What is a Credit Default Swap?

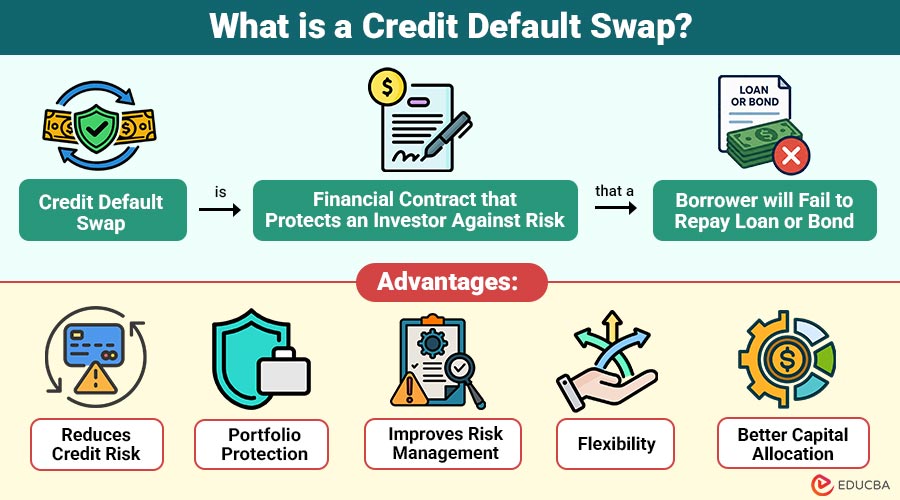

A credit default swap (CDS) is financial contract that protects an investor against the risk that a borrower will fail to repay loan or bond. It works like debt insurance. The buyer of the CDS pays regular premiums to the seller. In return, the seller agrees to compensate buyer if the borrower defaults or experiences another specified credit event.

In simple words, a credit default swap transfers the credit risk of loan or bond from one party to another without transferring ownership of the underlying debt.

For example, suppose a bank owns a $5 million corporate bond issued by Company XYZ. To protect itself against the possibility of XYZ defaulting, the bank purchases a CDS from an insurance company. The bank pays an annual premium, and if XYZ defaults, the insurance company compensates the bank for the agreed amount.

Table of Contents:

- Meaning

- Key Features

- Working

- Example

- Types

- Advantages

- Disadvantages

- Applications

- Risks Associated with Credit Default Swaps

- Who Uses Credit Default Swaps?

Key Takeaways:

- Credit default swaps transfer the risk of borrower default from protection buyers to protection sellers through premium payments.

- Contracts help investors hedge credit exposure while improving overall portfolio risk management and financial stability.

- Protection sellers compensate buyers when predefined credit events occur under agreed contractual terms and conditions.

- It offers valuable protection but involves counterparty, liquidity, pricing, and market-related risks.

Key Features of Credit Default Swap

Some important features of credit default swaps include:

1. Protection Against Default

A credit default swap protects investors against losses if the borrower fails to repay debt or experiences a credit event.

2. Based on Debt Instruments

Credit default swaps are linked to bonds, loans, or other debt instruments whose credit risk is being transferred.

3. Regular Premium Payments

The protection buyer pays periodic premiums to the seller throughout the contract in exchange for default protection coverage.

4. Default Compensation

If credit event occurs, the protection seller compensates the buyer in accordance with the agreed contract terms and conditions.

5. Fixed Contract Term

Every credit default swap has a predetermined maturity date, after which the protection agreement automatically expires unless renewed.

6. Transfers Credit Risk

A CDS transfers the risk of borrower default while allowing the original owner to retain ownership of the debt.

7. Used for Hedging and Speculation

Investors use credit default swaps to reduce credit exposure or speculate on changes in a borrower’s creditworthiness.

How Does a Credit Default Swap Work?

The basic working process involves the following steps:

Step 1: Purchase of Debt

An investor purchases bonds or loans issued by a company or government.

Step 2: Buy a CDS Contract

To reduce risk of default, the investor purchases a credit default swap from another financial institution.

Step 3: Premium Payments

The CDS buyer pays periodic premiums, known as the CDS spread, throughout the contract period.

Step 4: No Default

If the borrower continues to make payments and no credit event occurs, the seller retains the premiums until the contract expires.

Step 5: Credit Event Occurs

If the borrower defaults, files for bankruptcy, or experiences another defined credit event, the CDS seller compensates the buyer for the agreed-upon amount.

Example of a Credit Default Swap

The following example shows how it works in practice.

Suppose ABC Bank purchases corporate bonds worth $10 million issued by XYZ Corporation.

To protect itself from default risk, ABC Bank buys a five-year credit default swap from Insurance Company PQR.

- Bond value: $10 million

- Annual CDS premium: 2%

- Annual premium payment: $200,000

Scenario 1: No Default

XYZ Corporation successfully repays all obligations over the five years.

- ABC Bank receives interest from the bonds.

- Insurance Company PQR keeps the premium payments.

- No compensation is required.

Scenario 2: Default

After three years, XYZ Corporation failed to repay its debt.

- ABC Bank files a claim under the CDS agreement.

- Insurance Company PQR compensates ABC Bank in accordance with the contract.

- The loss from the bond default is significantly reduced.

