What is Yield to Worst (YTW)?

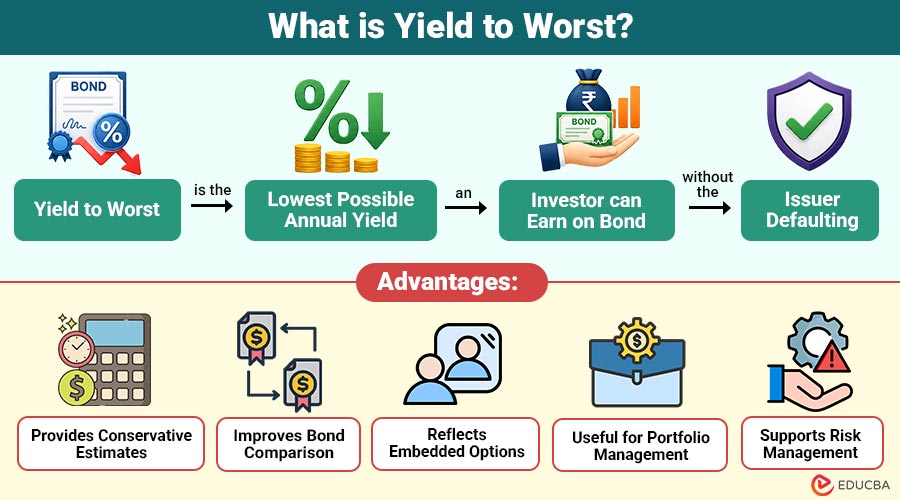

Yield to Worst is the lowest possible annual yield an investor can earn on bond without the issuer defaulting. It considers all possible redemption scenarios, such as early call dates, put options, or maturity, and identifies the minimum yield among them.

In simple words, Yield to Worst tells investors the minimum expected return they may receive if the bond is redeemed under the least favorable terms allowed in the bond agreement. It is widely used for callable, putable, and sinking-fund bonds, in which the bond may not remain outstanding until maturity.

For conservative investors, YTW serves as a risk assessment tool because it estimates the worst-case return while assuming the issuer fulfills all contractual obligations.

Table of Contents:

- Meaning

- Importance

- Formula

- Working

- Advantages

- Disadvantages

- Difference

- Applications

- Factors Affecting Yield to Worst

- Example

- Who Uses It?

Key Takeaways

- Yield to Worst is the lowest annual yield an investor can earn without issuer default.

- It considers Yield to Maturity, Yield to Call, Yield to Put, and other redemption scenarios.

- It is especially useful for callable and putable bonds.

- It helps investors evaluate downside risk before investing.

Importance of Yield to Worst

It provides a realistic estimate of bond returns under unfavorable yet contractually permitted scenarios. Its importance includes the following:

1. Conservative Return Estimate

Provides the lowest expected return, preventing investors from overestimating potential bond income under adverse scenarios.

2. Better Risk Assessment

Helps investors evaluate the minimum possible yield and understand potential risks before purchasing callable bonds.

3. Helps Compare Callable Bonds

Enables fair comparison between callable bonds by considering their lowest possible returns under redemption provisions.

4. Supports Investment Decisions

Assists portfolio managers in selecting fixed-income investments based on conservative yield expectations and associated risks.

5. Protects Against Reinvestment Risk

Reflects the risk of early bond redemption, helping investors prepare to reinvest proceeds at potentially lower interest rates.

Formula of Yield to Worst

It is calculated by determining the yield for every possible redemption date and selecting the lowest value.

Where:

- Yield to Maturity (YTM): Annual return if the bond is held until maturity.

- Yield to Call (YTC): Annual return if the issuer calls the bond before maturity.

- Yield to Put (YTP): Annual return if the investor exercises the put option.

- Yield to Sink (YTS): Annual return considering sinking fund repayments.

The smallest yield among these becomes the yield to worst.

How Does Yield to Worst Work?

It helps investors estimate the minimum return they can receive under different redemption possibilities.

The process works as follows:

Step 1: Identify Embedded Options

Determine whether the bond includes:

- Call option

- Put option

- Sinking fund provision

- Scheduled maturity

Step 2: Calculate Yield for Each Scenario

Calculate:

- Yield to Maturity

- Yield to Call

- Yield to Put (if applicable)

- Yield to Sink (if applicable)

Step 3: Compare All Yields

List every calculated yield.

Example:

- Yield to Maturity = 6.10%

- Yield to Call = 5.30%

- Yield to Put = 5.80%

Step 4: Select the Lowest Yield

The minimum yield becomes the yield to worst.

Yield to Worst = 5.30%

This represents the lowest annual return the investor can receive if the issuer acts according to the bond terms without defaulting.

Advantages of Yield to Worst

The key advantages are as follows.

1. Provides Conservative Estimates

Provides the minimum expected return, helping investors set realistic expectations before purchasing bonds with embedded options.

2. Improves Bond Comparison

Enables consistent comparison of bonds by evaluating their lowest possible yields under contractual redemption scenarios.

3. Reflects Embedded Options

Accounts for call and put provisions, providing a more accurate yield than coupon rates alone.

