What is Bankruptcy?

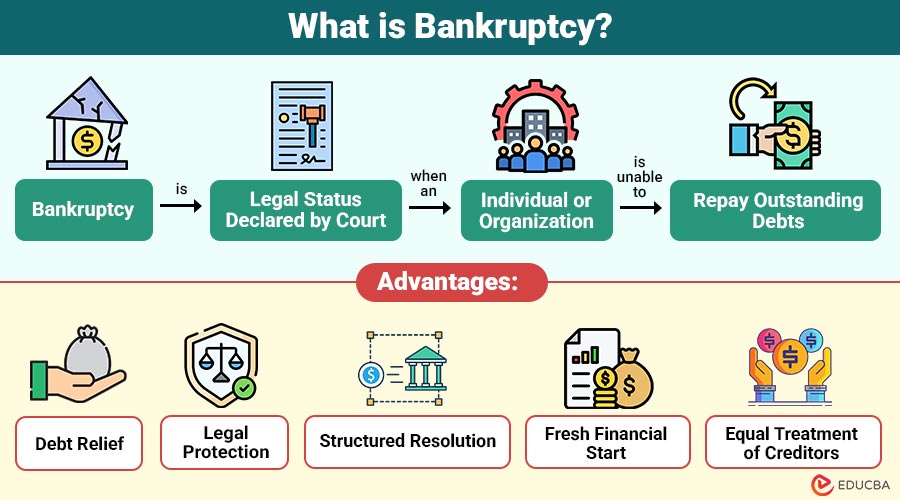

Bankruptcy is legal status declared by a court when an individual or organization is unable to repay outstanding debts. It allows debtors to either eliminate, reduce, or restructure their liabilities under the protection of bankruptcy laws.

Key Objectives of Bankruptcy:

- Provide financial relief to debtors

- Ensure orderly and fair repayment to creditors

- Prevent aggressive collection actions

- Enable financial rehabilitation or orderly liquidation

Bankruptcy laws differ by country, but the fundamental goal remains the same: resolving insolvency in a legally transparent and structured manner.

Table of Contents:

- Meaning

- When is Bankruptcy Declared?

- Types

- Process

- Impact

- Advantages

- Disadvantages

- Real-World Examples

- When Should Bankruptcy be Considered?

Key Takeaways:

- Bankruptcy provides a legal framework to resolve insolvency through debt relief, restructuring, or an orderly liquidation.

- It protects debtors via automatic stay while ensuring fair, transparent treatment and repayment opportunities for creditors.

- Different bankruptcy types address individuals, businesses, and municipalities based on financial condition and recovery objectives.

- Though initially damaging to credit, bankruptcy can enable financial rehabilitation, stability, and long-term sustainable recovery planning.

When is Bankruptcy Declared?

Bankruptcy is typically declared when:

1. Excessive Debts

An individual or a company generally declares bankruptcy when their total debts substantially exceed their available income or assets.

2. Missed Payments

When a person or business consistently misses payments to creditors, it usually indicates that they will eventually be unable to fulfill their financial responsibilities.

3. Rising Legal Actions

Legal pressures, including lawsuits, foreclosures, or creditor actions, often trigger bankruptcy when individuals or companies cannot reasonably manage their financial liabilities.

4. Insufficient Cash Flow

For businesses, bankruptcy arises when operating cash flows are insufficient to cover expenses, debts, and essential ongoing operational requirements.

Types of Bankruptcy

Bankruptcy is categorized based on the debtor’s situation and objectives. Below are the most common types:

1. Liquidation Bankruptcy

The court sells the debtor’s assets to repay creditors, discharges any remaining eligible debts, and terminates operations, which commonly occurs for individuals or businesses.

2. Reorganization Bankruptcy

Debts are restructured under a court-approved plan, allowing businesses to continue operations while making payments over time, often for large corporations.

3. Individual Debt Adjustment

Designed for individuals with regular income, it permits repayment through manageable installments while usually allowing retention of most personal assets.

4. Municipal Bankruptcy

Applies to cities, towns, or public entities to restructure public debt obligations, ensuring essential services continue and financial stability is restored.

Bankruptcy Process

The bankruptcy process generally follows these structured steps to assess insolvency, protect the debtor, and resolve debts legally and transparently.

1. Financial Assessment

The debtor reviews all debts, assets, income, and expenses carefully to determine insolvency and financial inability to pay.

2. Filing the Petition

A petition is submitted to the court, listing creditors, assets, liabilities, income, and expense statements accurately.

3. Automatic Stay

Filing triggers an automatic stay that immediately halts collection calls, lawsuits, wage garnishments, and foreclosure proceedings against the debtor.

4. Trustee Appointment

The court appoints a trustee who evaluates assets, communicates with creditors, and, if applicable, distributes funds to creditors.

