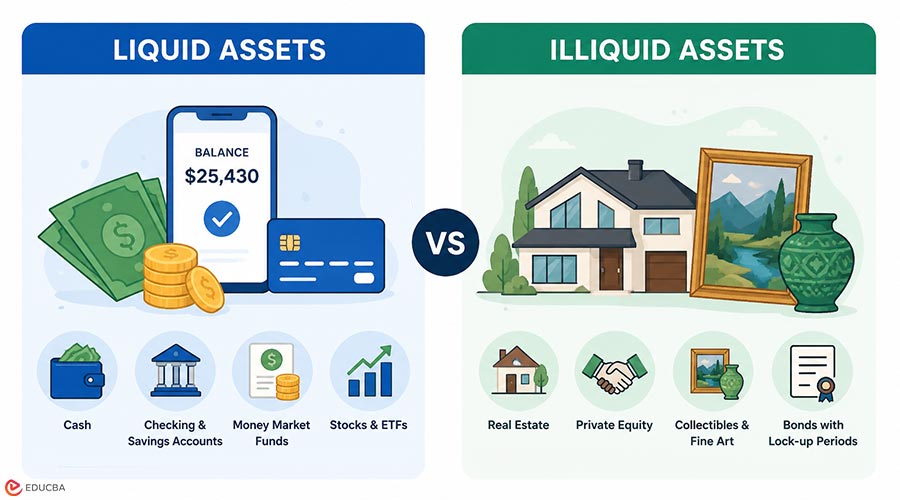

What are Liquid Assets?

Liquid assets are the financial resources that can be rapidly and easily converted into cash without significantly affecting their market value. These assets are highly accessible and are typically used to meet short-term financial needs.

Examples of Liquid Assets:

- Cash in hand

- Savings and current bank accounts

- Money market instruments

- Treasury bills

- Publicly traded stocks and mutual funds

Key Characteristics:

- High convertibility into cash

- Minimal or no loss in value during conversion

- Easily accessible

- Typically lower returns compared to long-term investments

What are Illiquid Assets?

Illiquid assets are those that cannot be easily or quickly converted into cash without a potential loss in value or a lengthy selling process. These assets are usually held for long-term growth and wealth accumulation.

Examples of Illiquid Assets:

- Real estate properties

- Land and buildings

- Private equity investments

- Collectibles (art, antiques)

- Retirement funds with withdrawal restrictions

Key Characteristics:

- Low convertibility

- Longer selling time

- Possible value fluctuation during the sale

- Often, higher potential returns over time

Key Differences Between Liquid and Illiquid Assets

The table below highlights the major differences between liquid and illiquid assets for better financial understanding.

| Basis | Liquid Assets | Illiquid Assets |

| Definition | Easily convertible to cash | Difficult to convert to cash quickly |

| Time to Convert | Immediate or short-term | Long-term |

| Risk Level | Lower risk | Higher risk |

| Return Potential | Lower returns | Higher returns |

| Price Stability | Stable | Can fluctuate |

| Usage | Emergency funds, daily expenses | Wealth building, long-term investment |

Advantages and Disadvantages of Liquid Assets and Illiquid Assets

Here are the key advantages and disadvantages of liquid and illiquid assets to help you understand their practical impact on financial planning.

Advantages of Liquid Assets:

- Liquid assets provide immediate access to funds, ensuring financial security in emergencies or when funds are needed urgently.

- They carry relatively low risk and offer high stability, making them suitable for conservative financial planning strategies.

- Liquid assets effectively support short-term financial needs, helping individuals manage expenses without delays caused by asset liquidation.

- They are easy to manage and monitor, allowing individuals to track finances and maintain better financial control.

Disadvantages of Liquid Assets:

- Liquid assets generally offer lower returns than long-term investments, limiting overall potential for wealth accumulation over time.

- They may lose value due to inflation, reducing purchasing power and diminishing real returns on held funds.

- Easy access can encourage overspending, leading to poor financial discipline and reduced long-term savings potential.

- Liquid assets may offer limited tax advantages, reducing opportunities for tax savings compared to certain long-term investments.

Advantages of Illiquid Assets:

- Illiquid assets typically offer higher potential returns, making them suitable for long-term investment and wealth growth strategies.

