What is Fedwire?

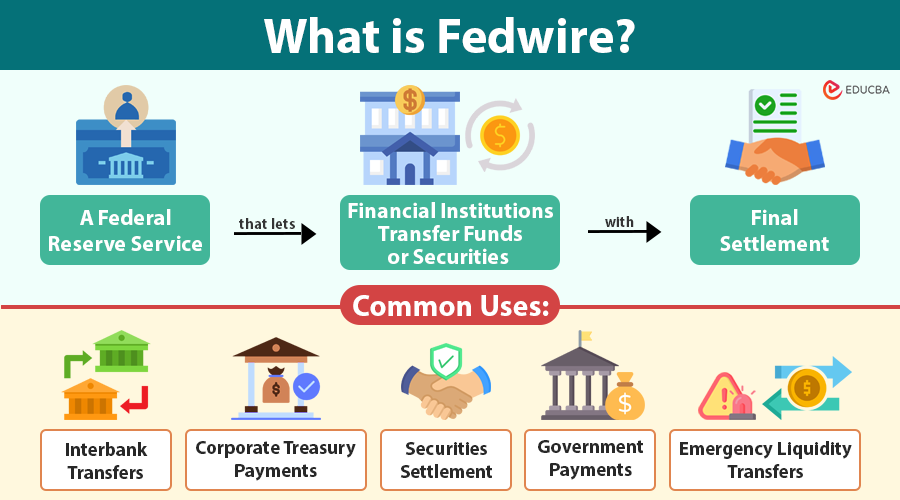

Fedwire is a specialized electronic wire transfer service operated by the Federal Reserve Banks. It enables financial institutions to transfer funds or securities in real-time, on a transaction-by-transaction basis, with immediate and final settlement.

Unlike other payment systems, such as check clearing or Automated Clearing House (ACH), which can take hours or days to settle fully, Fedwire provides instant availability of funds, making it ideal for high-value and time-sensitive payments.

For example, suppose a corporation in New York buys $20 million in U.S. Treasury bonds through its bank. The bank uses Fedwire to instantly transfer $20 million from its Federal Reserve account to the seller’s bank account at another Federal Reserve Bank. Within seconds, the Federal Reserve provides a final and irrevocable settlement of the funds, enabling the seller’s bank to complete the securities trade without delay.

Table of Contents

- What is Fedwire?

- Common Uses of Fedwire

- History of Fedwire

- How Does Fedwire Work?

- Participants in the Fedwire System

- Types of Fedwire Services

- Features of Fedwire

- Security Measures

- Operating Hours

- Fedwire vs. CHIPS

- The Role of Fedwire in the U.S. Financial System

- Recent Developments and the Future of Fedwire

Key Takeaways

- Fedwire enables real-time, irrevocable, high-value transfers of funds and securities, supporting critical interbank and government payments.

- Operated by the Federal Reserve, Fedwire ensures instant settlement and legal finality, reducing systemic risk in the U.S. financial system.

- It serves banks, government agencies, and clearinghouses, but individuals can only access it indirectly through their financial institutions.

- Fedwire offers both funds and securities settlement services, integrating multiple financial market activities into a single secure platform.

- Robust security measures — including encryption, multi-factor authentication, and disaster recovery systems — protect Fedwire as a systemically important infrastructure.

- Fedwire remains the backbone of large-value payments while complementing newer systems like FedNow for smaller, instant consumer transactions.

Common Uses of Fedwire

Some of the most common uses of Fedwire include:

- Interbank transfers: Large banks move funds between their accounts to manage liquidity needs.

- Corporate treasury payments: Corporations settle high-value supplier invoices, acquisitions, or strategic investments.

- Securities settlement: Payments for purchases of U.S. Treasury bonds and other government-backed instruments.

- Government payments: Disbursements such as Social Security benefits, tax refunds, and federal procurement payments.

- Emergency liquidity transfers: During periods of financial stress, banks rely on Fedwire to quickly reallocate funds and meet urgent obligations.

Fedwire’s legal finality ensures that once a payment is sent and settled, it cannot be reversed, thereby reducing systemic risk and providing certainty to all participants.

History of Fedwire

The roots of Fedwire stretch back more than a century. In 1918, the Federal Reserve established an early wire transfer network that used Morse code over leased Western Union telegraph lines to connect its Reserve Banks. This groundbreaking innovation enabled banks to transfer funds far more quickly than sending paper checks by train or courier.

By the 1920s, the network had expanded to serve the growing U.S. economy. As technology progressed, Fedwire transitioned:

- From telegraph-based instructions

- To telephone-based settlement messages

- Then, there were computer-based systems in the 1970s.

