What is Invoice Factoring?

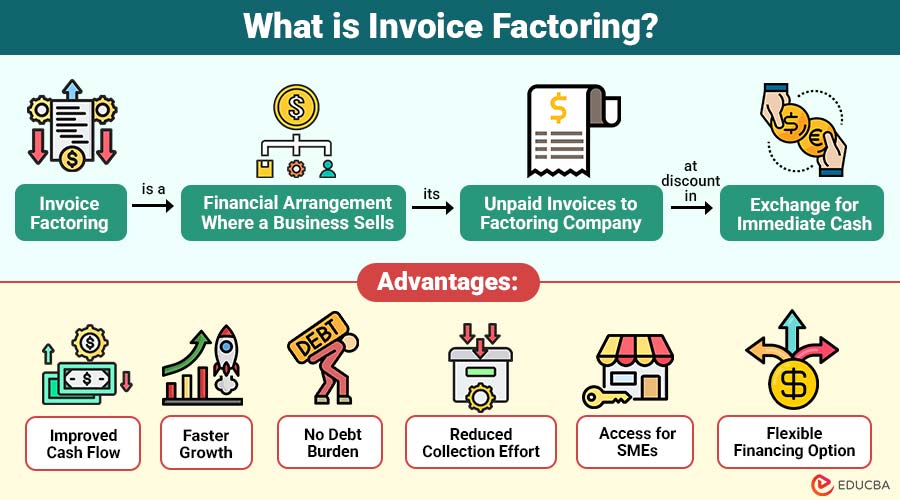

Invoice factoring is a financial arrangement where a business sells its unpaid invoices to factoring company at discount in exchange for immediate cash. Typically, the factor advances around 70% to 90% of the invoice value upfront. Once the customer pays invoice, the factor releases the remaining balance after deducting fees.

Table of Contents:

- Meaning

- Features

- Working

- Types

- Advantages

- Disadvantages

- Difference

- Real-World Example

- Use Cases

- When Should a Business Use Invoice Factoring?

- Limitations

Key Takeaways:

- Invoice factoring provides immediate cash by selling unpaid invoices, improving liquidity, and supporting operations.

- Factoring companies assess customer creditworthiness, reducing risk and ensuring predictable and reliable cash inflows.

- Invoice factoring is not a loan, so it avoids debt while offering financing options.

- Businesses consider costs, fees, and impact before choosing invoice factoring as a financing solution.

Features of Invoice Factoring

Here are the features that help businesses improve cash flow and financial flexibility:

- Immediate Cash Flow: Businesses receive immediate cash by factoring, improving liquidity and meeting operational expenses without waiting for customers to pay invoices.

- Credit Risk Assessment: Factoring companies assess customers’ creditworthiness to reduce risk, ensuring businesses partner with reliable buyers and maintain predictable cash inflows.

- No Collateral Required: Requires no collateral since funding is secured against receivables, making it accessible for small businesses with limited assets.

- Outsourced Collections: Factoring companies manage collections, which lessens the administrative load and frees up companies to concentrate on their core competencies rather than pursuing payments.

- Flexible Financing: Companies can manage cash flow with flexibility by factoring invoices according to needs rather than committing to long-term credit agreements.

- Scalable Funding: Grows with business sales, allowing companies to access higher funding as invoice volume increases without renegotiating agreements.

How Does Invoice Factoring Work?

The process involves the following steps:

- Invoice Generation: After delivering goods or services, the business creates and sends an invoice to the customer detailing payment terms.

- Selling the Invoice: The business sells unpaid invoice to a factoring company to receive immediate funds instead of waiting for payment.

- Advance Payment: The factoring company advances between 70 and 90 percent of the invoice value, providing quick working capital.

- Collection by Factor: The factoring business is in charge of handling follow-ups, guaranteeing prompt receipt, and obtaining payment from the client.

- Final Settlement: The factor takes agreed-upon costs out of the customer’s payment and sends the leftover amount to the company.

Types of Invoice Factoring

Here are the different types that businesses can choose based on their financial needs and risk preferences:

- Recourse Factoring: In recourse factoring, the business retains payment risk and must reimburse the factor if customers fail to settle invoices.

- Non-Recourse Factoring: In non-recourse factoring, the factor assumes credit risk and absorbs losses if customers default on all invoice payments.

- Disclosed Factoring: In disclosed factoring, customers are notified about the arrangement and make invoice payments directly to the factoring company.

- Undisclosed (Confidential) Factoring: In undisclosed factoring, customers remain unaware of the arrangement, and the business continues collecting payments without factor involvement.

- Spot Factoring: In spot factoring, businesses sell selected individual invoices occasionally instead of factoring their entire accounts receivable portfolio consistently.

Advantages of Invoice Factoring

Here are the key advantages that help businesses manage cash flow and support growth:

- Improved Cash Flow: Provides immediate funds from unpaid invoices, ensuring steady working capital and helping businesses maintain smooth daily operations.

- Faster Growth: Access to quick cash enables businesses to invest in expansion, purchase inventory, and enhance marketing efforts without financial delays.

- No Debt Burden: Since invoice factoring is not a loan, it does not raise debt obligations or add liabilities to the balance sheet.

- Reduced Collection Effort: Factoring companies manage invoice collections and follow-ups, saving businesses time, resources, and administrative effort involved in receivables management.

- Access for SMEs: Small and medium businesses with limited credit history can access funds, as approval depends mainly on customers’ creditworthiness.

