What is 50/30/20 Budget Rule?

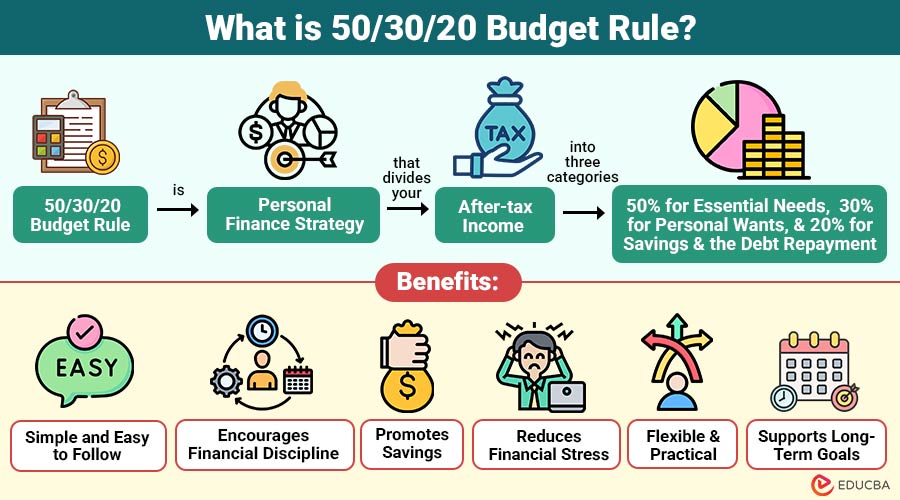

The 50/30/20 Budget Rule is personal finance strategy that divides your after-tax income into three categories: 50% for essential needs, 30% for personal wants, and 20% for savings and the debt repayment.

This method was popularized by U.S. Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan. The idea is to simplify budgeting so that people can maintain a balance between essential living expenses, lifestyle choices, and long-term financial goals. Instead of tracking every rupee in detail, you simply assign portions of your income to each category.

Table of Contents:

- Meaning

- Working

- Why is 50/30/20 Budget Rule Effective?

- Benefits

- Limitations

- How to Apply 50/30/20 Rule Effectively?

- Real-Life Scenario

- Who Should Use 50/30/20 Rule?

Key Takeaways:

- 50/30/20 rule simplifies budgeting by dividing income into needs, wants, and savings categories.

- This budgeting method encourages disciplined spending habits while promoting consistent, long-term growth in financial savings.

- Allocating twenty percent toward savings improves financial security, emergency preparedness, and future wealth creation.

- The rule offers flexibility, helping individuals balance essential expenses, lifestyle choices, and investment planning.

How Does 50/30/20 Budget Rule Work?

To apply this rule, you first calculate your monthly after-tax income (salary after deductions like income tax, PF, etc.). Then divide it as follows:

1. 50% – Needs (Essential Expenses)

Needs are the expenses required for basic living and survival. These include:

- Rent or home loan EMI

- Groceries

- Utility bills (electricity, water, gas)

- Transportation (fuel, public transport)

- Insurance premiums

- Basic healthcare and medicines

These are non-negotiable expenses. If your needs exceed 50%, you may need to reduce costs or adjust your lifestyle.

2. 30% – Wants (Lifestyle Expenses)

Wants are non-essential, but they improve your quality of life. They include:

- Dining out and food delivery

- Entertainment (movies, OTT subscriptions)

- Shopping for clothes and gadgets

- Travel and vacations

- Hobbies and leisure activities

These expenses are flexible and can be reduced during financial constraints.

3. 20% – Savings and Debt Repayment

This portion is crucial for financial security and future planning. It includes:

- Savings account deposits

- Emergency fund contributions

- Investments (mutual funds, stocks, SIPs)

- Retirement planning (PPF, NPS)

- Extra loan or credit card repayments

This category helps build long-term wealth and financial independence.

Why is 50/30/20 Budget Rule Effective?

The popularity of this budgeting method lies in its simplicity and practicality. Here is why it works:

1. Easy to Understand

Unlike complex budgeting systems, this rule is straightforward. Even beginners can apply it without financial expertise.

2. Encourages Financial Discipline

It creates a balance between spending and saving, helping you avoid overspending on non-essential items.

