What are Floating Rate Bonds?

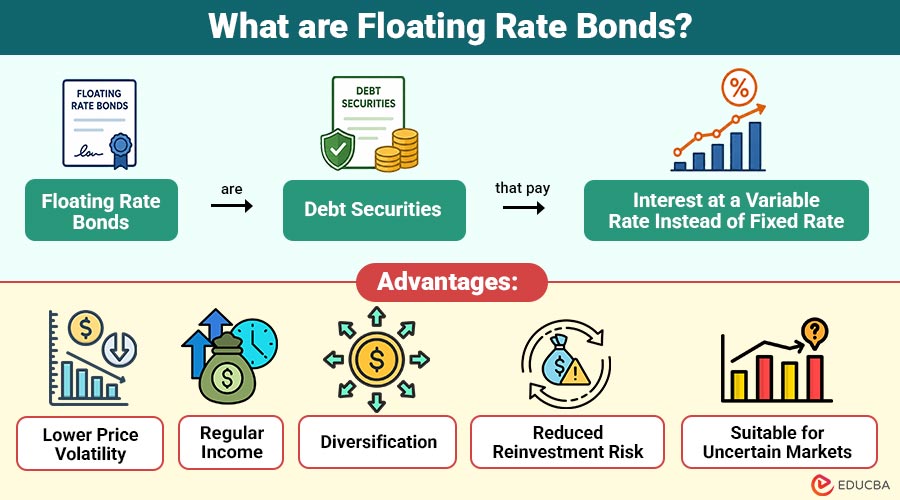

Floating rate bonds (FRBs) are debt securities that pay interest at a variable rate instead of a fixed rate. The coupon rate is linked to a benchmark interest rate, such as the SOFR, treasury bill rate, or another market reference rate, plus a fixed spread.

For example, suppose a company issues a floating-rate bond with an interest rate of SOFR + 2%. If SOFR is currently 4%, investors receive 6% interest. If SOFR rises to 5%, the coupon automatically adjusts to 7% during the next reset period.

Because coupon payments vary with interest rates, floating-rate bonds experience less price fluctuation than fixed-rate bonds when interest rates change.

Table of Contents:

- Meaning

- Key Features

- Types

- Working

- Advantages

- Disadvantages

- Difference

- Applications

- Who Should Invest?

- Example

Key Takeaways:

- Floating rate bonds pay variable interest linked to benchmark rates, helping investors adapt to changing markets.

- Coupon payments reset periodically, reducing interest rate risk and lowering bond price volatility significantly overall.

- These bonds perform best during rising interest rates, offering potentially higher income through increasing coupon payments.

- Investors should consider the issuer’s credit quality, benchmark movements, and investment objectives before purchasing floating-rate bonds.

Key Features of Floating Rate Bonds

Some important key features of floating-rate bonds include the following:

1. Variable Interest Payments

Interest payments vary with benchmark interest rates, so investors’ income can rise or fall with market conditions.

2. Periodic Coupon Reset

Coupon rates are reset monthly, quarterly, semi-annually, or annually based on changes in the selected benchmark rate.

3. Lower Interest Rate Risk

Floating-rate bonds experience less price volatility than fixed-rate bonds because coupon payments adjust with interest rates.

4. Fixed Spread

Most floating-rate bonds add a fixed spread above the benchmark rate, providing consistent additional returns for investors.

5. Principal Repayment

Investors generally receive the bond’s full face value upon maturity, provided the issuer fully meets its repayment obligations.

6. Suitable During Rising Rates

These bonds perform well when interest rates rise because higher benchmark rates automatically increase future coupon payments.

Types of Floating Rate Bonds

Floating-rate bonds are available in several forms depending on the issuer and coupon structure.

1. Corporate Floating Rate Bonds

Companies issue floating-rate bonds to raise funds for business expansion, acquisitions, or operational needs. These bonds generally offer higher spreads because corporate issuers carry greater credit risk than governments.

2. Bank Floating Rate Notes

Banks frequently issue floating-rate notes (FRNs) to strengthen their capital base and manage funding requirements.

3. Asset-Backed Floating Rate Securities

These securities have coupons that change on a regular basis and are secured by financial assets including credit card receivables, vehicle loans, and mortgages.

4. Callable Floating Rate Bonds

The issuer has the right to redeem the bond before maturity, usually when market interest rates decline.

How do Floating Rate Bonds Work?

It follows a straightforward process:

Step 1: Bond Issuance

A government or company issues a bond with a variable coupon formula.

Example:

Coupon = Benchmark Rate + Fixed Spread

Step 2: Initial Coupon Rate

The initial interest payment is calculated using the current benchmark rate.

Example:

- Benchmark Rate = 5%

- Fixed Spread = 1.5%

Coupon Rate = 6.5%

Step 3: Periodic Reset

After every reset period, the benchmark rate is reviewed.

If the benchmark increases:

- Coupon payment increases.

If the benchmark decreases:

- Coupon payment decreases.

Step 4: Interest Payments

Investors receive coupon payments according to the updated interest rate throughout the bond’s life.

Step 5: Maturity

At maturity, investors receive the bond’s face value (principal).

Advantages of Floating Rate Bonds

Below are the key advantages of floating-rate bonds and how they benefit investors across different interest-rate environments.