The 1980s and 1990s brought further modernization, including:

- Secure, private telecommunications networks

- Advanced, automated processing systems

Today, Fedwire operates as a highly secure, high-speed, computerized platform with:

- Robust disaster recovery systems

- Advanced cybersecurity measures

- The capacity to process trillions of dollars in payments daily

Fedwire’s evolution underscores the Federal Reserve’s commitment to maintaining a resilient, modernized payment infrastructure that adapts to changing technology and financial needs.

How Does Fedwire Work?

The Fedwire system operates through a central network, which is operated and monitored by the Federal Reserve. Here is a more detailed look at the step-by-step process:

- Message initiation: A financial institution creates a funds transfer message through its connection to Fedwire, specifying the sending and receiving institutions, amount, and purpose of the transaction.

- Transmission: The financial institution securely transmits the message through a dedicated communication network to the Federal Reserve.

- Authentication and validation: Fedwire verifies the identity of the sender and ensures that the sending institution has sufficient funds in its reserve account at the Federal Reserve.

- Settlement: Upon successful validation, the Federal Reserve debits the sending institution’s reserve account and credits the receiving institution’s reserve account — this is final and irrevocable.

- Confirmation: Fedwire sends both banks a settlement confirmation, typically within seconds of receiving the original request.

Because Fedwire operates on a real-time gross settlement basis, each transaction is settled individually rather than being netted with other transactions. This eliminates settlement risk and ensures the immediate availability of funds, supporting critical functions such as liquidity management and monetary policy.

Participants in the Fedwire System

The Federal Reserve designed Fedwire for institutions that hold accounts directly with the Federal Reserve. Participants include:

- Commercial banks: The largest group of users, settling interbank transactions and customer payments.

- Savings banks and credit unions: Handling High-Value Member Transfers.

- Government agencies: Disbursing federal funds or collecting taxes.

- International banking organizations: Managing cross-border flows involving U.S. dollar transactions.

- Clearinghouses: Settling securities trades or other market activities.

These institutions often act on behalf of their customers — businesses, organizations, or individuals — who may need to send large, time-sensitive payments. However, an individual cannot directly use Fedwire; they must go through their bank.

This participant structure helps the Federal Reserve manage risk while ensuring that only regulated, supervised financial institutions can access the powerful Fedwire network.

Types of Fedwire Services

Fedwire consists of two primary services, each with specific purposes and protocols:

1. Fedwire Funds Service

- Handles transfers of cash balances between financial institutions.

- Supports payments for corporate transactions, interbank loans, Federal Reserve monetary operations, and government transfers.

- Processes millions of payments totaling trillions of dollars every day.

2. Fedwire Securities Service

- Provides safekeeping and settlement for U.S. Treasury securities and securities issued by government-sponsored enterprises.

- Fedwire ensures that payment is confirmed before exchanging securities, enabling delivery-versus-payment (DvP) settlement and reducing counterparty risk.

- Plays a crucial role in the stability and efficiency of U.S. financial markets.

By offering both funds and securities settlement, Fedwire helps integrate various components of the U.S. financial system into a seamless and secure ecosystem.

Features of Fedwire

Features of Fedwire are:

- Speed: Transactions settle within seconds, supporting time-critical obligations like margin calls or securities settlements.

- Finality: Payments are legally final once processed, reducing legal and settlement risks.

- Certainty: Participants know exactly when funds have moved, improving cash and liquidity management.

- Security: operated under strict Federal Reserve oversight with advanced cybersecurity controls.

- High capacity: can process enormous transaction volumes without delays or bottlenecks.

- Risk reduction: Real-time gross settlement minimizes systemic risk compared to net settlement systems.

- Liquidity support: Enables banks to reallocate funds during market stress or liquidity shortages quickly.

For these reasons, Fedwire is indispensable for both normal economic activity and crisis management in the financial sector.

Security Measures

Fedwire is designated as a Systemically Important Financial Market Utility (SIFMU), meaning its failure could have a severe impact on the U.S. economy. As a result, it has world-class security protections, including:

- Multi-factor authentication to prevent unauthorized access.

- End-to-end data encryption to protect sensitive transaction data.

- Secure telecommunications using private networks rather than the open internet.

- Strict participant vetting to ensure only supervised financial institutions can connect.

- Resilience planning through redundant systems, backup data centers, and emergency procedures.

- Real-time monitoring to detect fraud or cybersecurity threats as they happen.

Additionally, the Federal Reserve regularly conducts simulations and stress tests to ensure Fedwire can continue operating even during cyberattacks, natural disasters, or market panics.

Operating Hours

Fedwire Funds Service generally operates Monday through Friday from 9:00 p.m. Eastern Time on the previous calendar day until 7:00 p.m. Eastern Time on the business day itself. The final half-hour (6:30 p.m. to 7:00 p.m.) is a closing window to reconcile and settle any remaining messages.

