What are Perpetual Bonds?

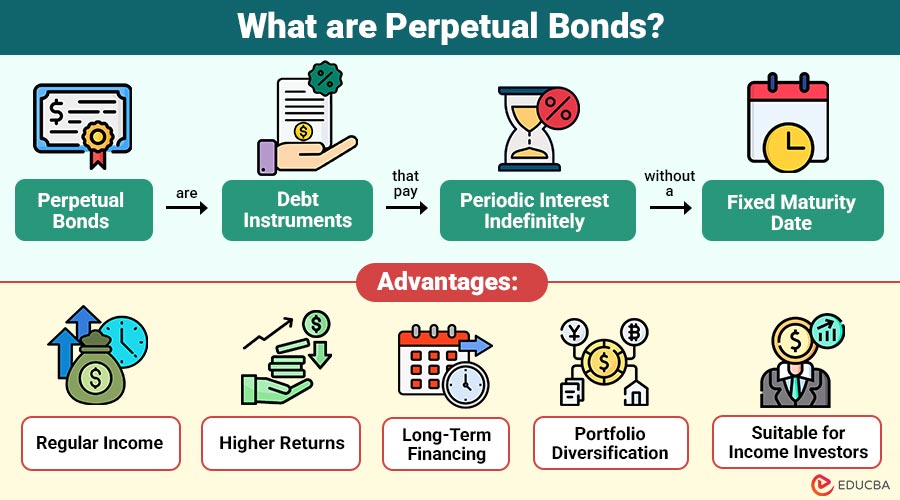

Perpetual bonds are debt instruments that pay periodic interest indefinitely without a fixed maturity date. Since there is no maturity, investors generally do not receive the principal unless the issuer exercises a call option to redeem the bond.

These bonds offer higher interest rates than conventional bonds to compensate investors for the absence of principal repayment. Financial institutions often issue perpetual bonds to strengthen their capital base and meet regulatory requirements.

For example, a bank issues a perpetual bond with a face value of $10,000 and a coupon rate of 7%. The investor receives $700 annually in interest. Since the bond has no maturity date, these payments continue indefinitely unless the issuer redeems the bond.

Table of Contents:

- Meaning

- Key Features

- Types

- Working

- Advantages

- Disadvantages

- Difference

- Applications

- Who Should Invest in Perpetual Bonds?

Key Takeaways:

- Perpetual bonds provide regular interest payments indefinitely without a fixed maturity date or principal repayment obligation.

- They offer higher coupon rates to compensate investors for greater long-term investment risks involved.

- Issuers may redeem callable perpetual bonds after specified periods if favorable market conditions arise later.

- It suits income-focused investors seeking steady cash flow and long-term portfolio diversification benefits.

Key Features of Perpetual Bonds

Below are the key features mentioned:

1. No Maturity Date

They have no fixed maturity date, allowing issuers to avoid repaying the principal at a predetermined time.

2. Regular Interest Payments

Investors receive fixed periodic interest payments for as long as the bond remains outstanding and is not redeemed.

3. Higher Coupon Rates

It generally offers higher coupon rates than traditional bonds to compensate investors for increased long-term investment risk.

4. Callable by the Issuer

Many perpetual bonds allow issuers to redeem them after a specified period under predefined terms and conditions.

5. Long-Term Capital Instrument

Governments and financial institutions issue perpetual bonds to raise long-term capital without fixed principal repayment obligations.

Types of Perpetual Bonds

It can be classified into following types:

1. Government Perpetual Bonds

Issued by governments to finance public expenditure without committing to repay the principal on a fixed maturity date.

2. Bank Perpetual Bonds

Issued by banks to strengthen regulatory capital, improve financial stability, and support long-term business growth.

3. Corporate Perpetual Bonds

Issued by companies to raise long-term capital without creating an obligation for fixed principal repayment.

4. Callable Perpetual Bonds

Allow issuers to redeem the securities after a specified date if market conditions become favorable.

How do Perpetual Bonds Work?

The following steps explain how it works:

Step 1: Bond Issuance

A government, bank, or company issues perpetual bonds to raise capital.

Step 2: Investor Purchase

Investors buy the bonds and provide funds to the issuer.

Step 3: Interest Payments

The issuer pays regular interest to investors based on the coupon rate.