3. Flexible Approach

You can adjust percentages based on your income level, location, or financial goals.

4. Promotes Savings Habit

Automatically allocating 20% to savings ensures consistent wealth building.

5. Reduces Financial Stress

Having a clear structure removes confusion and helps you feel more in control of your money.

Benefits of the 50/30/20 Rule

50/30/20 rule offers several benefits that help individuals manage money effectively and build long-term financial stability.

1. Simple and Easy to Follow

The rule uses broad categories, making budgeting less complicated for beginners.

2. Encourages Financial Discipline

It helps individuals avoid overspending and maintain balanced finances.

3. Promotes Savings

Allocating 20% toward savings supports wealth creation and future security.

4. Reduces Financial Stress

A structured budget provides clarity and improves money management confidence.

5. Flexible and Practical

The method can be adjusted based on income levels and personal priorities.

6. Supports Long-Term Goals

It helps individuals prepare for retirement, emergencies, and major life expenses.

Limitations of the 50/30/20 Rule

While effective, the rule is not perfect for everyone. Some limitations include:

1. Not Suitable for Low-Income Earners

For individuals with lower incomes, essential expenses may exceed 50%, leaving less room for savings or discretionary spending.

2. High Cost of Living Areas

In cities with high rents and living costs, the “needs” category may exceed 50%.

3. Oversimplified Structure

Some people require more detailed budgeting to better track their finances.

4. Debt Situation Variations

If someone has significant debt, they may need to allocate more than 20% toward repayment.

How to Apply 50/30/20 Rule Effectively?

Here are key steps to successfully implement the 50/30/20 budgeting rule and manage your finances efficiently.

Step 1: Calculate Your Net Income

Calculate your monthly income after deductions and taxes.

Step 2: Categorize Your Expenses

List all expenses and divide them into needs, wants, and savings.

Step 3: Adjust Spending Habits

If you are overspending in one category, reduce expenses in another.

Step 4: Automate Savings

Configure automatic transfers to investment or savings accounts.

Step 5: Review Monthly

Track your spending every month and adjust as needed.

Real-Life Scenario

Here is a simple example of how the 50/30/20 rule can be applied in real-life financial planning.

Consider a young professional earning ₹80,000 per month:

- Needs (50%) = ₹40,000

- Wants (30%) = ₹24,000

- Savings (20%) = ₹16,000

With this structure:

- Rent, groceries, and bills are covered

- Lifestyle activities are maintained

- Investments and savings grow steadily

Over time, this leads to financial stability and wealth creation.

Who Should Use 50/30/20 Rule?

Here are the types of individuals who can benefit the most from using the 50/30/20 budgeting rule.

1. Students Starting Financial Planning

Students can manage expenses responsibly while developing strong saving and budgeting habits early in life.

2. Salaried Employees

Salaried employees can effectively balance spending, savings, and lifestyle needs using structured monthly budgeting techniques.

3. Freelancers with Stable Income

Freelancers with a stable income can successfully organize irregular earnings and maintain consistent financial discipline.

4. Individuals looking to save consistently

People wanting regular savings can allocate money efficiently toward future financial goals and emergencies.

5. Beginners in Personal Finance

Beginners can easily understand budgeting basics and improve their money management skills through simple financial planning.

Final Thoughts

50/30/20 budget rule is simple financial planning method that helps balance spending, saving, and lifestyle needs effectively. By consistently following this structured approach, individuals can improve money management, reduce financial stress, build savings, and achieve long-term financial stability and wealth growth through disciplined budgeting habits.

Frequently Asked Questions (FAQs)

Q1. Is 50/30/20 rule suitable for beginners?

Answer: Yes, it is one of the easiest budgeting methods for beginners because of its simple and flexible structure.

Q2. Can the percentages in 50/30/20 rule be adjusted?

Answer: Yes, individuals can modify the percentages depending on income level, financial goals, debt obligations, and living costs.

Q3. How does 50/30/20 rule help savings growth?

Answer: The rule encourages consistent saving habits by allocating twenty percent of monthly income toward savings and investments.

Recommended Articles

We hope that this EDUCBA information on “50/30/20 Budget Rule” was beneficial to you. You can view EDUCBA’s recommended articles for more information.