- Flexible Financing Option: Offers flexible funding based on sales volume, allowing businesses to access more cash as their invoices grow.

Disadvantages of Invoice Factoring

Here are the key disadvantages that businesses should consider before choosing financing option:

- Higher Costs: Factoring fees and discount charges are often higher than traditional financing, increasing the overall cost of business funding.

- Customer Relationship Impact: Factor involvement in collections may influence customer perception and potentially strain long-term business relationships and communication trust.

- Dependency on Customer Credit: Approval depends primarily on customers’ creditworthiness, making it difficult if clients have poor payment history or weak financial standing.

- Limited Profit Margins: Discounting invoices reduces total revenue received, ultimately lowering profit margins and affecting overall business profitability and financial performance.

- Not Suitable for All Businesses: Businesses with low margins or limited invoice volume may find factoring less beneficial and not a cost-effective financing option overall.

- Loss of Control: Businesses may lose some control over the collection process, as the factoring company manages customer payments and communication directly.

Difference Between Invoice Factoring and Invoice Discounting

Here is a comparison between invoice factoring and invoice discounting based on key aspects:

| Basis | Invoice Factoring | Invoice Discounting |

| Ownership of Invoice | Sold to a factor | Retained by business |

| Collection Responsibility | A factor collects payments | The business collects payments |

| Customer Awareness | Usually disclosed | Usually confidential |

| Risk | May transfer to factor (non-recourse) | Remains with business |

| Cost | Generally higher | Relatively lower |

Real-World Example

Here is an example to understand how invoice factoring works in practice:

A manufacturing company supplies goods worth ₹10,00,000 to a retailer with a 60-day payment term. Instead of waiting, the company approaches a factoring firm.

- The factor advances 80% = ₹8,00,000 immediately

- After 60 days, the retailer pays the full amount

- The factor deducts a fee (say 2%) and pays the remaining balance

This allows the manufacturer to maintain smooth operations without disruptions to cash flow.

Use Cases of Invoice Factoring

Here are the common use cases across different types of businesses:

- Small and Medium Enterprises (SMEs): Helps manage working capital efficiently, ensuring smooth operations and meeting short-term financial obligations without disrupting cash flow.

- Export Businesses: Reduces risks in international trade by ensuring timely payments and protecting against delays or defaults from overseas customers.

- Startups: Provides quick access to funds without relying heavily on credit history, helping startups maintain operations and support early growth.

- Seasonal Businesses: Supports cash flow management during off-peak periods, ensuring businesses cover expenses and remain stable between high revenue cycles.

- Manufacturing Companies: Helps manufacturers maintain production cycles by ensuring steady cash flow for purchasing raw materials and managing operational expenses.

- Service-Based Businesses: Enables service providers to access funds quickly against invoices, helping cover payroll, overhead costs, and ongoing project expenses.

When Should a Business Use Invoice Factoring?

Here are the key situations where it can be a suitable financing option:

- Delayed Customer Payments: When customers pay invoices late, it creates cash flow gaps that affect daily operations and financial stability.

- Need Immediate Cash: When a business needs quick funds to manage expenses, invest in growth opportunities, or support ongoing operational activities.

- Difficulty Getting Loans: When businesses cannot secure bank loans due to strict requirements, limited credit history, or insufficient collateral availability.

- Creditworthy Customers: When a business serves customers with strong credit profiles, it increases the chances of approval and ensures timely payments through factoring arrangements.

- Rapid Business Growth: When a business is expanding quickly and needs consistent cash flow to fulfill increasing orders, hire staff, or scale operations without financial strain.

- Limited Internal Resources for Collections: When a business lacks the time or resources to manage invoice collections efficiently and prefers outsourcing receivables management to a factoring company.

Limitations of Invoice Factoring

Here are the key limitations that businesses should consider before adopting it:

- Long-Term Cost Accumulation: Continuous use of invoice factoring can lead to high cumulative costs, reducing overall financial efficiency over time.

- Selective Invoice Approval: Factoring companies may reject certain invoices based on customer risk, limiting access to funds for all receivables.

- Contractual Obligations: Some factoring agreements require long-term commitments, restricting flexibility and locking businesses into ongoing financial arrangements.

- Hidden Fees and Charges: The total cost may unexpectedly rise due to additional expenses like service charges, processing fees, or early termination penalties.

- Impact on Confidentiality: In disclosed factoring, customers become aware of third-party involvement, which may affect business privacy and professional image.

- Minimum Volume Requirements: Some factoring companies require a minimum invoice volume, making them unsuitable for businesses with low transaction volumes.

Final Thoughts

Invoice factoring is powerful financial tool that helps businesses maintain liquidity, manage cash flow, and support growth. Businesses may prevent operational delays and concentrate on growth by turning outstanding bills into instant cash. However, businesses must carefully evaluate the costs and suitability of factoring before adopting it. When used strategically, it can be an effective solution to overcome cash flow challenges and achieve financial stability.

Frequently Asked Questions (FAQs)

Q1. Is invoice factoring a loan?

Answer: No, invoice factoring is not a loan. It involves selling receivables rather than borrowing money.

Q2. Who uses invoice factoring?

Answer: SMEs, startups, exporters, and businesses with long payment cycles commonly use factoring.

Q3. Can startups use invoice factoring?

Answer: Yes, startups can use factoring if they have customers with strong creditworthiness.

Recommended Articles

We hope that this EDUCBA information on “Invoice Factoring” was beneficial to you. You can view EDUCBA’s recommended articles for more information.