Step 4: No Principal Repayment

Unlike traditional bonds, the principal is not repaid on a fixed maturity date.

Step 5: Optional Redemption

If the bond is callable, the issuer may redeem it after the specified call period.

Advantages of Perpetual Bonds

It offers several advantages to both issuers and investors.

1. Regular Income

It provides investors with consistent interest payments, creating a reliable source of long-term income over the life of the bond.

2. Higher Returns

These bonds generally offer higher coupon rates than traditional bonds, increasing potential returns for long-term income-focused investors.

3. Long-Term Financing

Issuers secure long-term funding without the obligation to repay the principal on a predetermined maturity date.

4. Portfolio Diversification

They diversify investment portfolios by adding a unique fixed-income asset with long-term income potential and stability.

5. Suitable for Income Investors

Income-focused investors benefit from regular coupon payments, making perpetual bonds suitable for generating steady cash flow over time.

Disadvantages of Perpetual Bonds

Despite their benefits, they also have certain disadvantages.

1. No Fixed Maturity

Investors may never recover their principal because perpetual bonds have no fixed maturity or repayment date.

2. Interest Rate Risk

Bond prices can decline significantly when market interest rates rise, reducing the investment’s overall market value.

3. Call Risk

Issuers may redeem perpetual bonds early when interest rates decline, limiting investors’ future interest income potential.

4. Credit Risk

Investors face potential losses if the issuer experiences financial difficulties and cannot continue making interest payments.

5. Inflation Risk

Inflation reduces purchasing power of future interest payments, lowering the real return earned by investors over time.

Difference Between Perpetual Bonds and Traditional Bonds

The table below highlights the key differences between both:

| Feature | Perpetual Bonds | Traditional Bonds |

| Maturity Date | No maturity | Fixed maturity date |

| Principal Repayment | Usually not repaid unless called | Repaid at maturity |

| Interest Payments | Continue indefinitely | Continue until maturity |

| Coupon Rate | Generally higher | Usually lower |

| Issuers | Governments, banks, corporations | Governments, corporations, municipalities |

Applications of Perpetual Bonds

They are commonly used in the following areas:

1. Banking and Financial Institutions

To strengthen capital reserves and meet regulatory capital requirements.

2. Government Financing

To fund long-term public projects without fixed principal repayment obligations.

3. Corporate Capital Raising

To raise long-term capital while avoiding fixed principal repayment schedules.

4. Infrastructure Funding

To finance large-scale infrastructure projects requiring long-term investment.

5. Long-Term Investment Portfolios

To generate steady income and diversify fixed-income investment portfolios.

Who Should Invest in Perpetual Bonds?

Perpetual bonds may be suitable for:

1. Income-Focused Investors

Investors seeking regular income through consistent periodic interest (coupon) payments.

2. Retirees Seeking Regular Cash Flow

Retirees who need a dependable stream of interest income to support their living expenses.

3. Long-Term Investors

Investors with a long investment horizon who prioritize stable income over principal repayment.

4. Investors Comfortable with Moderate Risk

Investors comfortable with interest rate, credit, and call risks in exchange for potentially higher yields.

5. Portfolio Diversification Seekers

Investors looking to diversify their fixed-income portfolio and reduce overall portfolio concentration risk.

Final Thoughts

Perpetual bonds are long-term debt securities that provide continuous interest payments without a fixed maturity date. They offer higher income potential than many traditional bonds while helping issuers raise permanent capital. However, investors should also consider risks such as interest rate changes, inflation, credit risk, and the possibility of the bond being called. Evaluating these factors carefully can help determine whether they are an appropriate addition to an investment portfolio.

Frequently Asked Questions (FAQs)

Q1. Do perpetual bonds repay the principal?

Answer: Generally, no. The principal is repaid only if the issuer exercises a call option or redeems the bond.

Q2. Why do perpetual bonds offer higher interest rates?

Answer: They offer higher coupon rates to compensate investors for lack of a maturity date and greater investment risk.

Q3. Are perpetual bonds risky?

Answer: Yes. They are exposed to credit risk, interest rate risk, inflation risk, and call risk, making them riskier than many traditional bonds.

Recommended Articles

We hope that this EDUCBA information on “Perpetual Bonds” was beneficial to you. You can view EDUCBA’s recommended articles for more information.