What is a Ghost Employee?

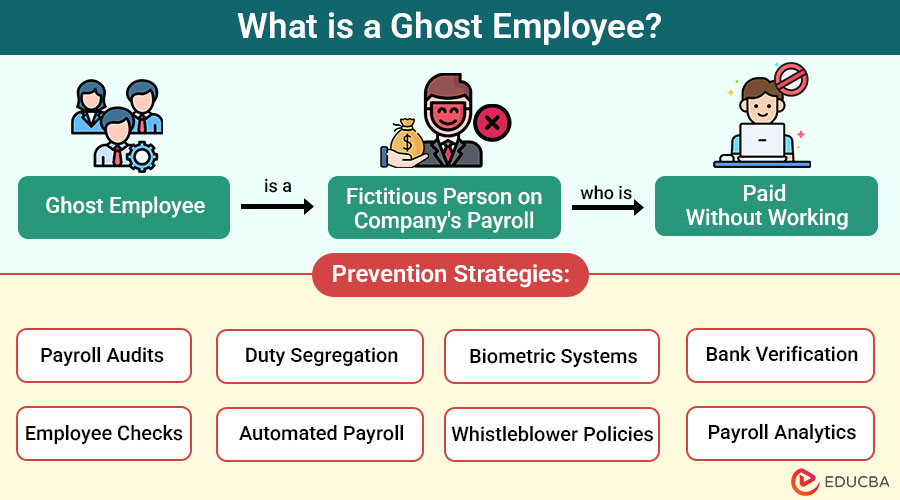

A ghost employee is a fictitious or non-existent person who is listed on a company’s payroll system but does not work for the organization. The salary and benefits for this “employee” are fraudulently collected by someone within the company, often a payroll manager, HR staff, or supervisor.

For example, Sarah, a payroll officer, creates a fake employee named “John Smith” and directs his salary to her bank account. She logs fake attendance and keeps the salary low to avoid detection. Over 18 months, she steals $75,000 before an audit reveals that John never accessed the workplace.

Table of Contents:

- Meaning

- How Ghost Employees Operate?

- Who Commits This Fraud?

- How to Spot a Ghost Employee?

- Consequences of Ghost Employee Fraud

- How to Prevent Ghost Employee Fraud?

- Role of Technology in Combating Payroll Fraud

- Legal and Ehical Responsibilities

Key Takeaways:

- Ghost employee fraud involves insiders manipulating payroll systems to divert unauthorized salaries to themselves.

- Strong internal controls, regular audits, and role-based access can deter and detect payroll fraud early.

- Technology like AI, audit trails, and biometrics plays a crucial role in preventing payroll manipulation.

- Unchecked fraud risks financial losses, legal issues, donor distrust, and deterioration in employee morale.

How Ghost Employees Operate?

The process of operating ghost employees involves a few common steps:

1. Creation of a Fake Profile

A ghost employee may be created by using fictitious details or by duplicating an existing employee’s information with minor variations (e.g., a different employee ID).

2. Entry into the Payroll System

Someone with access to the payroll system inputs the ghost employee’s details, setting them up to receive regular paychecks.

3. Collection of Payment

The fraudster redirects the funds meant for the ghost employee to an account they control. In some cases, they issue and cash the checks manually.

4. Evasion of Detection

The fraudster may rotate ghost employees, change names, or adjust records periodically to avoid audits or scrutiny.

Who Commits this Fraud?

Ghost employee schemes are typically carried out by:

1. Payroll or HR Staff

These individuals can create fictitious employees or keep terminated staff on payroll, diverting salaries for personal gain without immediate detection.

2. Department Managers

Managers may add ghost employees to inflate department budgets or embezzle funds by authorizing payments to non-existent staff under their supervision.

3. IT Personnel

IT personnel can exploit system vulnerabilities to create or conceal ghost employee entries, bypassing controls that normally detect unauthorized payroll modifications or discrepancies.

4. Colluding Employees

Groups of employees may collaborate, fabricating documents such as attendance logs or HR files to legitimize ghost workers and evade suspicion during audits or reviews.

How to Spot a Ghost Employee?

Detecting a ghost employee requires vigilance. Here are some common warning signs:

1. Duplicate Bank Account Numbers

Multiple employees receiving salaries deposited into the same bank account may indicate that one person is collecting pay for fictitious or duplicate identities.

2. Unusual Employee Records

Files with missing identification, incomplete personal details, or inconsistent HR data can indicate fabricated records for ghost employees, which are used to bypass verification procedures.

3. Unrecognized Names

If coworkers or supervisors do not recognize certain names on the payroll, it may mean those individuals are not working in the department or even exist.

4. Manual Payroll Entries

Frequent manual changes to payroll, off-cycle payments, or retroactive adjustments can be signs of someone attempting to manipulate records to pay ghost employees.

5. Lack of Physical Presence

Employees who never attend meetings, do not clock in regularly, or are never seen by others could be fake or falsely retained on payroll.

6. Mismatch in Work Records

A lack of assigned tasks, output, or performance reviews for an employee raises suspicions about whether the individual is performing any work.

