What is General Ledger?

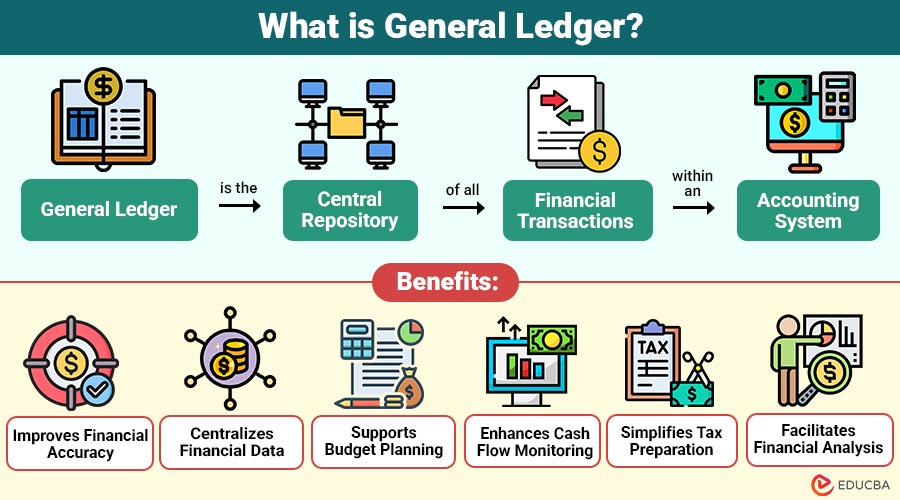

A general ledger is the central repository of all financial transactions within an accounting system. It records every financial event, including sales, purchases, expenses, income, assets, liabilities, and equity. Transactions are first entered into journals and then posted to the appropriate ledger accounts.

The general ledger serves as the foundation for preparing key financial statements, including balance sheet, income statement, and cash flow statement. Every business, regardless of its size, relies on a general ledger to maintain accurate accounting records and ensure financial transparency.

In simple terms, a general ledger is the master book of accounts, where every financial transaction is categorized and recorded for reporting and analysis.

Table of Contents:

Key Takeaways:

- A general ledger organizes all financial transactions into accounts, supporting consistent, accurate reporting and informed business decision-making.

- It records debits and credits systematically, ensuring balanced accounts, financial transparency, and reliable accounting records.

- General ledger data efficiently supports financial statements, budgeting, auditing, tax compliance, and effective cash flow management.

- Modern accounting software automates general ledger processes, reducing errors, improving accuracy, and significantly increasing operational efficiency.

Importance of General Ledger

The following points highlight the reasons why a general ledger is important for maintaining accurate financial records, reporting, compliance, and effective business decision-making.

1. Maintains Complete Financial Records

Records every business transaction systematically, ensuring complete, organized financial data while minimizing omissions, inconsistencies, and accounting recordkeeping errors effectively.

2. Supports Financial Reporting

Supplies the precise financial information needed to create cash flow statements, balance sheets, income statements, and other crucial business reports.

3. Helps Track Income and Expenses

Enables businesses to monitor revenue, expenses, profitability, and spending patterns throughout each accounting period for better financial control.

4. Improves Decision-Making

Delivers reliable financial information, helping managers evaluate performance, allocate resources wisely, and make strategic business decisions confidently.

5. Ensures Regulatory Compliance

Maintains accurate accounting records that support tax filing, regulatory compliance, financial transparency, and adherence to applicable accounting standards.

6. Simplifies Auditing

Organized ledger entries enable auditors to verify transactions, trace account balances, identify discrepancies, and complete audits more efficiently.

7. Detects Errors and Fraud

Regular ledger reconciliation identifies accounting errors, duplicate transactions, unauthorized activities, and potential fraud before causing significant financial losses.

Key Components of a General Ledger

A general ledger consists of multiple accounts that classify financial transactions.

1. Account Number

A unique identification number is assigned to each ledger account for accurate classification, organization, and transaction tracking purposes.

2. Account Name

Specifies the financial account category, clearly identifying the purpose and type of business transactions recorded in ledgers.

3. Date

Records the exact transaction date, ensuring consistent chronological organization and accurate financial reporting throughout the accounting period.

4. Journal Reference

Links each ledger entry to its original journal entry, improving traceability, verification, and audit accuracy across records.

5. Description

Provides a brief explanation of each transaction, helping users understand its purpose and supporting financial documentation requirements.

6. Debit Amount

Records increases in assets and expenses or decreases in liabilities, equity, and revenue accounts accurately during transactions.

7. Credit Amount

Accurately records increases in liabilities, equity, and revenue, or decreases in assets and expense accounts, during transactions.

8. Running Balance

Displays the updated account balance after each transaction, helping to continuously monitor financial position and account activity over time.

How Does a General Ledger Work?

The accounting cycle follows a structured process for maintaining the general ledger.

Step 1: Record Transactions

Business transactions are initially recorded in journals.

Example:

Purchase of office equipment.

Step 2: Classify Transactions

Each transaction is assigned to appropriate account.

Examples include:

- Cash

- Equipment

- Revenue

- Expenses

Step 3: Post to Ledger

Journal entries are transferred to the respective ledger accounts.