- They support long-term wealth creation by appreciating over time, helping individuals achieve major financial goals effectively.

- Illiquid assets often provide protection against inflation, preserving value and maintaining purchasing power as prices rise.

- They enhance portfolio diversification by reducing dependence on liquid investments and spreading financial risk across asset classes.

Disadvantages of Illiquid Assets:

- Illiquid assets are difficult to convert into the cash quickly, limiting access to funds during urgent financial situations.

- They involve higher transaction costs, including legal, administrative, and brokerage expenses, reducing overall investment profitability margins.

- Their value depends on market conditions, causing fluctuations that may impact returns and overall investment stability negatively.

- Illiquid assets are unsuitable for emergency needs because they cannot provide immediate funds when sudden financial needs arise.

Real-World Example

Here is a simple example illustrating how liquid and illiquid assets impact financial flexibility in real-life situations:

Consider two individuals with different asset allocations:

Person A:

Keeps most of their money in savings accounts and stocks. When faced with a sudden medical emergency, they can quickly access funds without stress.

Person B:

Invests heavily in real estate and long-term assets. While they may have higher net worth, accessing cash during emergencies becomes challenging due to the time required to sell property.

This example highlights the importance of balancing both asset types rather than relying solely on one.

How to Balance Liquid and Illiquid Assets?

A well-structured financial plan requires a mix of both liquid and illiquid assets. The right balance depends on your financial objectives, income level, and risk tolerance.

- Keep at least 3–6 months of expenses in liquid assets to handle unexpected situations.

- Allocate a portion of your portfolio to illiquid assets to create long-term wealth.

- Younger individuals may be more willing to invest in illiquid assets, while those nearing retirement should prioritize liquidity.

- Avoid putting all your funds into a single asset class. A diversified approach reduces overall financial risk.

- Financial needs change over time, so review and adjust your asset allocation periodically.

When Should You Choose Liquid Assets and Illiquid Assets?

Here are the key situations that help you decide between liquid and illiquid assets:

Liquid Assets are more Suitable when:

- Choose liquid assets when you need quick access to money for immediate financial requirements or emergencies.

- Liquid assets are ideal for building an emergency fund to cover unexpected financial situations or expenses.

- They are suitable for those who prefer low-risk investments that provide stability and effectively protect their capital.

- Liquid assets work best when you have short-term financial goals that require flexibility and easy access to funds.

Illiquid Assets are more Suitable when:

- Choose illiquid assets when you are planning for long-term wealth creation and financial growth.

- They are appropriate when you can tolerate limited access to funds without affecting your financial stability.

- Illiquid assets are beneficial for higher returns through long-term investment strategies.

- They are suitable for diversifying your investment portfolio and reducing overall financial risk.

Common Mistakes to Avoid

Here are some common mistakes to watch out for when managing liquid and illiquid assets:

- Investing all funds in illiquid assets can create financial stress during emergencies.

- Keeping too much money in liquid form may reduce potential returns over time.

- Relying on a single asset type increases financial risk.

- Not aligning assets with financial goals can lead to inefficiencies.

Final Thoughts

Both liquid and illiquid assets play essential roles in financial planning. Liquid assets ensure accessibility, stability, and short-term security, while illiquid assets support long-term growth and wealth creation. A balanced allocation between both helps achieve financial resilience, meet immediate and future goals, and build a strong, sustainable financial foundation.

Frequently Asked Questions (FAQs)

Q1. Why are illiquid assets important?

Answer: They help in long-term wealth creation and often provide higher returns compared to liquid assets.

Q2. How much liquidity should I maintain?

Answer: It is generally recommended to keep 3–6 months of living expenses in liquid assets.

Q3. Can illiquid assets generate regular income?

Answer: Yes, some illiquid assets, such as real estate or certain long-term investments, can generate passive income through rent, dividends, or interest over time.

Q4. How does inflation affect liquid and illiquid assets?

Answer: Inflation can reduce the purchasing power of liquid assets like cash, while certain illiquid assets such as real estate may appreciate and help hedge against inflation over time.

Recommended Articles

We hope that this EDUCBA information on “Liquid Assets vs Illiquid Assets” was beneficial to you. You can view EDUCBA’s recommended articles for more information.