5. Creditor Review

Creditors may object to claims, negotiate repayment terms, and participate in meetings regarding the debtor’s bankruptcy proceedings and obligations.

6. Debt Discharge or Repayment Plan

The court discharges eligible debts or approves a repayment plan that the debtor successfully executes over time.

7. Case Closure

After the debtor fulfills all obligations or the debts are discharged, the court formally closes the bankruptcy case.

Impact of Bankruptcy

Bankruptcy affects multiple stakeholders differently, influencing financial stability, operations, and recovery prospects across individuals, businesses, and creditors.

1. Impact on Individuals

- Credit score drops significantly

- Difficulty obtaining loans or credit cards

- Emotional and psychological stress

- Opportunity for a financial reset

2. Impact on Businesses

- Loss of investor confidence

- Vendor and customer concerns

- Operational restructuring

- Potential survival through reorganization

3. Impact on Creditors

- Partial or delayed repayment

- Legal protection against unequal treatment

- Structured recovery process

Advantages of Bankruptcy

Here are the key advantages that help individuals and businesses manage severe financial distress effectively.

1. Debt Relief

Eliminates or significantly reduces unmanageable debt, giving debtors relief from overwhelming financial obligations and repayment pressure.

2. Legal Protection

Automatic stay stops harassment, collection calls, lawsuits, garnishments, and foreclosures, legally protecting debtors during bankruptcy proceedings.

3. Structured Resolution

Provides an organized legal framework for systematically resolving debts, avoiding chaotic collections and creditor conflicts.

4. Fresh Financial Start

Allows individuals and businesses to rebuild finances, restore creditworthiness, and confidently plan sustainable, long-term financial futures.

5. Equal Treatment of Creditors

Ensures a fair, transparent distribution of assets or payments, treating all creditors equally in accordance with court-supervised rules.

Disadvantages of Bankruptcy

Here are the key disadvantages of bankruptcy that individuals and businesses should consider before filing.

1. Credit Damage

Credit scores and borrowing trustworthiness are severely reduced when bankruptcy is listed on credit reports for a number of years.

2. Asset Loss

Non-exempt assets may be sold by trustees to repay creditors, reducing personal or business property ownership.

3. Public Record

Bankruptcy filings become public records, allowing employers, lenders, and others to access financial history easily.

4. Limited Future Credit Access

Future credit access becomes limited, with higher interest rates, stricter lending terms, and reduced borrowing options.

5. Emotional and Reputational Impact

Emotional stress and social stigma may impact personal confidence, professional reputation, and overall mental well-being.

Real-World Examples

Here are practical, real-world examples illustrating how bankruptcy applies to individuals and businesses.

1. Individual

An individual with high medical bills and credit card debt files for liquidation bankruptcy. Assets are minimal, debts are discharged, and the individual begins rebuilding credit.

2. Business

A retail chain facing declining sales files for bankruptcy. It closes underperforming stores, renegotiates leases, restructures debt, and continues operations.

When Should Bankruptcy be Considered?

Here are common situations in which bankruptcy may be an appropriate option for individuals or businesses facing severe financial distress.

1. Debt Repayment is Impossible

Debt repayment becomes realistically impossible when obligations far exceed income, assets, or repayment capacity over time.

2. Legal Actions Threaten Assets or Income

Ongoing lawsuits, garnishments, or foreclosures threaten essential assets or income, making bankruptcy protection necessary for survival.

3. Persistently Negative Cash Flows

Cash flows remain persistently negative, preventing the meeting of operating expenses, debt payments, and the maintenance of normal financial operations.

4. Business Survival Requires Restructuring

Business survival depends on formal restructuring to reduce debt burdens, renegotiate obligations, and restore long-term operational viability.

Final Thoughts

Bankruptcy is a powerful legal remedy designed to address severe financial distress when other options fail. While it carries long-term consequences, it also offers protection, structure, and a path toward recovery. When used responsibly and with professional guidance, bankruptcy can serve as a strategic reset, enabling individuals and organizations to regain stability and rebuild sustainable financial futures.

Frequently Asked Questions (FAQs)

Q1. Is bankruptcy the end of financial life?

Answer: No. Many individuals and businesses recover successfully after bankruptcy with disciplined financial planning.

Q2. How long does bankruptcy stay on a credit report?

Answer: Typically between 7 and 10 years, depending on jurisdiction and type.

Q3. Is bankruptcy always voluntary?

Answer: Not always. In some cases, creditors may initiate proceedings.

Q4. Can all debts be erased through bankruptcy?

Answer: No. Certain obligations, such as taxes, student loans, and child support, usually remain.

Recommended Articles

We hope that this EDUCBA information on “Bankruptcy” was beneficial to you. You can view EDUCBA’s recommended articles for more information.