Step 4: Update Account Balances

Debit and credit entries adjust the running balance.

Step 5: Prepare Trial Balance

The balances of all ledger accounts are summarized to verify the accuracy of the accounting.

Step 6: Generate Financial Statements

The ledger data is used to prepare:

- Balance Sheet

- Income Statement

- Cash Flow Statement

Types of General Ledger Accounts

General ledger accounts are grouped into five major types.

1. Assets

Assets are valuable resources owned by business that provide future economic benefits and support daily operations, growth, and profitability.

Examples:

- Cash

- Inventory

- Equipment

2. Liabilities

Liabilities are financial obligations a business owes to external parties that require future payments of cash, goods, services, or other assets.

Examples:

- Loans

- Accounts Payable

- Taxes Payable

3. Equity

Equity represents the owner’s financial interest in the business after deducting liabilities from total assets, reflecting the overall net business value.

Examples:

- Capital

- Retained Earnings

- Owner’s Equity

4. Revenue

Revenue represents income earned from selling products, providing services, or other business activities, increasing profitability and overall financial performance.

Examples:

- Sales Revenue

- Service Revenue

- Interest Income

5. Expenses

Expenses are business costs incurred in the course of operations to generate revenue, reducing profits while supporting everyday activities and organizational growth.

Examples:

- Rent Expense

- Utility Expense

- Salaries Expense

Example of a General Ledger

The table below provides a basic example of how transactions are recorded in a general ledger.

| Date | Account | Description | Debit($) | Credit($) | Balance($) |

| Jan 1 | Cash | Owner Investment | 20,000 | – | 20,000 |

| Jan 3 | Equipment | Purchased Equipment | 5,000 | – | 5,000 |

| Jan 3 | Cash | Equipment Purchase | – | 5,000 | 15,000 |

| Jan 10 | Sales Revenue | Product Sales | – | 3,500 | 3,500 |

| Jan 10 | Cash | Customer Payment | 3,500 | – | 18,500 |

This simplified example illustrates how transactions affect multiple accounts while maintaining a balance of debits and credits.

Benefits of Using a General Ledger

A general ledger provides several operational and financial benefits.

1. Improves Financial Accuracy

Proper transaction recording minimizes accounting errors, ensures consistent records, and improves the overall accuracy of financial information.

2. Centralizes Financial Data

Stores all financial transactions within one organized system, making information easier to access, manage, and review efficiently.

3. Supports Budget Planning

Historical financial records help businesses forecast future budgets, allocate resources wisely, and control spending more effectively.

4. Enhances Cash Flow Monitoring

Tracks cash inflows and outflows accurately, helping businesses maintain liquidity and manage financial obligations efficiently throughout operations.

5. Simplifies Tax Preparation

Accurate ledger records streamline tax calculations, reduce filing errors, and simplify compliance with applicable tax regulations annually.

6. Facilitates Financial Analysis

Provides reliable financial data to effectively evaluate profitability, operational efficiency, business performance, and long-term financial trends.

Challenges of General Ledger Management

Although essential, maintaining a general ledger can present certain challenges.

1. Manual Data Entry Errors

Human errors in transaction recording can create inaccurate financial records, significantly affecting reporting, reconciliation, and overall accounting reliability.

2. Duplicate Transactions

Recording the same transaction multiple times causes inaccurate account balances, misleading financial reports, and unnecessary reconciliation challenges later.

3. Delayed Posting

Late transaction updates reduce reporting accuracy, delay financial insights, and undermine timely business planning and decision-making.

4. Reconciliation Issues

Differences between ledger balances and bank records require careful investigation, corrections, and regular reconciliation to maintain financial accuracy.

5. Complex Account Structures

Large organizations manage numerous ledger accounts, making financial organization, maintenance, reporting, and monitoring significantly more complex and time-consuming.

6. Compliance Requirements

To avoid fines and maintain financial transparency, businesses must always adhere to accounting standards, tax laws, and reporting obligations.

Final Thoughts

A general ledger is the foundation of an accounting system, organizing financial transactions into key accounts for accurate reporting and analysis. It improves financial accuracy, supports compliance, simplifies audits, enhances decision-making, and provides businesses with reliable financial information essential for effective management, transparency, and sustainable long-term growth.

Frequently Asked Questions (FAQs)

Q1. Can a business maintain a general ledger manually?

Answer: Yes. Small businesses may use paper-based or spreadsheet-ledgers, while medium and large organizations typically use accounting software for greater accuracy and efficiency.

Q2. Can accounting software automate general ledger management?

Answer: Yes. Modern accounting software automatically posts journal entries, updates account balances, generates reports, and reduces the risk of manual errors.

Q3. What happens if the general ledger is not maintained properly?

Answer: Poor ledger maintenance can lead to inaccurate financial reports, reconciliation problems, tax filing errors, compliance issues, and unreliable business insights.

Q4. How long should businesses retain general ledger records?

Answer: The retention period depends on local tax laws and regulatory requirements. Many businesses keep general ledger records for at least 5–7 years, while some industries may require longer retention periods.

Recommended Articles

We hope that this EDUCBA information on “General Ledger” was beneficial to you. You can view EDUCBA’s recommended articles for more information.