1. Lower Price Volatility

Floating-rate bonds generally experience lower price fluctuations because their coupon payments adjust periodically with changing market interest rates.

2. Regular Income

Investors receive periodic interest payments throughout the bond’s life, providing a steady income stream despite changing market conditions.

3. Diversification

Floating-rate bonds diversify investment portfolios by reducing sensitivity to interest-rate changes while effectively complementing other fixed-income investments.

4. Reduced Reinvestment Risk

Higher coupon payments during periods of rising interest rates reduce the need to reinvest earnings at comparatively lower available rates.

5. Suitable for Uncertain Markets

These bonds perform relatively well in uncertain markets because their coupon payments automatically adjust to changing interest rate environments.

Disadvantages of Floating Rate Bonds

Below are the major disadvantages that investors should consider before investing.

1. Lower Income When Rates Fall

Coupon payments decrease when benchmark interest rates decline, resulting in lower income for investors over the bond’s duration.

2. Credit Risk

Corporations carry credit risk because repayment depends on the issuer’s financial strength and stability.

3. Benchmark Dependence

Investment returns largely depend on movements in benchmark interest rates, making income less predictable during changing market conditions.

4. Complex Structure

Understanding benchmark calculations, coupon resets, and spread adjustments can be challenging for beginners and inexperienced bond investors.

5. Limited Capital Appreciation

Stable bond prices reduce opportunities for significant capital gains compared with traditional fixed-rate bonds when interest rates are falling.

Difference Between Floating Rate Bonds and Fixed Rate Bonds

The table below highlights the major differences between the two:

| Feature | Floating Rate Bonds | Fixed Rate Bonds |

| Interest Rate | Variable | Fixed |

| Coupon Payment | Changes periodically | Remains constant |

| Interest Rate Risk | Lower | Higher |

| Price Volatility | Lower | Higher |

| Income Stability | Variable | Stable |

| Best During | Rising interest rates | Falling interest rates |

| Market Value | More stable | More sensitive to rate changes |

| Investor Preference | Protection from rate increases | Predictable income |

Applications of Floating Rate Bonds

Floating-rate bonds are widely used in various financial situations.

1. Corporate Borrowing

Businesses use it to finance expansion, acquisitions, infrastructure projects, and long-term capital investment requirements effectively.

2. Banking Sector

Banks issue floating-rate notes to raise funds, strengthen capital, and support lending activities during changing interest rates.

3. Investment Portfolios

Portfolio managers include it to reduce interest rate risk while generating regular variable income for investors.

4. Pension and Insurance Funds

Pension funds and insurers invest in floating-rate bonds to effectively balance their portfolios against changing interest-rate environments.

5. Wealth Management

Financial advisors recommend it for clients seeking rising income potential with reduced interest rate sensitivity.

Who Should Invest?

It may be suitable for:

1. Investors Expecting Interest Rates to Rise

Investors anticipating rising interest rates can benefit from higher coupon payments that adjust with benchmark rates.

2. Income-Focused Investors

Income-focused investors comfortable with variable payments may benefit from increasing cash flows in rising-rate environments.

3. Conservative Investors

Conservative investors seeking lower interest-rate risk may prefer it to fixed-rate alternatives.

4. Portfolio Managers

Portfolio managers seeking diversification can balance fixed-income exposure with securities that offer variable interest payments.

5. Banks, Pension Funds, and Insurance Companies

Banks, pension funds, and insurance companies use floating-rate bonds to manage interest-rate exposure effectively.

6. Long-Term Investors

Long-term investors wanting protection against changing market rates may benefit from periodically adjusting bond coupon payments.

Example

The following example shows how the interest payments on a floating rate bond change as the benchmark interest rate changes over time.

Suppose ABC Corporation issues a 5-year floating rate bond with:

- Face Value = $10,000

- Benchmark Rate = 4%

- Fixed Spread = 2%

- Reset Frequency = Every six months

First Six Months:

- Coupon Rate = 6%

- Annual Interest = $600

After Six Months:

- Benchmark increases to 5%.

- New Coupon Rate = 7%

- Annual Interest = $700

One Year Later:

- Benchmark falls to 3%.

- New Coupon Rate = 5%

- Annual Interest = $500

This example shows how investor income changes with market interest rates.

Final Thoughts

Floating rate bonds are an effective investment option for managing interest rate risk while earning regular income. Unlike fixed-rate bonds, their coupon payments adjust with market interest rates, making them particularly valuable during periods of rising rates. Although returns may decline when benchmark rates fall and investors still face issuer credit risk, floating-rate bonds offer greater flexibility, lower price volatility, and useful portfolio diversification. Understanding how they work helps investors decide whether they fit their income goals, market outlook, and overall investment strategy.

Frequently Asked Questions (FAQs)

Q1. How often do floating rate bond coupons change?

Answer: The coupon is usually reset monthly, quarterly, semi-annually, or annually, depending on bond’s terms.

Q2. Are floating rate bonds safer than fixed-rate bonds?

Answer: They generally have lower interest rate risk, but investors still face credit risk depending on the issuer.

Q3. What happens if interest rates rise?

Answer: The bond’s coupon payments increase during the next reset period, providing higher income to investors.

Recommended Articles

We hope that this EDUCBA information on “Floating Rate Bonds” was beneficial to you. You can view EDUCBA’s recommended articles for more information.