This extended window of operation — nearly 22 hours a day — ensures that financial institutions across all U.S. time zones, as well as in some international locations, can access Fedwire when needed. These hours are especially valuable for managing liquidity around market open and close times or during times of economic stress when payment volumes surge.

Fedwire vs. CHIPS

Many people compare Fedwire to CHIPS (Clearing House Interbank Payments System), but these systems serve slightly different purposes. Here is a deeper comparison:

| Aspect | Fedwire | CHIPS |

| Operator | Federal Reserve Banks | The Clearing House |

| Settlement | Real-time gross settlement | Net settlement at end of day |

| Finality | Immediate, irrevocable | Final at the end of the day after netting |

| Participants | Primarily financial institutions with Fed accounts | Primarily large commercial banks |

| Risk Profile | Virtually no settlement risk due to immediate finality | Some risk due to intra-day exposure before netting |

| Typical Uses | Government, interbank, securities settlement | Corporate commercial payments between large banks |

In practice, many large banks use both Fedwire and CHIPS, depending on the type of payment, timing requirements, and risk considerations.

The Role of Fedwire in the U.S. Financial System

Fedwire is at the heart of America’s financial plumbing. It supports critical functions such as:

- Liquidity distribution among financial institutions

- Monetary policy implementation through Federal Reserve operations

- Settlement of large-value securities trades

- Government disbursements and collections

- Market confidence by providing a predictable, resilient settlement backbone.

In times of financial stress, such as during the 2008 financial crisis or the 2020 pandemic, Fedwire ensured the uninterrupted flow of high-value payments and provided an essential mechanism for distributing emergency liquidity. Without Fedwire, interbank credit would seize up, securities markets could fail to settle trades, and the economic consequences would be catastrophic.

Recent Developments and the Future of Fedwire

To keep up with modern payment needs, the Federal Reserve has been continuously enhancing Fedwire. Recent efforts include:

- Migrating to ISO 20022, a modern financial messaging standard that improves data richness, consistency, and cross-border compatibility.

- Enhancing cybersecurity through layered defenses, penetration testing, and tighter supervision of participants’ cybersecurity hygiene.

- Expanding resilience with advanced backup sites, additional contingency plans, and more frequent disaster recovery drills.

- Collaborating with emerging instant payment networks like FedNow® to ensure large-value (Fedwire) and small-value (FedNow) payments can coexist and complement each other.

The Federal Reserve designed FedNow for instant payments to consumers and small businesses. At the same time, it will continue to operate Fedwire as the dominant platform for large, mission-critical transactions in the financial system for the foreseeable future.

Final Thoughts

In summary, Fedwire serves as the mission-critical backbone of the U.S. financial ecosystem. Its real-time gross settlement capabilities, security features, and finality of payment make it essential for maintaining trust and efficiency in financial markets. Every day, trillions of dollars move across its wires to keep the nation’s economy running, from securities trades to interbank loans to government disbursements.

As financial technology evolves, Fedwire will continue to adapt, ensuring it meets the growing demands of a faster, more interconnected global economy while remaining a pillar of financial stability in the United States.

Frequently Asked Questions (FAQs)

Q1. Is there a dollar limit on Fedwire transfers?

Answer: No, Fedwire does not impose a maximum dollar limit on transfers. “Because the Federal Reserve designed Fedwire for high-value transactions, it processes payments worth millions or even billions of dollars.

Q2. Can Fedwire be reversed if a mistake is made?

Answer: No. The Federal Reserve makes a Fedwire transaction final and irrevocable once it settles. However, the sending institution may request the recipient’s cooperation in voluntarily returning funds if an error occurs, but there is no guarantee of recovery.

Q3. How is Fedwire different from SWIFT?

Answer: SWIFT is a messaging network for sending payment instructions internationally, but it does not settle payments. Fedwire, by contrast, both transmits instructions and settles payments in U.S. dollars within the Federal Reserve’s accounts.

Q4. How does Fedwire handle errors or disputes?

Answer: Fedwire’s settlement is final, so errors must generally be resolved by the sending and receiving banks after the fact. The Federal Reserve provides operational support, but it does not mediate disputes between commercial parties.

Q5. Does Fedwire support cryptocurrency transfers?

Answer: No, Fedwire only supports transfers of U.S. dollars or U.S. dollar-denominated securities between institutions holding Federal Reserve accounts. Payment networks settle cryptocurrency transactions outside of the Federal Reserve system.

Recommended Articles

We hope this guide on Fedwire has been clear and informative. For more expert-backed insights on financial infrastructure and secure payment systems, explore these related articles: