What is Overcollateralization?

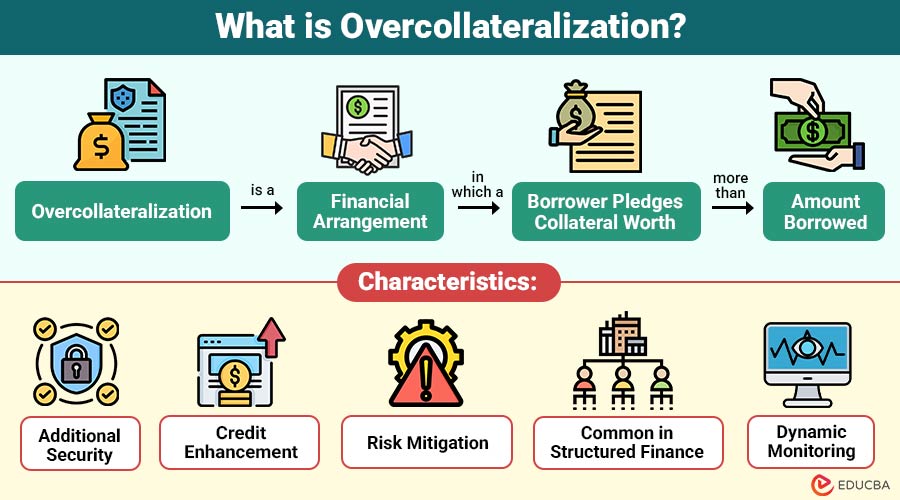

Overcollateralization is a financial arrangement in which a borrower pledges collateral worth more than amount borrowed. The excess collateral acts as additional protection for the lender against potential losses arising from default, market volatility, or declining asset values.

For example, if a borrower obtains a $100,000 loan and pledges $130,000 in collateral, the loan is overcollateralized by $30,000, or 30%.

Table of Contents:

- Meaning

- Importance

- Working

- Characteristics

- Types

- Benefits

- Disadvantages

- Difference

- Real-World Examples

Key Takeaways:

- Overcollateralization occurs when the collateral value exceeds the debt it secures.

- It provides lenders and investors with additional protection against default risk.

- The technique is widely used in lending, securitization, mortgage-backed securities, and DeFi platforms.

- Proper monitoring and risk management are essential to maintaining effective overcollateralization levels.

Why is Overcollateralization Important?

Overcollateralization serves several important functions in financial markets.

1. Protects Lenders

Extra collateral provides financial protection against losses when borrowers fail to repay debts.

2. Improves Credit Ratings

Overcollateralization enhances security, often resulting in higher credit ratings for securities.

3. Enhances Investor Confidence

Additional collateral reassures investors by reducing perceived investment risk and uncertainty.

4. Supports High-Risk Borrowers

Borrowers with weaker credit profiles can access financing through additional collateral.

5. Reduces Default Risk

Higher collateral coverage improves lenders’ chances of recovery in the event of borrower default.

How Does Overcollateralization Work?

The process is relatively straightforward:

Step 1: Loan Request

A borrower applies for financing from a lender.

Step 2: Collateral Assessment

The lender evaluates the value of the assets offered as collateral, such as property, securities, cash, or digital assets.

Step 3: Determination of Collateral Ratio

The lender establishes a collateralization ratio that exceeds 100%.

Step 4: Loan Approval

The borrower receives funding while the lender obtains rights to the pledged collateral.

Step 5: Monitoring

The lender periodically reviews the collateral value to ensure it remains above required levels.

Step 6: Repayment or Liquidation

If borrower repays the loan, the collateral is released, and if the borrower defaults, the lender may sell the collateral to recover losses.

Characteristics of Overcollateralization

The following characteristics explain how overcollateralization enhances security, reduces risk, and strengthens the overall creditworthiness of financial arrangements.

1. Additional Security

The value of the collateral exceeds the amount of debt, providing extra protection for lenders.

2. Credit Enhancement

It improves the credit quality and reliability of loans, bonds, and other financial securities.

3. Risk Mitigation

Overcollateralization helps protect against borrower defaults and declines in collateral value.

4. Common in Structured Finance

It is widely used in securitization transactions, asset-backed securities, and other structured finance products.

5. Dynamic Monitoring

Lenders regularly monitor collateral values and may require additional collateral if asset values decrease.

Types of Overcollateralization

The following are the main types of overcollateralization commonly used across traditional and digital financial markets.

1. Loan-Based Overcollateralization

Occurs when borrowers pledge collateral that exceeds the loan amount to provide additional protection for the lender.

2. Asset-Backed Securities

It involves maintaining underlying assets exceeding the value of issued securities to enhance credit quality and investor protection.

3. Mortgage-Backed Securities

Uses mortgage assets that exceed security values to significantly reduce risk and strengthen investor confidence.

4. DeFi Overcollateralization

Cryptocurrency lending platforms commonly require borrowers to deposit crypto assets worth significantly more than the borrowed amount.

Benefits of Overcollateralization

The following benefits explain why overcollateralization is widely used in lending, securitization, and financial markets.

1. Lower Credit Risk

Excess collateral reduces lenders’ potential losses if borrowers default on their obligations.

2. Improved Loan Approval Chances

Additional collateral helps borrowers qualify for financing despite lower creditworthiness levels.

3. Better Borrowing Terms

Reduced lender risk may result in lower interest rates and favorable terms.

4. Higher Investor Protection

Strong collateral coverage provides investors with greater security against potential losses.

5. Increased Market Stability

Additional collateral helps absorb shocks and supports stability during financial stress.

Disadvantages of Overcollateralization

Despite its advantages, overcollateralization has disadvantages.

1. Capital Inefficiency

Borrowers must lock significantly more assets than the actual loan amount, reducing usable capital.

2. Reduced Liquidity

Pledged collateral cannot be easily accessed or used for other financial purposes or needs.

3. Opportunity Cost

Locked assets miss potential investment returns that could have been earned elsewhere in markets.

4. Collateral Value Declines

Market fluctuations can reduce collateral values, requiring borrowers to quickly deposit additional assets.

5. Liquidation Risk

If collateral falls below required levels, lenders may liquidate assets to recover outstanding debt.

Difference Between Overcollateralization and Collateralization

The table below highlights the key differences between overcollateralization and standard collateralization:

| Basis | Overcollateralization | Collateralization |

| Collateral Value | Exceeds loan value | Equals or closely matches the loan value |

| Risk for Lender | Lower | Moderate |

| Borrower Requirement | Higher | Lower |

| Credit Enhancement | Strong | Limited |

| Investor Protection | Greater | Standard |

| Common Usage | Structured finance, DeFi | Traditional lending |

Real-World Examples

The following examples demonstrate how overcollateralization is applied across traditional finance, securitized products, and cryptocurrency lending to reduce risk and enhance security.

1. Asset-Backed Security

A financial institution creates securities worth $500 million backed by loans totaling $550 million. The extra $50 million serves as a credit enhancement feature.

2. Cryptocurrency Lending

A crypto investor wants to borrow stablecoins worth $5,000. The lending platform requires $8,000 in cryptocurrency collateral. If the collateral value falls significantly, part of it may be liquidated automatically.

3. Business Financing

A manufacturing company borrows $1 million and pledges machinery valued at $1.4 million. The additional collateral improves lenders’ confidence and increases the likelihood of approval.

Final Thoughts

Overcollateralization is a powerful risk-management and credit-enhancement tool that strengthens the security of loans and financial products. By requiring collateral values that exceed debt obligations, lenders and investors gain additional protection against uncertainty, defaults, and market volatility. Although it can reduce capital efficiency for borrowers, its role in improving financial stability, facilitating lending, and enhancing investor confidence makes it a fundamental concept in modern finance.

Frequently Asked Questions (FAQs)

Q1. Why do lenders require overcollateralization?

Answer: Lenders use it to reduce losses from borrower defaults and declines in collateral value.

Q2. Is overcollateralization common in cryptocurrency lending?

Answer: Yes. Most DeFi lending platforms require borrowers to pledge crypto assets exceeding the loan amount because cryptocurrencies are highly volatile.

Q3. What happens if collateral value falls significantly?

Answer: The lender may request additional collateral, reduce borrowing limits, or liquidate collateral to recover the outstanding debt.

Q4. Is overcollateralization always necessary?

Answer: No. Its necessity depends on the borrower’s creditworthiness, the lender’s risk tolerance, market conditions, and the type of financing involved.

Recommended Articles

We hope that this EDUCBA information on “Overcollateralization” was beneficial to you. You can view EDUCBA’s recommended articles for more information.