Updated July 13, 2023

What is a Debt Collector?

The term “debt collector” refers to an agency engaged in recovering debt that is either past due or in default. Typically, the debt collectors are hired by the creditors whose money is stuck in delinquent accounts.

These debtor collectors operate either for a pre-determined fee or a certain percentage of the debt recovered. Some debt collectors purchase the delinquent accounts at a discount to their original value and then try to recover the total amount of the debt. Thus, debt collectors are also popularly known as collection agencies.

Key Takeaways

Some of the key takeaways of the article are:

- A debt collector is an entity recovering past due or default debts.

- It is typically paid a certain percentage of the amount of debt they recover.

- Debt collectors, who purchase delinquent accounts at a discount and independently recover the amounts, are responsible for the collection process.

- Strict regulations govern debt collectors’ actions, ensuring debtors’ protection from abusive collection agencies.

How Does a Debt Collector work?

The process of debt collection might vary based on the debt collector. Although many agencies resort to harmful, illegal practices for recovering debt, most agencies adhere to the prescribed regulations and professionally retrieve money from delinquent accounts.

Initially, they send letters to the borrower’s address as provided to the creditor. Otherwise, the agency can also call the borrower to recover the debt. Whether through letters or telephonic calls, the debt collector must provide specific details about the debt, such as the original creditor’s name and the total amount outstanding, including late fees & other charges. The agency offers the borrower a certain period (say 30 days) to dispute the debt claim in writing. If the borrower does not deny the claim within the specified time frame, the agency considers the debt valid and begins contacting the borrower for collection.

When debt collectors follow the regulations diligently and work within the statute of limitations, they seldom resort to unlawful practices, and the borrowers don’t feel harassed or threatened.

Types of Debt Collector

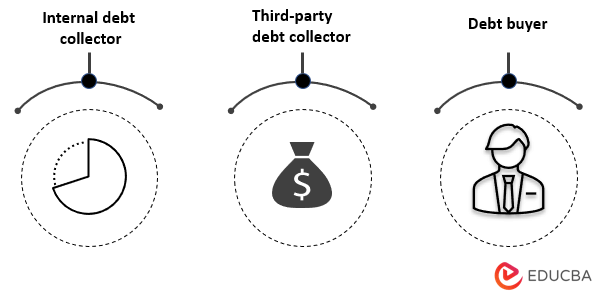

There are three major types:

1. Internal Debt Collector

An internal debt collector (also known as a first-party debt collector) is usually a sub-unit of the creditor entity. The debt recovery task is assigned to the sub-unit internally rather than hiring outside parties. The selection of an internal debt collection team depends mainly on the company policies, such as type of debt, period of overdue, etc.

2. Third-Party Debt Collector

Creditors enlist third-party debt collectors to recover outstanding debts when company policies or internal teams cannot do so. These agencies typically receive payment based on a certain percentage of the amount of debt they recover, which implies that they do not receive any fees if they cannot recover the debt. Given that these debt collectors are external to the creditors, they don’t represent the creditors and thus may be less customer-friendly to the borrowers.

3. Debt Buyer

If internal and external debt collection efforts don’t yield meaningful results, the creditors may file a lawsuit against the debtors or sell the debt to some debt buyers. These debt collectors purchase the delinquent accounts at a discount to their original value and then attempt to recover the total amount of the debt. The difference between the purchase price and the recovered amount is their profit.

Regulation of Debt Collector

The Federal Trade Commission (FTC) governs the actions of debt collectors through the Fair Debt Collection Practices Act (FDCPA), which prohibits debt collectors from employing unfair, abusive, or misleading practices during the collection process. For instance, the debt collectors can only contact the debtors between 8:00 AM to 9:00 PM on weekdays. Further, they can’t resort to false claims to pressure the debtors or physically harm and threaten them. They can only seize a debtor’s assets after winning a lawsuit against them.

The debtors must know their rights. The debtor can send a cease and desist letter to a debt collector if the debt collector repeatedly contacts them within a short period, as the FDCPA regulations consider it harassment. If the debt collector continues to harass even after receiving the cease and desist letter, the debtor can report the issue to the Consumer Financial Protection Bureau (CFPB).

Who can Debt Collector Contact?

A debt collector can contact the borrower’s relatives, employer, friends, or neighbors to retrieve the borrower’s telephone number or address. However, the restrictions are relieved if:

- the contacted person is the guarantor or co-borrower of the loan

- the employer is contacted to confirm the borrower’s employment

- the borrower gave consent to contact the person

In case of oral confirmation by the borrower, he/ she should receive written verification of the consent either on paper or electronically.

Conclusion

So, it can be seen that the work of debt collectors is challenging and requires strong experience in recovery. Typically, when a creditor fails to recover its loans, it assigns the recovery to an internal team, hires an external agency, or sells the loans to a debt buyer. A debt collector starts their work by ensuring the genuineness of the debt and then carries out an independent analysis before jumping into the collection process.

Recommended Articles

This is a guide to the Debt Collector. Here we also discuss the definition, How it works, with types and key takeaways. You may also have a look at the following articles to learn more –