Consequences of Ghost Employee Fraud

Ghost employee fraud not only incurs financial costs but also damages trust and reputation. Some key consequences include:

1. Financial Losses

Ghost employee fraud leads to substantial financial damage over time through repeated unauthorized salary payments that drain company or organizational resources unnecessarily.

2. Legal Repercussions

Employees involved may face civil lawsuits or criminal prosecution, while organizations could suffer penalties for poor oversight and failure to maintain proper internal controls.

3. Reputational Harm

The revelation of payroll fraud can severely damage public trust, especially in government agencies or nonprofits, where transparency and accountability are critical to maintaining stakeholder confidence.

4. Operational Disruption

Investigating and addressing ghost employee fraud disrupts daily operations, often requiring audits, staffing changes, and new policies to restore system integrity and prevent recurrence.

How to Prevent Ghost Employee Fraud?

To protect against ghost employee fraud, organizations must adopt a multi-layered approach that combines technology, auditing, and effective governance.

1. Payroll Audits

Schedule routine internal and external payroll audits to identify discrepancies between payment records and actual employees, helping detect and prevent ghost employee schemes early.

2. Duty Segregation

Divide responsibilities among multiple staff members so that no single person handles hiring, payroll processing, and payment approval, thereby reducing the opportunity for fraud to occur undetected.

3. Biometric Systems

Utilize fingerprint or facial recognition systems to link physical presence to attendance records, ensuring only actual employees are paid based on real work attendance.

4. Bank Verification

Verify that each employee’s bank account matches HR records and regularly check for duplicate or suspicious banking details linked to multiple payroll entries.

5. Employee Checks

Perform regular on-site spot checks and physical headcounts to confirm that all listed employees are actively present and legitimately employed by the organization.

6. Automated Payroll

Use secure, automated payroll software that tracks user actions, flags irregular activity, and prevents unauthorized manual entries that could conceal ghost employee fraud.

7. Whistleblower Policies

Establish anonymous reporting channels and protect whistleblowers to encourage staff to report suspicious payroll or employee activity without fear of retaliation.

8. Payroll Analytics

Leverage data analytics tools to monitor payroll trends, flag unusual spikes in wages continuously, duplicate employee information, or inconsistent attendance-to-payment ratios for further investigation.

Role of Technology in Combating Payroll Fraud

Modern payroll systems now come with built-in features to detect fraud:

1. Audit Trails

Modern payroll systems maintain comprehensive logs of all changes, allowing organizations to track who made modifications, when they occurred, and what data was affected.

2. AI and Machine Learning

Advanced systems use AI to detect irregular patterns in salaries, attendance, or banking details, automatically flagging suspicious activity for further investigation and review.

3. Integration with HR and Timekeeping Systems

Seamless integration between payroll, HR, and attendance systems ensures real-time synchronization of employee data, reducing the risk of errors or fraudulent discrepancies.

4. Role-Based Access Controls

Limiting access to important payroll functions according to user responsibilities reduces the opportunities for insider fraud and ensures that only authorized personnel make crucial modifications.

Legal and Ethical Responsibilities

Beyond financial prudence, preventing ghost employee fraud is a legal and ethical obligation. Failing to detect and prevent fraud can expose a company to:

1. Regulatory Penalties

Organizations that fail to prevent or address payroll fraud may face fines, sanctions, or license revocation from regulatory authorities for violating labor and financial laws.

2. Shareholder Lawsuits

In corporate settings, undetected fraud can lead to lawsuits from shareholders who suffer financial losses due to mismanagement, negligence, or breaches of fiduciary duty.

3. Loss of Funding

Donors, grant providers, or government agencies withdraw or withhold funding when they uncover fraud, citing a loss of trust and accountability failures.

4. Damage to Employee Morale and Workplace Culture

Discovering fraud can erode trust among staff, demoralize honest employees, and foster a culture of suspicion that is toxic, ultimately impacting productivity and retention.

Final Thoughts

A ghost employee might be invisible, but the damage they cause is all too real. As businesses expand and digitize their operations, they must also evolve their strategies to protect payroll systems from manipulation and fraud. Vigilant auditing, robust internal controls, and the use of modern payroll software are crucial in defending against this form of fraud. Ultimately, a transparent, accountable workplace culture is the most effective antidote to the ghost employee problem.

Frequently Asked Questions (FAQs)

Q1. How does ghost employee fraud differ from payroll errors or administrative mistakes?

Answer: Ghost employee fraud is intentional deception, while payroll errors are accidental mistakes without fraudulent intent or benefit to the perpetrator.

Q2. Can ghost employee fraud happen in small businesses, or is it limited to large organizations?

Answer: Yes, small businesses are often more vulnerable due to limited controls, fewer staff, and less frequent payroll audits or oversight.

Q3. What role does company leadership play in preventing ghost employee fraud?

Answer: Leadership enforces ethical culture, implements strong controls, ensures transparency, and encourages staff to report suspicious payroll activity safely.

Q4. Is it possible to recover losses from ghost employee fraud once it is discovered?

Answer: Recovery is possible through legal action or insurance, but prevention through audits and controls is far more effective and reliable.

Recommended Articles

We hope that this EDUCBA information on “Ghost Employee” was beneficial to you. You can view EDUCBA’s recommended articles for more information.