Types of Credit Default Swaps

They are available in different forms depending on the type and number of borrowers covered. The main types include:

1. Single-Name CDS

A single-name credit default swap provides protection only against the default of a specific company, bank, or government debt issuer.

2. Basket Credit Default Swap

A basket credit default swap covers multiple borrowers in a single contract, spreading credit risk across selected debt issuers.

3. Index Credit Default Swap

An index credit default swap protects against defaults affecting an entire credit index containing multiple debt issuers.

4. Sovereign Credit Default Swap

A sovereign credit default swap protects investors against losses if a government fails to meet its debt repayment obligations.

Advantages of Credit Default Swaps

They offer several advantages by helping investors manage credit risk, protect investments, and improve portfolio flexibility. Some of the key advantages are the following:

1. Reduces Credit Risk

Investors can transfer default risk to another party, protecting their investment portfolio.

2. Portfolio Protection

Banks and institutional investors use CDS contracts to safeguard large bond holdings against unexpected defaults.

3. Improves Risk Management

Organizations can better manage credit exposure without selling the underlying debt securities.

4. Flexibility

CDS contracts can be customized to suit different borrowers, maturities, and risk levels.

5. Better Capital Allocation

Financial institutions can reduce risk exposure while continuing to invest in income-generating assets.

Disadvantages of Credit Default Swaps

While it provide valuable protection against credit risk, they also involve certain limitations and risks. Some of the major disadvantages include:

1. Counterparty Risk

If the CDS seller cannot fulfill its obligation, the buyer may still face financial losses.

2. Complex Contracts

Understanding CDS pricing, settlement methods, and credit events requires specialized financial knowledge.

3. High Costs

Premium payments can become expensive when the borrower’s credit quality deteriorates.

4. Speculative Trading

Some investors purchase CDS contracts without owning the underlying debt, increasing market speculation.

5. Liquidity Risk

Certain CDS contracts may be difficult to trade during periods of financial market stress.

6. Systemic Risk

Large-scale CDS exposures can increase financial instability if major market participants fail simultaneously.

Applications of Credit Default Swaps

They are widely used across the financial industry.

1. Banking

Banks use it to hedge risks associated with corporate and commercial lending activities.

2. Investment Management

Asset managers protect bond portfolios against potential borrower defaults using credit default swap contracts.

3. Insurance Companies

Insurance companies sell CDS contracts to earn premiums while managing overall credit risk exposure.

4. Corporate Risk Management

Companies use CDS contracts to reduce credit risk associated with investments, lending, and financial transactions.

5. Sovereign Debt Protection

Investors hedge against possible government debt defaults by purchasing sovereign protection.

6. Credit Market Analysis

Analysts study CDS spreads to evaluate borrower creditworthiness and overall market risk sentiment.

Risks Associated with Credit Default Swaps

Although CDS contracts reduce credit risk, they introduce additional risks.

1. Counterparty Default Risk

The protection seller may fail to fulfill its payment obligations upon a credit event under the contract.

2. Market Volatility

Rapid market changes can significantly affect CDS prices, increasing uncertainty and potential trading losses for investors.

3. Regulatory Changes

New financial regulations may alter trading practices, compliance requirements, and the overall cost of CDS transactions.

4. Incorrect Pricing

Improper valuation of credit risk may result in inaccurate pricing and unexpected financial losses for participants.

5. Liquidity Challenges

Some CDS contracts may have limited buyers and sellers, making them difficult to trade at fair prices.

6. Legal and Documentation Risks

Unclear contract terms or documentation errors may lead to disputes during settlement after a credit event.

Who Uses?

Credit default swaps are mainly used by:

1. Commercial Banks

Use CDS contracts to reduce credit risk from loans and other lending activities.

2. Investment Banks

Trade and structure CDS contracts for hedging, market-making, and client investment strategies.

3. Hedge Funds

Use CDS contracts to speculate on credit movements or hedge investment portfolio risks.

4. Mutual Funds

Protect bond investments against potential borrower defaults using credit default swap agreements.

5. Pension Funds

Manage long-term credit exposure and safeguard fixed-income investments through CDS protection.

6. Insurance Companies

Sell CDS contracts to earn premiums while managing overall credit risk exposure.

Final Thoughts

A Credit Default Swap (CDS) helps investors transfer credit risk by protecting against borrower defaults. While it improves portfolio protection and risk management, it also involves counterparty, liquidity, and market risks. Understanding CDS enables informed investment and effective credit risk management decisions.

Frequently Asked Questions (FAQs)

Q1. Who pays the premium in a credit default swap?

Answer: The protection buyer pays regular premiums, called the CDS spread, to the protection seller for the duration of the contract.

Q2. Can a credit default swap be terminated before maturity?

Answer: Yes. Depending on market conditions and contract terms, a CDS may be closed, transferred, or terminated before its maturity date.

Q3. How is the cost of a credit default swap determined?

Answer: The premium depends on factors such as the borrower’s credit quality, market conditions, contract duration, and the likelihood of default.

Q4. Are credit default swaps regulated?

Answer: Yes. In many countries, CDS trading is subject to financial regulations that promote transparency, reduce systemic risk, and improve market stability.

Recommended Articles

We hope that this EDUCBA information on “Credit Default Swap” was beneficial to you. You can view EDUCBA’s recommended articles for more information.