4. Useful for Portfolio Management

Helps portfolio managers analyze fixed-income investments with conservative yield assumptions to improve investment decisions.

5. Supports Risk Management

Identifies bonds with lower potential returns, enabling investors to manage downside risk more effectively in portfolios.

Disadvantages of Yield to Worst

Despite its usefulness, it has certain disadvantages that investors should consider before making bond investment decisions.

1. May Underestimate Actual Returns

May underestimate returns because issuers might not redeem bonds early, allowing investors to earn higher yields.

2. Requires Complex Calculations

Calculating yields across multiple redemption dates often requires financial calculators, spreadsheets, or specialized investment software.

3. Does Not Predict Issuer Behavior

Assumes issuers choose the least favorable redemption options, though actual decisions may differ based on market conditions.

4. Ignores Default Risk

It assumes issuers continue to make payments, without considering the possibility of a bond default or missed obligations.

5. Sensitive to Interest Rates

Changes in market interest rates can significantly influence yield-to-worst calculations and investment value assessments.

Difference Between Yield to Worst and Yield to Maturity

The table below highlights the key differences between the two.

| Basis | Yield to Worst | Yield to Maturity |

| Definition | Lowest possible yield without default | Yield if held until maturity |

| Considers Call Option | Yes | No |

| Considers Put Option | Yes | No |

| Considers Sinking Fund | Yes | No |

| Investor Perspective | Conservative | Standard |

| Return Estimate | Minimum possible | Expected if held until maturity |

| Best Used For | Callable and putable bonds | Traditional bonds |

Applications of Yield to Worst

It is commonly used in various fixed-income investment decisions.

1. Bond Investment Analysis

Investors evaluate minimum potential returns before purchasing callable or redeemable bonds with embedded options.

2. Mutual Funds

Bond fund managers analyze portfolio yields and make informed investment decisions.

3. Pension Funds

Pension funds estimate conservative bond income to support long-term retirement payment planning and obligations.

4. Insurance Companies

Insurance companies assess conservative bond returns while effectively managing long-term liabilities and investment risk.

5. Credit Risk Evaluation

Financial analysts combine conservative yield estimates with credit ratings to assess bond risk comprehensively.

Factors Affecting Yield to Worst

Several factors influence yield-to-worst calculations.

1. Interest Rates

Lower market interest rates increase the likelihood of early bond redemption, reducing potential investor returns.

2. Bond Price

Premium-priced bonds often generate lower returns because early redemption becomes more likely for issuers.

3. Coupon Rate

Higher coupon rates encourage issuers to refinance debt, increasing the probability of early bond redemption.

4. Call Provisions

Earlier call dates reduce it by shortening the bond’s expected investment holding period.

5. Market Conditions

Economic and market conditions influence issuer refinancing decisions, directly affecting yield-to-worst calculations and outcomes.

Example

Suppose an investor purchases a callable corporate bond with the following details:

| Particular | Value |

| Face Value | $1,000 |

| Coupon Rate | 7% |

| Market Price | $1,080 |

| Maturity | 10 years |

| First Call Date | After 5 years |

| Call Price | $1,030 |

After Calculations:

- Yield to Maturity = 6.05%

- Yield to Call = 4.92%

Since the issuer is likely to call the bond when interest rates decline, investors should consider the lower yield. Therefore,

Yield to Worst = 4.92%

Although the bond advertises a 7% coupon, the investor should expect a minimum annual return of only 4.92% if the issuer exercises the call option.

Who Uses It?

Yield to the worst is widely used by:

1. Individual Bond Investors

Individual bond investors evaluate minimum expected returns before purchasing callable or putable fixed-income securities.

2. Portfolio Managers

Portfolio managers use conservative yield estimates for bond selection and effective portfolio risk management.

3. Mutual Fund Companies

Mutual fund companies analyze portfolio yields using conservative return estimates for fixed-income investment strategies.

4. Pension Funds

Pension funds estimate minimum bond returns to support long-term retirement income planning and financial stability.

5. Insurance Companies

Insurance companies assess conservative bond yields to manage liabilities and maintain stable investment portfolios.

6. Investment Advisors

Investment advisors recommend bonds after carefully evaluating minimum expected returns and potential downside risks.

Final Thoughts

Yield to worst is an essential metric for evaluating the most conservative return a bond investment may generate under contractual redemption terms. Considering every possible redemption scenario helps investors measure downside risk, compare bonds more effectively, and make informed fixed-income investment decisions while maintaining realistic return expectations and stronger portfolio risk management.

Frequently Asked Questions (FAQs)

Q1. Does Yield to Worst change over time?

Answer: Yes, it changes with bond prices, interest rates, and redemption dates.

Q2. Is Yield to Worst relevant for all bonds?

Answer: No, it is mainly used for bonds with embedded options, such as callable or the putable bonds.

Q3. Should Yield to Worst be the only investment criterion?

Answer: No, investors should also consider credit quality, maturity, and overall risk.

Recommended Articles

We hope that this EDUCBA information on “Yield to Worst” was beneficial to you. You can view EDUCBA’s recommended articles for more information.